US Dollar Weekly Forecast: The Dollar stumbles, but the bigger picture remains unchanged

- The US Dollar reversed two consecutive weekly advances.

- Discouraging data and the USD/JPY sell-off were behind the Greenback’s drop.

- Next of note on the US docket will be the ISM Services and FOMC Minutes.

The week that was

The US Dollar (USD) has come under fresh downward pressure this week. Indeed, the US Dollar Index (DXY) could not sustain its earlier advance past the 101.50 level, succumbing to fresh bearish pressure in the latter half of the week on the back of disappointing labour market data and the marked decline in USD/JPY.

On the latter, Japanese authorities maintained their verbal intervention, despite growing scepticism among investors. It is worth recalling that the so-called “line in the sand” initially was around 160.00 and has been subsequently postponed to 161.00, 162.00 and maybe 163.00.

Anyway, bets that the Federal Reserve (Fed) might hike rates later in the year remain steady, which should offer a decent floor to the buck on occasional dips.

Fed officials keep inflation firmly in focus

Federal Reserve officials spent the week trying to stress the hawkish tone set at last month’s policy meeting. Speaking at the European Central Bank (ECB) Forum in Sintra, Chair Kevin Warsh said that restoring price stability remains the Fed’s top priority, even as he acknowledged that inflation risks and expectations have eased a bit in recent weeks. He stressed that prices remain too high and made it clear the central bank has no intention of tolerating inflation persistently above its 2% target.

Warsh also painted a constructive picture of the US economy, pointing to a resilient labour market, solid supply-side conditions and signs that potential growth may be improving. He devoted considerable attention to artificial intelligence, describing the current AI boom as being in its "first or second inning" while arguing that it remains too early to determine whether the technology will ultimately prove inflationary or disinflationary. On the institutional side, he reaffirmed the Fed's independence and confirmed that reviews of its communications framework, forecasting models and policy tools remain underway.

Governor Beth Hammack echoed many of those themes earlier in the week. She argued that inflation remains broad-based rather than solely driven by energy prices, highlighting persistently elevated core and services inflation as evidence that underlying price pressures remain too strong. She said higher rates pose a risk to the broader economy, but she also suggested that the Fed may need to consider raising them further if consumer demand remains strong and current policy is not restrictive enough.

All in all, this week’s Fedspeak gave little reason for markets to change their views of the current policy outlook. While officials acknowledged some tentative improvement in the inflation picture, both Warsh and Hammack made it clear that bringing inflation sustainably back to target remains the Fed's primary objective, leaving the door open to further tightening should price pressures fail to moderate.

