Rates spark: Debt ceiling deal adds to bond angst

A deal to raise the US debt ceiling increases selling pressure on Treasuries, but will also result in tighter financial conditions for the economy. This opens upside to EUR rates but a soggy economic backdrop means wider rate differentials near-term.

Once approved, the debt limit deal paves the way to a liquid crunch

The deal between President Biden and House leader McCarthy amounts to the removal of a tail risk for financial markets, that of a US default. Even if this was a tiny probability event to begin with, it'll allow markets to focus on the more important debate: whether the Fed is indeed done with its hiking cycle. The budget deal, which lifts the debt limit for two years and caps some categories of government spending, still needs to be approved by the House tomorrow. The outcome of the vote is uncertain but the likely opposition by some Republicans means Democrat votes will be key. We expect the run-up to the vote to see Treasury Yields gradually climb higher if more lawmakers come out in favour of the deal.

Money markets can expect a $500bn liquidity drain over the coming months

Beyond tomorrow, US rates will quickly look past the deal and turn their attention to the Treasury's task of rebuilding its cash buffer at the Fed. Two aspects matter here. On the liquidity front, money markets can expect a $500bn drain over the coming months as more debt is issued. In a context of $95bn/month Quantitative Tightening (QT) and of likely tightening of at least some banks' funding conditions, this should amount to an additional drag on financial conditions for the broader economy. This should ultimately draw a line under the US Treasury selloff but, should the new borrowing come with an increase in maturity, some of that support may be weakened.

The case for a June hike has strengthened after Friday's higher than expected core PCE print and Treasuries are set to trade softly into Friday's jobs report as recent prints have demonstrated the labour market's resilience. 4% yield for 10Y now seems a more achievable level.

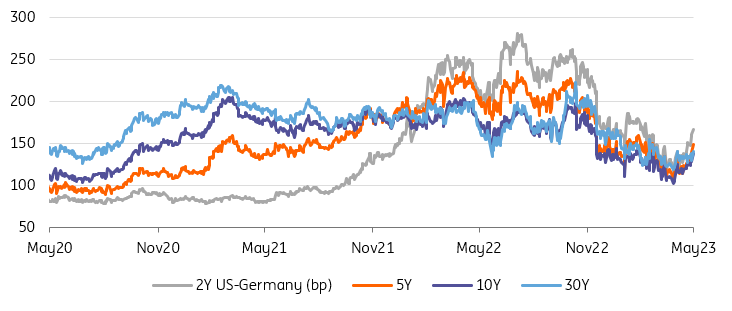

Weak European data prevents EUR rates from rising as fast as their US peers

Source: Refinitiv, ING

European rates back the hawkish ECB view but upside is more limited than in the US

In Europe, this week's inflation data, starting today with a print from Spain, will play a major role in how European rates trade into the June European Central Bank (ECB) meeting. To be sure, a pick-up in Fed hike expectations for June or July has also opened some upside for EUR rates but the domestic swap curve already discounts a path for ECB policy rates that is consistent with its communication. This comes against a backdrop of soggy hard economic data, and against a softening of sentiment indicators, such as last week's German Ifo which should also prevent European markets from getting too upbeat.

Unacceptably high core price dynamics will lend a helping hand to ECB officials pushing for a hawkish line

The most likely outcome to this week's inflation releases, still unacceptably high core price dynamics, will lend a helping hand to ECB officials pushing for a hawkish line. Warnings that hikes may have to continue until September will stand a better chance of pushing longer term rates higher even if a subdued economic outlook, and growing doubts about the strength of China's post Covid recovery, should prevent European rates from rising as quickly as their US peers in the coming weeks. Wider USD-EUR rates differentials should only be a temporary development, however, and one resulting from a rise in global rates. Market participants who, like us, expect lower rates into year-end, should also consider the possibility of US rates falling faster than their European peers, perhaps to sub-100bp levels for 10Y Treasury-Bund spreads.

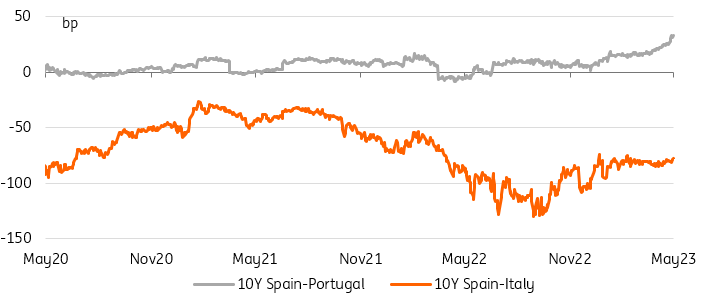

This is all the more true since European markets have to contend with another dollop of political uncertainty in the form of early Spanish general elections on 23 July. The prime minister called for a vote after local elections defeat at the weekend and the opposition party PP is on the front foot, although it would likely rely on a coalition with another party due to the fragmented nature of the Spanish political landscape. Spain’s still wide budget deficit (the European commission forecasts 4.1% of GDP this year and 3.3% next) mean a period of uncertainty is an unwelcome development and could lead to underperformance of Spanish government bonds vs peers such as Portugal and Italy.

Early elections mean Spanish bonds are at risk of underperformance vs Italy and Portugal

Source: Refinitiv, ING

Read the original analysis: Rates spark: Debt ceiling deal adds to bond angst

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.