Project Freedom on pause

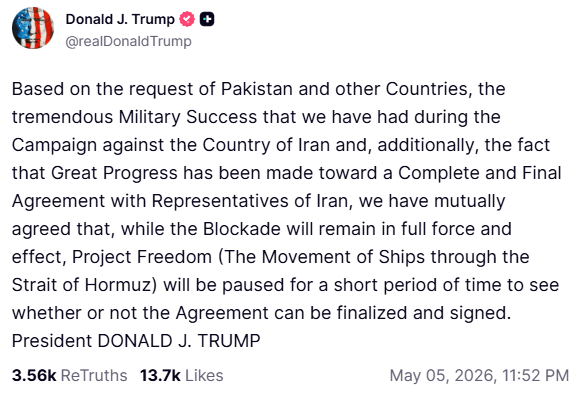

Yesterday’s dominant narrative was the announcement from US President Trump to pause Project Freedom, an operation to escort vessels through the Strait of Hormuz. I expected it to last a little longer, if I am honest. For the life of me, how does one trade this market right now or position it in a portfolio, given the on-off nature of the situation?

As you can see below, in a Truth Social post, Trump said the initiative would be suspended for a ‘short period’ while negotiations with Tehran continued. I feel that Trump clearly wants an off-ramp here, but Iran may not be letting him off the hook so easily, at least not without concessions and war reparations.

Markets responded ‘constructively’ to the news, with risk catching a bid and remaining in place this morning. US stock benchmarks closed higher across the board on Tuesday, with the S&P 500 and Nasdaq 100 refreshing all-time highs of 7,273 and 28,065, respectively.

From my perspective, the tone has shifted from unease to one of watchful optimism. Whether this sanguinity is warranted is difficult to assess at this point, given that Iran’s President dismissed US demands as impossible a couple of hours before Trump’s post hit the wires.

Overnight in Asia, Samsung Electronics also crossed the US$1 trillion market capitalisation mark, making it only the second Asian company after TSMC to do so, with shares up more than 13% in Seoul as the KOSPI finds acceptance north of the psychologically important 7,000 level.

Divergence between stocks and bonds

The divergence between stocks and bonds warrants attention. US Treasury yields were lower across the curve yesterday, yet the bond market is not telling the same story as the equity market. Supply remains relentless, with gross issuance exceeding half a trillion dollars weekly. With pricing power returning to corporate balance sheets, the inflationary backdrop remains uncomfortable for duration.

Simply put, stock investors feel good, while the bond market is concerned about excessive government debt and elevated inflationary pressures.

Oil lower, Yen eyed

Oil prices finished yesterday’s session in the red; spot Brent crude fell 3.3% to US$110.3/barrel, while WTI dropped to US$102.89. Both benchmarks are also on the ropes this morning, with the latter now trading near US$100. Despite Trump’s recent announcement – and reports that at least one vessel transited the Strait under US military escort – the structural energy problem remains far from resolved.

While the USD concluded Tuesday pretty much unchanged, the US dollar index is under pressure in early Europe this morning as markets assume a more risk-on environment. The JPY is also worth watching closely, rallying approximately 1% to around ¥156.00 against the USD in Asia amid speculation of further intervention by the BoJ, which reportedly spent some US$35 billion defending the currency last week.

Final thoughts

Markets, for now, are content to look through the geopolitical fog and lean into earnings momentum. The AI trade shows no signs of fatigue; Samsung’s milestone is a powerful symbol of that structural shift.

But the bond market’s reluctance to fully embrace the equity narrative, combined with an unresolved energy situation, means the path higher is narrower than the headlines suggest.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,