Rates Spark: Accelerated tightening timetable

Rates markets have taken reports of an accelerated European Central Bank tightening process in their stride. If such reports are confirmed next week, we expect another leg wider in sovereign spreads, and core rates. The money markets' reaction depends on how the ECB pushes banks to repay TLTRO loans; we may get more information in the coming days.

ECB sequencing on steroids

Francois Villeroy has often been one of the ECB officials laying out his policy expectations most explicitly. Even if he’s only one member of the 25-strong governing council, his opinion can also reflect the tone of policy discussions that are happening behind closed doors. He has also been more often at the slightly more hawkish end of the council, which in the currently hawk-dominated debate makes him a relatively interesting barometer of where the discussion is.

This makes his expectation that quantitative tightening could start from the end of this year a particularly notable one. Press reports so far have suggested a start in the course of 2023, most likely in the second quarter. This was to give the ECB time to reach neutral deposit rates (likely around 2%) and to mop up some of the excess liquidity created by targeted longer-term refinancing operation (TLTRO) loans to banks. That suggested timing would not only imply an earlier reduction of the ECB’s bond portfolio, but also a decision as early as next week on how to nudge banks into repaying their TLTRO loans.

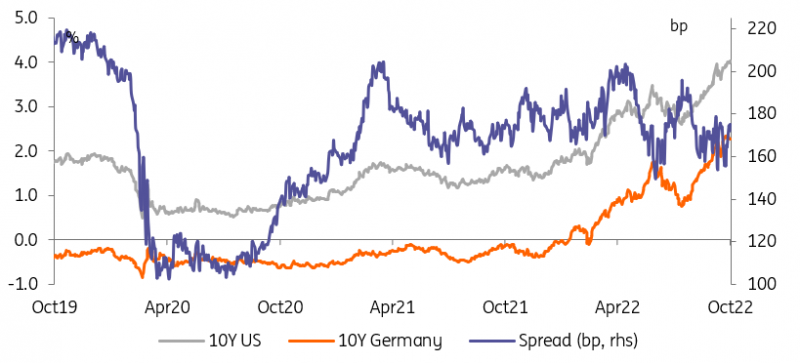

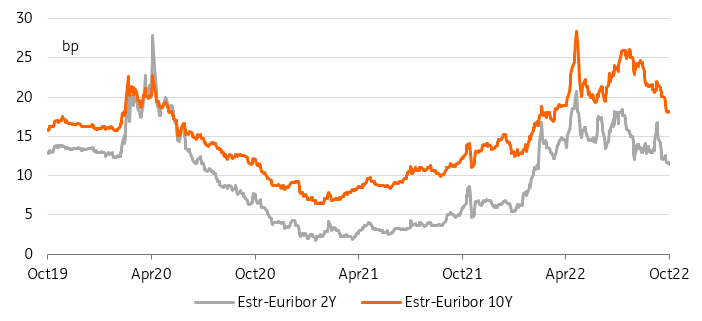

Market reaction to QT or TLTRO-related headlines has been very muted. It is difficult to discern euro-specific drivers among the gilt-induced volatility but there has been no appreciable uptrend in sovereign spreads in recent weeks, and the spread of German 10Y yields relative to Treasuries remains well within its recent range. The same goes with money market spreads, which are prime candidates for widening when the ECB tightens policy (see below), and long-dated bases have tightened, if anything.

The prospect of ECB QT hasn't pushed euro yields up relative to dollar

Source: Refinitiv, ING

Liquidity reduction and quantitative tightening around the corner

Both are momentous decisions that should be considered carefully by market participants. In the case of pushing banks to repay TLTRO loans, the range of options on the table is so wide that it is difficult to have great certainty about the market impact. Ranging from the most to the least likely, we could see:

-

A reduction of excess liquidity to the tune of €0.5tn in December and €0.5tn in March.

-

A greater sensitivity of Euribor fixings to widening in credit and sovereign spreads.

-

A rise in Estr fixings relative to the ECB deposit rate.

-

A rise in repo rates relative to Estr fixings.

-

An easing of collateral scarcity.

-

A differentiated tightening of liquidity conditions in various member states.

Except for the first two, these impacts will depend on the type of mechanism implemented by the ECB. We’ve done our best to keep up with various trial balloons released in the press in dedicated publications on TLTRO repayments, comparison with other central banks' options, and the broader choice of reserve tiering.

Quantitative tightening is more straightforward in that there seems to be a broad agreement on the form it will take: a progressive phasing out of reinvestment of its asset purchase programme (APP) portfolio starting sometime in 2023 (or very late in 2022), and then the same for pandemic emergency purchase programme (PEPP) reinvestments in 2025. Here too, we’ve covered the implications in more detail in a dedicated publication but we would expect another leg wider in sovereign spreads, an acceleration of money market spread widening when combined with TLTRO repayments (see above), and eventually higher core rates although we think the effect should be manageable next year.

Money markets don't appear concerned about a widening of Euribor fixes

Source: Refinitiv, ING

Read the original analysis: Rates Spark: Accelerated tightening timetable

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.