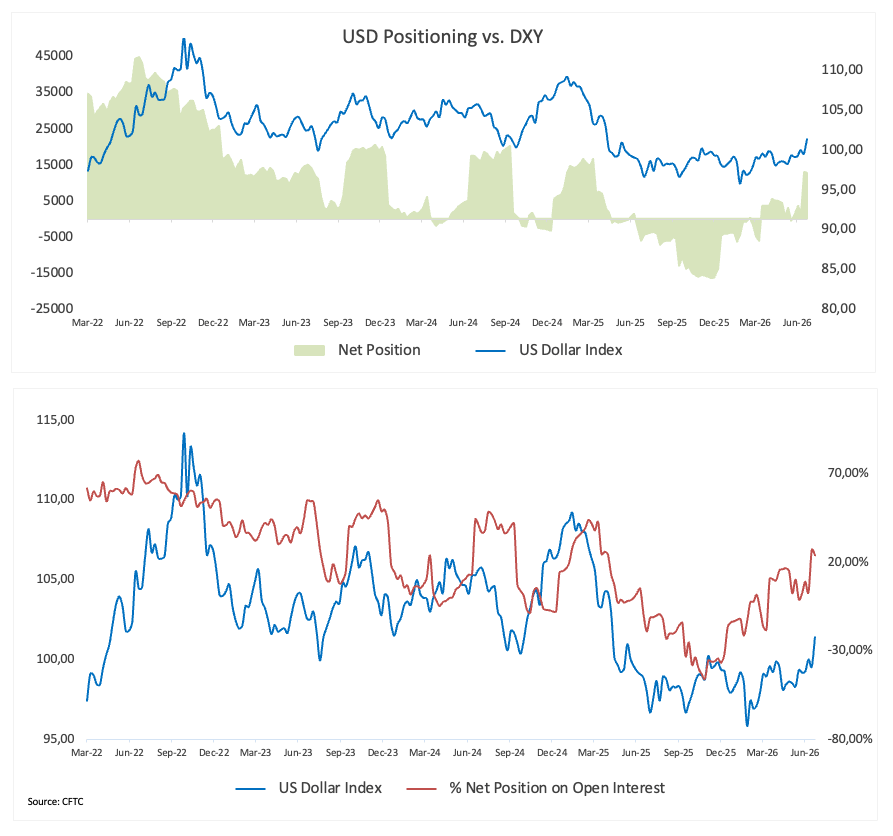

Dollar bulls return; positioning remains far from crowded

Speculative positioning in the US Dollar changed little in the week ending June 23, with net longs edging down marginally to 12.9K contracts from 13.2K the previous week. After the steady rebuilding of bullish exposure seen over the past month, the latest CFTC data suggest investors have entered a more cautious phase, with positioning broadly stabilising rather than extending higher.

The weekly change was negligible, with net positioning easing by just 269 contracts. Even so, the broader trend remains constructive, as speculative accounts have added just over 12K contracts to their net long exposure over the past four reporting weeks. Open interest, meanwhile, rose to 54.9K contracts from 49.4K, suggesting new participation despite little change in overall positioning.

Historical positioning metrics support the view that the Dollar is not a crowded trade. The current net position is at the 57th percentile of its five-year range and the Speculative Exposure Index is at 24%, the 49th percentile. The readings suggest speculative sentiment has rebounded from depressed levels earlier this year but is still near its historic average.

Overall, the latest CFTC data shows a slowly rebuilding bullish Dollar exposure that lacks strong conviction. Positioning is constructive but balanced, with plenty of room for further accumulation if incoming macroeconomic data and Fed expectations continue to favour the Greenback.

