Rates Spark: Bank of England vs the market

UK rates haven’t had a chance to fully digest the Bank of England’s statement yesterday. We think hike expectations will persist, but there are other areas where the BoE and Treasury can restore confidence. Italian bonds didn’t fare well on the first day of the Meloni era. Tough to stand in the way of higher US rates, even with the market very biased that way.

UK gilts: All crises lead to higher yields

From inflation to fiscal sustainability worries, and from fiscal sustainability worries to a loss of confidence in sterling and sterling-denominated assets, the past few months have been a bruising one for gilts. Macro concerns are of course legitimate, but we feel the scale of the sell-off in UK rates has a clear element of market disfunction. Liquidity in gilts has been deteriorating all year and the Bank of England (BoE) is adding to the already fraught environment by reducing the size of its bond portfolio. Stopping this policy, also known as quantitative tightening (QT), is one of the low hanging fruits for UK policymakers to restore confidence in the country’s economic management.

This is a necessary but by no means a sufficient condition, however. Gilts have suffered from the perception that the Treasury (through more generous spending and tax cuts) and the BoE (trying to offset the inflationary implications) are working at cross purposes. The result has been a perfect storm: more gilts issuance and more BoE hikes. Any sign of better cooperation (for instance by government spending cuts or a windfall tax on energy companies) would also go a long way to shore up confidence in gilts and the pound. As often however, it will take time for investors to regain their appetite for gilts after the recent volatility. At first glance, the BoE’s struggle to calm market expectations of an inter-meeting emergency hike is another example of the market’s nervousness.

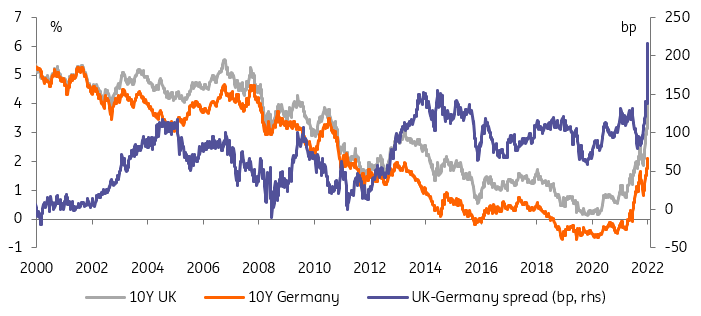

10Y gilts have crossed well above our 4% yield and 200bp spread over Bund forecasts. Given that some of this sell-off is explained by hopes of a BoE intervention that might not materialise, we would refrain from moving our forecast ever higher.

Gilts have moved through our 4% yield and 200bp spread to Bund forecasts

Source: Refinitiv, ING

Italy, the carrot and sticks do their job, for now

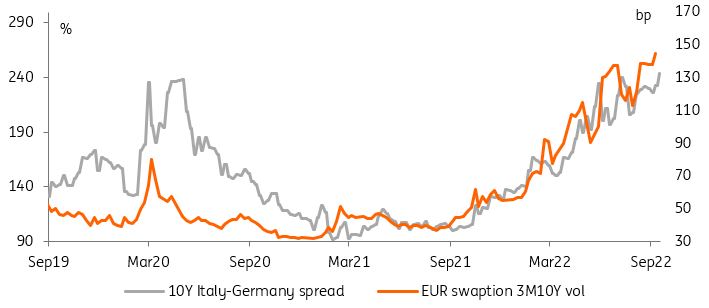

Italy’s political developments played second fiddle to the exceptional volatility in sterling markets but the election of a potentially stable right wing coalition is no less momentous. Markets took a sanguine view judging from the solid price action in Italian bonds into the election, but Italian bonds gave it all back yesterday. We tend to agree that, in the short run, risks of fiscal divergence are limited. Potential good news could be the nomination of a market-friendly Finance Minister (eg, out of the European Central Bank or Banca d’Italia), and no wholesale change to the 2023 budget.

At its core, the market’s relaxed approach is a reflection of the trust in the EU’s carrot (almost €200bn in grants and loans from NGeu) and stick (risk of a bond market crisis if the ECB withdraws its support). Longer-term, markets are ill equipped to assess the risk of Italy diverging from EU fiscal guidance from a party that has never been in power. All this calls for caution, especially given the backdrop of hawkish central banks. The prospect of the ECB reducing its bond portfolio in particular could be another delay of selling pressure on Italian bonds, and take 10Y spreads to Germany above the 250bp.

Even if they give Meloni the benefit of the doubt, Italian spreads are pushed wider by rates volatility

Source: Refinitiv, ING

US market rates still on wider crisis watch

The US 10yr yield is powering towards 4%, and the Treasury / Bund spread has re-widened, but there is not a huge sense that the bond market rout is being driven by the Treasuries. It's more of a synchronized process, but with differentiating drivers (two of which are summarized above). The common denominator is interest rate risk, and the net power play is the US by virtue of implied capital flows coming from the movement in FX rates (dollar strength). These in fact mute the magnitude of rises in US market rates.

That said, bond players maintain a preference to short the market. The repo market is littered with bond trading on special, reflecting an ongoing excess of liquidity over collateral, but also now two other items, 1. A market preference to short the market (where bonds need to be borrowed), and 2. A desire to fly to the safety of the Fed’s reverse repo facility where 3.05% is on offer with no capital at risk. SOFR is finding is tough to even get up to 3% (latest 2.99%), which is illustrative of the same.

And the system is holding up so far. Financial commercial paper is holding in at single digit over the risk free rate. We can’t see this continuing; expect a larger concession to build for bank funding ultimately. But for now, all is good; which is also a positive signal for contemporaneous liquidity circumstances. Wider liquidity has become worse in the past number of days though. Price discovery is tough in consequence, causing prices to run away from business, manifesting in wider bid/offer spread at times.

Read the original content: Rates Spark: Bank of England vs the market

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.