Poland’s inflation surprises to the downside as odds of rate cuts rise

Inflation came in lower at the beginning of 2025 due to the new CPI basket and revisions to the January reading. With new CPI weights and more realistic assumptions on electricity prices, inflation could return to the target range later this year rather than next year's third quarter as the NBP expects. We could see rates being cut in the second half of 2025.

CPI lower than initial estimates

CPI inflation totalled 4.9% year-on-year in February (ING: 5.4%; consensus: 5.3%). That's the same pace that we saw in January, following a downward revision from 5.3% YoY. Our forecast of price growth of 0.3% month-on-month materialised, but the difference in annual growth stemmed from an update to the CPI basket and a downward revision of the January reading.

In February, goods prices went up by 4.3% YoY and services prices increased by 6.6% YoY, compared with 4.2% and 6.8% respectively in January. Upward pressure on annual CPI was generated by prices of food and non-alcoholic beverages, which rose by 6.2% YoY vs 5.5% YoY in January. At the same time, fuel prices had a disinflationary impact as gasoline prices dropped by 2.6% YoY in February after remaining stable (0.0% YoY) in January.

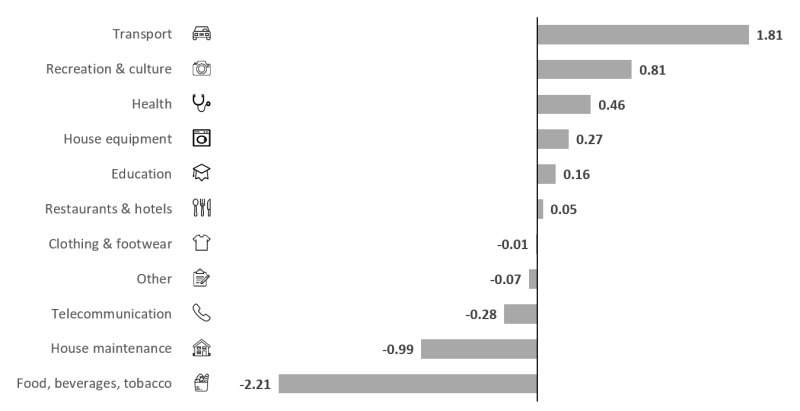

Surprisingly large changes to the basket

Every year in March, Poland's StatOffice updates CPI basket weights to reflect changing patterns of consumer outlays. This year, the changes were of higher magnitude than we've seen in the past. The biggest decline was reported in food and non-alcoholic beverages (down by 1.76 percentage points to 25.87%) as Poles proved quite frugal when it came to spending on necessities last year.

Substantial declines also took place in costs linked to housing (down by 0.99ppt) as energy prices were frozen in the first half of 2024. The share of energy linked to housing in CPI declined to 11.08% from 11.8% in 2024.

We did see a notable rise to 11.05% from 9.24% previously for transport, despite a decline in fuel outlays in the CPI basket by 0.6ppt to 5.5%. This reflects an impressive increase in the share of transport equipment, which nearly tripled to 3.4% in 2025 vs 1.2% last year. This development is in line with retail sales data pointing to strong momentum in passenger car purchases last year.

Based on the available data, we estimate that core inflation excluding food and energy prices eased to about 3.7% YoY in January and February, from 4.0% YoY at the end of last year. Official data on core inflation from the National Bank of Poland will be published next week. The share of core inflation in overall CPI increased to 57.55% from 54.47% in 2024.

Changes to CPI basket weights in 2025 vs. 2024

% of CPI

Source: GUS.

Inflation outlook more favourable than presented in the March NBP projection

We see a peak in inflation in March closer to 5% YoY than 5.6% YoY as we'd previously expected. We will enter a higher statistical base from April due to the reinstatement of VAT on food from the beginning of the second quarter.

We estimate that in the second quarter of 2025, inflation will be relatively stable around 4.5% YoY, and the third quarter will bring a further decline to the region of 3.0-3.5% YoY. In the year's final quarter, we expect inflation in the 3.0-3.5% YoY range, while the latest NBP projection sees inflation in this period at 4.8% YoY.

Another important difference between our estimates and those from the NBP is electricity prices in the fourth quarter of 2025. We do not expect an increase in electricity bills after the expiration of the cap price, while the central bank expects a spike to add 0.7ppt to CPI.

Rising odds of rate cuts later this year as MPC grows more divided

NBP President Adam Glapinski continues to present a hawkish stance but updates to the CPI weights and the inclusion of lower electricity tariffs should shift the inflation path downward in the next NBP projections. According to our forecasts, inflation returning to target should occur sooner – i.e., around the final quarter of this year rather than in 2027 as indicated by the March projection. The discussion within the MPC about rate cuts will intensify in the coming months, and the likelihood of our scenario of interest rate cuts occurring in the second half of this year (50-100bp) appears to be rising.

Read the original analysis: Poland’s inflation surprises to the downside as odds of rate cuts rise

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.