Rates spark: Data catches up to the market

US data is converging fast towards the market’s bearish expectations but there are still some important releases to come this week, starting with ISM services today. Treasury yields should continue to converge lower but 10Y should prove stickier below 3%. USD-EUR rates differentials should continue to narrow.

US macro vindicates our call for lower Treasury yields

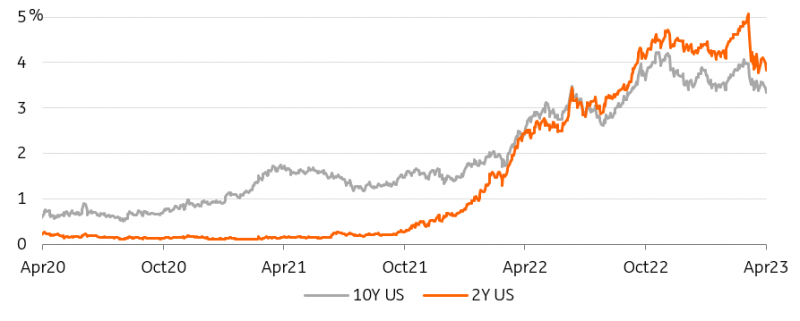

It is tempting to conclude from economic data released so far this week that the world economy is turning a corner, and that the market’s bearish expectations are being fulfilled. Indeed, the subsequent release of disappointing ISM manufacturing and job openings in the US suggests that the lag between the US regional bank crisis and the time when data starts falling (regardless whether the two are related) may not be so long after all. This view matches ours, but we would caution that this week still has a lot in store, starting with the ISM services today (a greater portion of the economy than manufacturing) and the jobs report (on Friday, when markets are closed). Caution is not the market’s default mode, however. 10Y Treasury yields are flirting with their lowest closes since September 2022, which would be a break through a floor that has held on at least four occasions since. As Fed cuts become more probable, yields should continue to fall. Indeed, we forecast 3% for year-end but don’t expect any fall below that level to be longer-lasting, as inflation expectations and term premia should recover with lower policy rates. The extent of the fall in 2Y yields will depend on the size of the Fed cutting cycle and it doesn’t benefit from the inflation expectation cushion that protects 10Y bonds.

2Y Treasury yields are converging fast to 10Y as the end of the Fed's tightening cycle approaches

Source: Refinitiv, ING

European rates prove stickier, more spread tightening is on the cards

We would be remiss if we did not mention that Europe is doing its part in feeding the deflationary narrative. The European Central Bank’s consumer expectations continue to converge downwards. The tone at the ECB, rightly or wrongly, remains hawkish however. Where the US swap curve assigns less than a 50% probability to a final 25bp hike at the Fed’s May meeting, the EUR curve still bakes in two more 25bp hikes in this cycle with a high degree of confidence. This in itself justifies a convergence between dollar and euro rates, but the policy difference might become even starker in the following quarters.

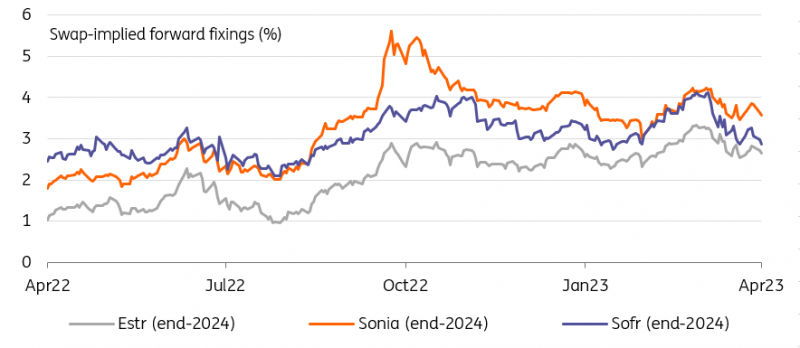

By end-2024, the differential in policy rates would have narrowed by 150bp

We see the Fed cutting rates 100bp this year, whereas the market has over 75bp priced. In comparison, we expect ECB cuts to only start in the third quarter of 2024, and to only amount to 50bp by end-2024. By that point, the differential in policy rates with thr Fed would have narrowed by 150bp. By some measures, the eurozone will have the same policy rate as the US. This last happened in the 2008-2012 period. This should drive a narrowing of US-eurozone rates differentials across maturities.

At the 10Y point, Bund-Treasury spreads reached their tightest level since 2020 yesterday, but we expect them to narrow to 90bp by year-end. A more steadfast ECB may well push this to 75bp temporarily. Indeed, the narrowing should be even more impressive at the front-end but we think this is already expected to an extent, in with for instance 1Y1Y Estr trading only 28bp lower than its USD equivalent.

Forwards are pricing a convergence between US and European policy rates

Source: Refinitiv, ING

Read the original analysis: Rates spark: Data catches up to the market

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.