Inflation remains the hot topic

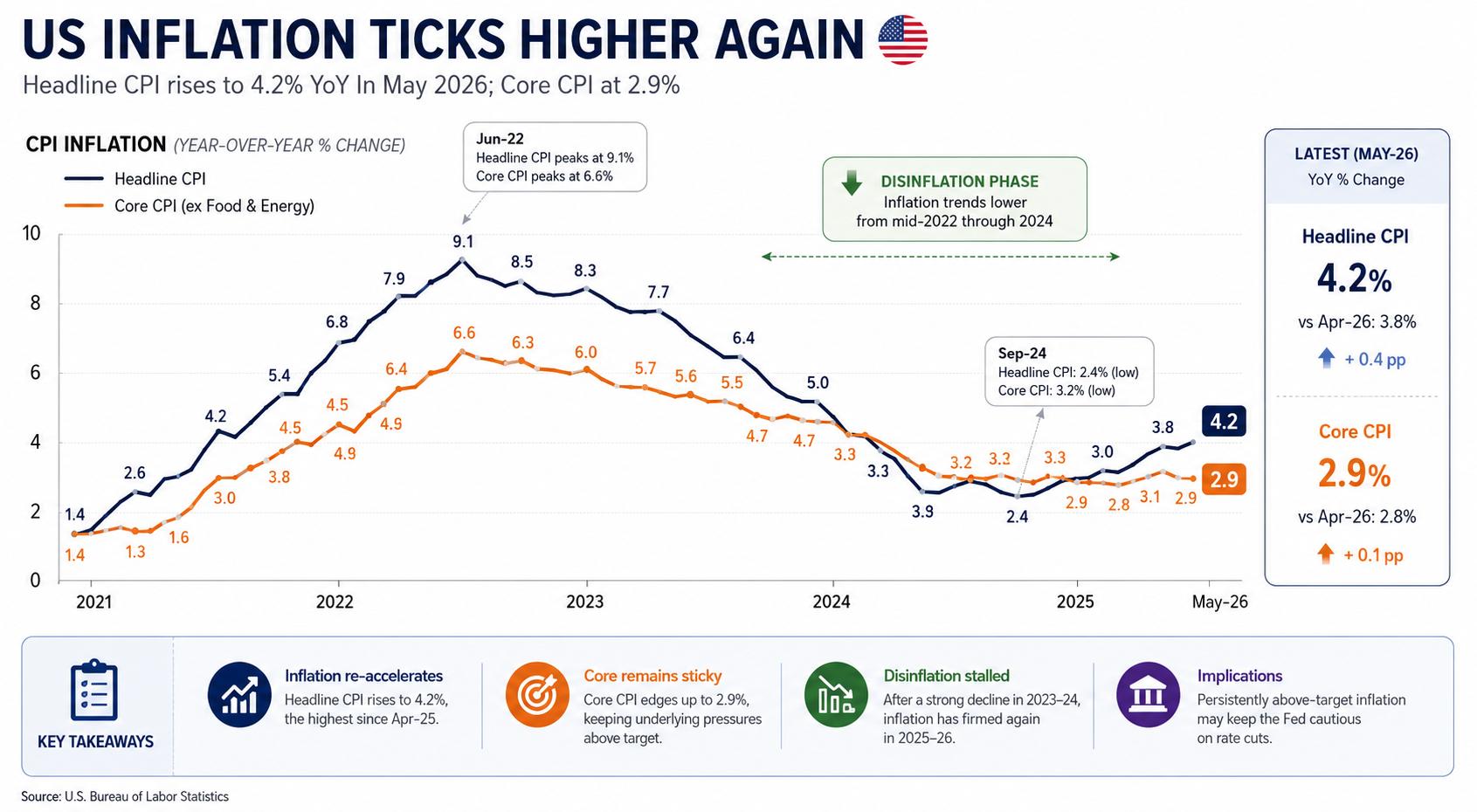

US consumer inflation came in hotter than expected in May, with headline CPI accelerating to 4.2% YoY from 3.8% in April and core inflation inching higher to 2.9% from 2.8%. The latest Personal Consumption Expenditures (PCE) report delivered a similar message, reinforcing the view that underlying price pressures remain more persistent than many had anticipated.

The US-Iran agreement has triggered a sharp reversal in crude Oil prices, with West Texas Intermediate (WTI) retreating toward the $68.00 region per barrel and erasing most of the geopolitical risk premium built up during the Strait of Hormuz tensions.

However, the delayed effects of US tariffs are only now beginning to filter through supply chains and consumer prices, raising the risk that inflation remains stickier than expected.

Taken together, it is precisely the backdrop markets had hoped to avoid: resilient inflation at a time when the narrative of US economic exceptionalism remains firmly intact.

