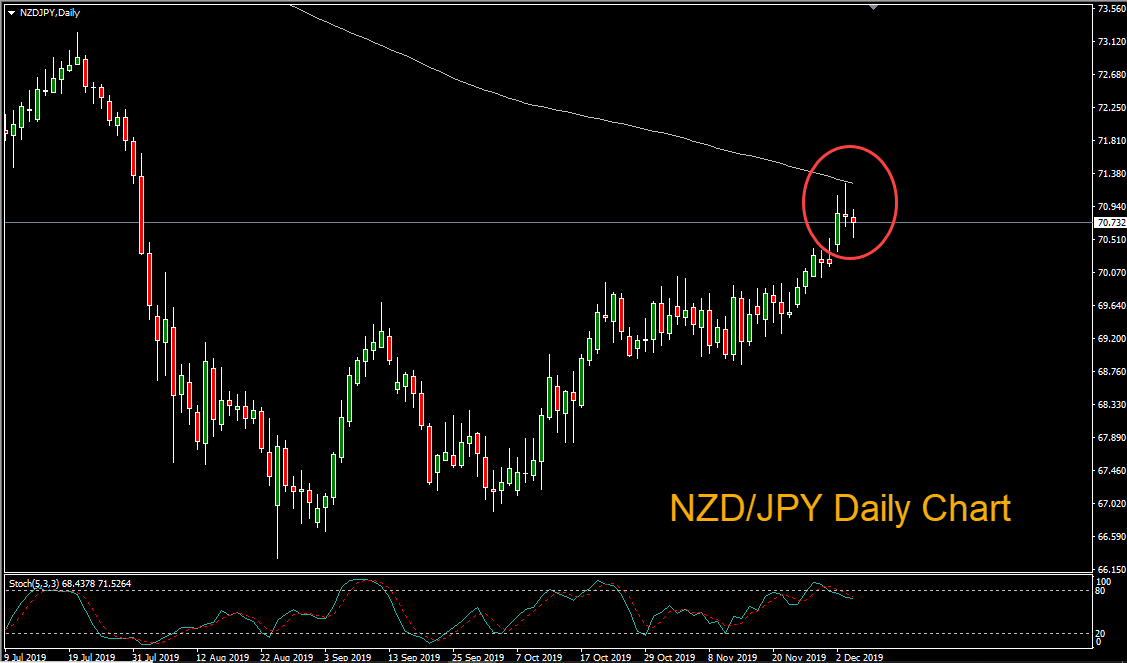

Pin Bar Pattern Forms off Resistance in NZD/JPY

A pin bar reversal pattern formed on the NZD/JPY daily chart, after price reached the key resistance level of the 200-period simple moving average in Monday’s trading session. Additionally, stochastics crossed below the 80 level, lending confirmation to the bearish scenario.

From a fundamental perspective, the Kiwi was pressured after the Australian Bureau of Statistics reported on Wednesday that the Australian economy expanded by a weaker-than-expected 0.4 per cent through the September quarter. Annual growth increased to 1.7 per cent, but remained below trend.

Meanwhile, the markets reeled after President Trump’s comments on Tuesday, suggesting that a trade deal with China might not be finalized until after the 2020 presidential election in November. Speaking to reporters in London at the NATO summit, Trump said:

“In some ways, I like the idea of waiting until after the election for the China deal, but they want to make a deal now and we will see whether or not the deal is going to be right.”

The statement marked a reversal of the upbeat stance last week, when Trump said that that the United States and China were in the "final throes" of negotiations, signaling that the trade war could be coming to an end. On Tuesday, stocks sold off sharply and money flowed out of higher risk emerging market currencies and into safe havens such as the Japanese Yen and gold. As China is New Zealand’s largest trading partner, downbeat news on the US/China trade war is especially negative for the Kiwi.

Author

Dan Blystone

TradersLog.com

Experience Dan Blystone began his career in the trading industry in 1998. He worked as an arb clerk on the floor of the Chicago Mercantile Exchange (CME), flashing orders into the currency futures pits.