Rates spark: Can the Fed manage to keep a straight face?

The baseline view is that the Fed will bore us with a nothing outcome. They just can't be more dovish (could they?). So they can only surprise to the hawkish side. You can see then where the risks lie here. The smallest of pebbles can cause ripples. Meanwhile, Euro markets are facing a wall of supply that threatens hopes for stable rates into the summer.

Not much is expected from the Fed, but be careful as the smallest nuance can potentially have a big effect

One thing is for sure heading into today's FOMC meeting - the Fed could not possibly come out of it with a more dovish stance than they went in. This is an important nuance. The only issue is the degree, if at all, that the Fed pendulum moves in the direction of hawkishness. How could the Fed do this?

Move a few dots shorter and we suddenly have the Fed hiking a year earlier

First, one or more of the Fed members could move their "dot" shorter. At the moment there is a spectrum of dots (effectively individual Fed member votes) that result in a median call for a first rate hike in 2024. It would just take a few of those 2024 dots to slip into 2023 for there to be an instantaneous shortening of one year to the first Fed rate hike. Is there enough rationale out there for this to happen? Sure is; try 5% inflation for starters.

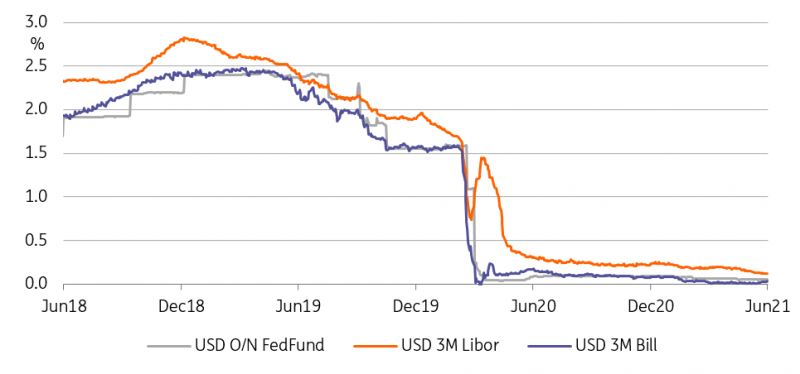

An RFF/IOER hike would help rates off 0% but Fed Fund effective has remained well above that line

Source: Refinitiv, ING

Second, the Fed could simply choose to verbally intervene by using language that acknowledges that they see what we all see. It may seem obvious, but it is important. Crucial here would be any recognition that inflation pressures might be building. One blink from the Fed could be enough to cause a re-pricing, all the way from the front end to right out the curve.

Any "technical" hike might not be a policy tightening, but it would still be a tightening

Third, the Fed, cognizant of the significant build in liquidity returning at 0% on the reverse repo facility, and its decision not to extend the break that banks got on the leverage ratio (which in part contributed to this), could attempt to coax up front end rates through technical hikes in the reverse repo rate (now 0%) and the rate on excess reserves (now 10bp). This would be a technical hike, one that would be watered down by the Fed as being just that, a technical move, and not a signal of monetary tightening. True, but still, a tightening it would in fact be.

The problem with a techncial hike like this is it attempts to change the price of liquidity without addressing the excess of it in the first place. We don't rule it out, as it is a viable approach. However, it might be smarter for the Fed to maintain an aloofness here (our base view), as they can handle the liquidity coming back, and increased volumes going into the reverse repo window is in itself a temporary technical adjustment to what should be a temporary situation (albeit likely to last for another month or so).

Let's see. We don't expect a surprise, and if we don't get one then vanilla carry trade for rates and risk-on for equities continue. But be pre-warned that any surprise here only points in one direction; a more hawkish Fed coming out the other side of the meeting.

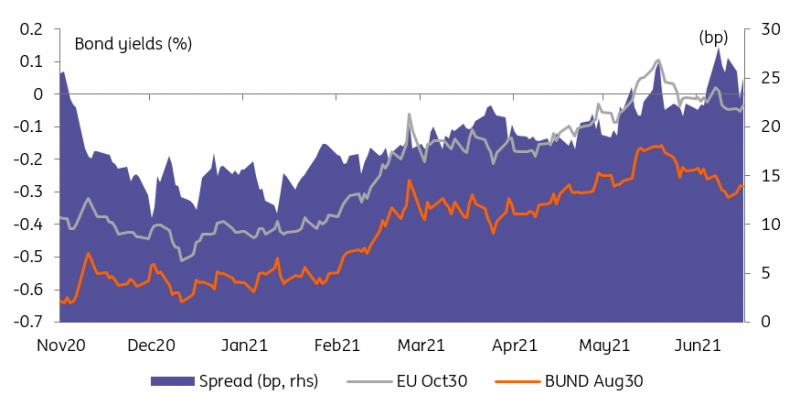

EU spreads to Bund have widened only modestly into the start of NGeu issuance

Source: Refinitiv, ING

EUR debt supply: Bracing for more

If USD markets can be expected to trade in a holding pattern into tonight’s FOMC meeting, EUR rates have to contend with the reality likely to prevail until the summer at least: low rates and rates volatility are attracting not only carry traders but also borrowers. The headliner is of course the EU’s maiden NGeu deal yesterday, raising nearly twice the amount we expected at €20bn. It seems that even these dizzying amounts are no particular challenge for the market to absorb, but supply events look set to bear more and more on the level of yields.

In the case of the EU, it is worth remembering that two more syndicated deals are expected before the end of July. There is no certainty about the magnitude of those deals but clearly the perceived ceiling for EU deal size has been raised. In this context, further repricing of EUR rates makes sense. Naturally, core and semi-core sovereign bond markets look most at risk to widen relative to other assets. Higher yielding bonds on the other hand, chiefly peripheral debt, look set to be less affected. Primarily because issuers in that group are also most likely to be the main beneficiaries to bountiful EU borrowing before the summer recess.

Today’s events and market view

Today’s FOMC meeting (occurring after the European close) looks set to keep market activity in check with US investors preferring to keep their powder dry before the event.

Germany will test investors’ appetite for 10Y debt only one day after the EU’s jumbo €20bn 10Y deal. Even with its more modest €5bn size, we think this skews price action in favour of higher EUR rates, as both Spain and France are waiting in the wings with auctions tomorrow.

The highlight of the data calendar will be US housing starts and building permits.

Read the original analysis: Rates spark: Can the Fed manage to keep a straight face?

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.