A labour market that loses its shine… and USD/JPY

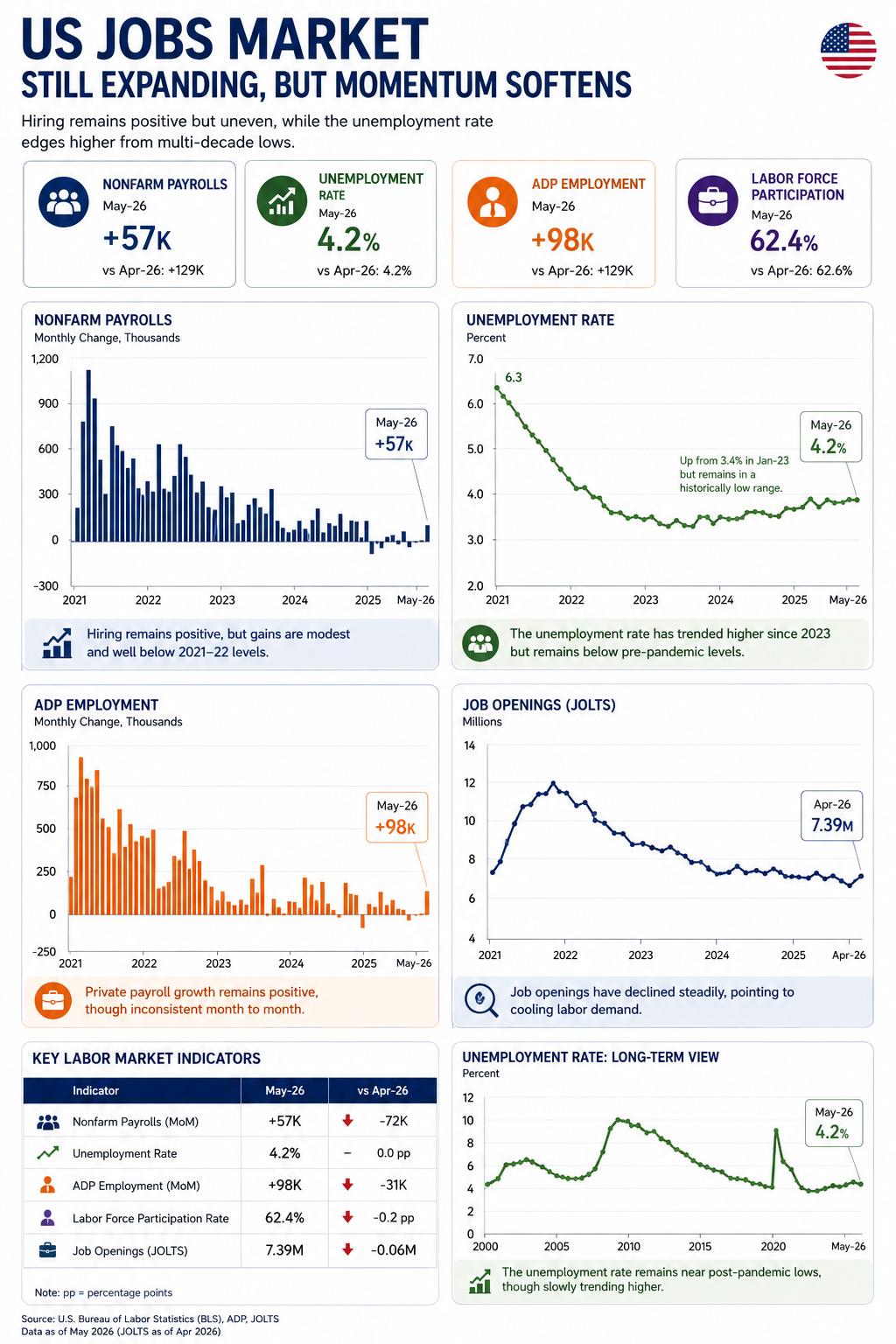

A big chunk of the Greenback’s renewed weakness has come after disappointing prints from the June Nonfarm Payrolls (NFP), showing the US economy added just 57K jobs, while the previous month’s revised reading went down to 129K from 172K.

The only positive is that the jobless rate ticked lower to 4.2% (from 4.3%), although this improvement may be partly due to a downtick in the participation rate.

However, Chair Warsh's reluctance to emphasise the performance of the domestic labour market has left market participants wondering whether these results have significantly impacted the buck’s price action.

That said, the severe sell-off in USD/JPY could be “the” culprit, as the spectre of FX intervention by the Ministry of Finance (MoF) to support the beleaguered Yen has been hovering over markets since spot broke above the 160.00 threshold.

What’s next?

Attention now shifts to next week's release of the FOMC Minutes of the June gathering, where the FOMC kept interest rates unchanged and delivered a hawkish message. Additionally, the ISM will publish its Services PMI gauge for the month of June.

Beyond the data, investors will continue to track developments in the Middle East as well as comments from Fed officials.

Higher for longer: markets rethink the Fed

Until the war in Iran began, investors operated under a relatively simple assumption: the Federal Reserve's next significant policy move would eventually be towards lower interest rates.

That assumption is becoming increasingly difficult to defend.

Sticky inflation, resilient economic activity, elevated energy prices and renewed supply-chain disruptions have all complicated the path back toward policy easing. More importantly, Fed officials no longer appear convinced that inflation will continue moving sustainably lower without monetary policy remaining restrictive.

None of these factors necessarily signals that another rate hike is imminent. It does, however, suggest that the bar for policy easing has risen considerably, while discussions about the possibility of further tightening have quietly returned to the conversation.

For the US Dollar, that shift matters. Expectations that interest rates will stay higher for longer should continue to underpin US Treasury yields and provide a supportive backdrop for the Greenback.

The Dollar's best friend: Persistent inflation

If recent months have taught investors anything, it is that bringing inflation down from very high levels is one challenge; eliminating the final leg of price pressures is another altogether.

That may be the US Dollar's greatest source of support in the months ahead.

Markets appear to have underestimated just how difficult the final stage of the inflation battle was always likely to be. As long as underlying price pressures remain stubbornly elevated, a prolonged period of restrictive monetary policy is likely to keep favouring the Greenback.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.