Q1 2017 Net Treasury Issuance Forecast Update

Last week's release of the Quarterly Refunding Statement indicated that the Treasury intends to borrow $57 billion in Q1 and $1 billion in Q2. We estimate 2017 calendar year net Treasury issuance of $613 billion.

Treasury Expected to Draw Down Cash Balance in Q1

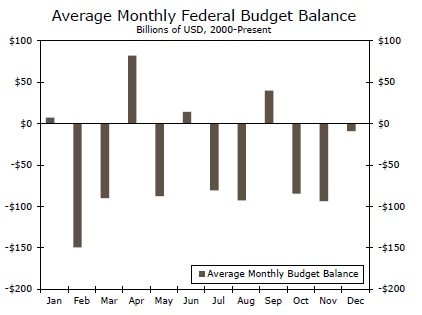

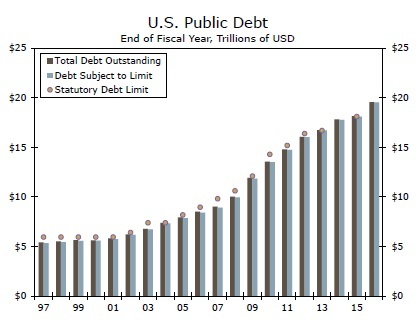

In Q1, the Treasury estimates a net marketable borrowing need of $57 billion, resulting in an end-of-quarter cash balance of $100 billion. The Q2 estimated marketable borrowing need is $1 billion, with an assumed end-of-quarter cash balance of $200 billion. While it would not be surprising in Q2 to see lower net marketable borrowing given the additional cash inflows into the Treasury from April tax collections (top graph), it is a bit unique to see such a low Q1 net borrowing estimate. One of the primary reasons for the lower Q1 borrowing estimate is related to the reestablishment of the debt ceiling on March 15 (middle chart). The last time the debt ceiling was suspended, Congress added a provision that instructs the Treasury to draw down its cash balance to $23 billion after the reestablishment of the borrowing limit. As of December, the Treasury had a cash balance of $399 billion, which is estimated to be reduced to comply with this new restriction before the end of the first quarter. Given this sizable cash draw down, we expect Treasury issuance to slow, particularly leading up to March 15, which could result in slightly lower rates across the curve due to the reduced new supply. We expect these lower rates to disproportionally affect the short-end of the curve. It is important to note that the cash drawdown around March 15 is expected to reduce net Treasury issuance, not the amount of outstanding Treasury securities. Once Congress passes an increase or another suspension of the debt ceiling, we expect net Treasury issuance to pick back up, which, in turn, could result in marginally higher rates across the curve but particularly at the short-end given the Treasury's intent to ramp up T-bill issuance this year. In short, expect some interest rate volatility, particularly at the short-end of the curve related to the March 15 debt ceiling deadline.

Net Treasury Issuance Forecast for CY 2017 and 2018

In our Monthly Economic Outlook released this morning, we made explicit assumptions about the future path of federal fiscal policy, which altered our views on the federal deficit and net Treasury issuance over the next two years. We now expect the federal budget deficit to total $650 billion in federal fiscal year 2017 and $950 billion in fiscal year 2018. Converting to calendar years, we expect net Treasury issuance to total $613 billion this calendar year, a slight decrease from the $715 billion issuance in calendar year 2016. The decline stems from a combination of drawing down the cash balance after the March 15 debt ceiling reestablishment and a shift in the timing of payments that pulled forward some payments at the end of the 2016 federal fiscal year. The most significant change to our issuance outlook is for calendar year 2018, where we now expect net Treasury issuance to total $975 billion, with total T-bill issuance amounting to roughly $209 billion and interest-bearing issuance of $765 billion.

Author

Wells Fargo Research Team

Wells Fargo