Payrolls next Friday set to overshadow inflation data

Outlook

Today the US reports July PCE income and consumption plus inflation, the balance of trade in goods, retail and wholesale inventories (important because of pre-tariff overbuying), the final U Mich consumer survey and Canada’s Q2 GDP, forecast to be negative.

We are not supposed to worry about PCE today, but that’s not true. If the service sector is the culprit again, and services are relatively unaffected by tariffs, it means inflation is embedded. Core could easily come in at 3%. How will the Fed view that?

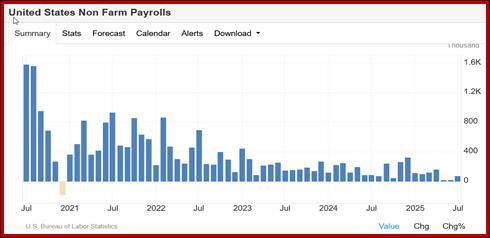

Then there is payrolls next Friday. This is supposed to overwhelm the inflation data. The Reuters polls forecasts 78,000 jobs (vs. 73,000 in July), plus those revisions to prior months that freaked out everyone. Okay, the labor market is cooling, and even if hardly a catastrophe, one strategist says "It would take very broad-based strength in the report in order to get the Fed to rethink the idea of moving rates lower. “ See the chart.

In other words, the Fed is not data-dependent this time. Neither is Fed member Waller, who repeated at the Miami Economic Club that the Fed needs to cut in Sept and if the jobs and inflation data is soft enough, by more than the standard 25 bp.

Note that there is a lethal gas-emitting data swamp roiling with different information about the drop in foreign-born workers, which may or may not mean the labor force is not adequate to keep the employment rate steady. As it is, it looks like the labor force is shrinking, most likely due to the Trump crackdown on anyone brown, legal or not. Here is the dense para from Reuters:

Lower jobs breakeven: Falling net migration has likely cut by two thirds the 'breakeven' monthly payroll benchmark - the number of jobs the economy needs to add to keep the jobless rate steady, reckons St. Louis Fed economist Alexander Bick. Data from the last three months suggests a breakeven below 50,000, and if employment growth is revised downward again when the August jobs report is released on Sept 5, "it would support the low end of our estimate range - 32,000 jobs - being closer to the mark".

In a nutshell, the true data supports the doves.

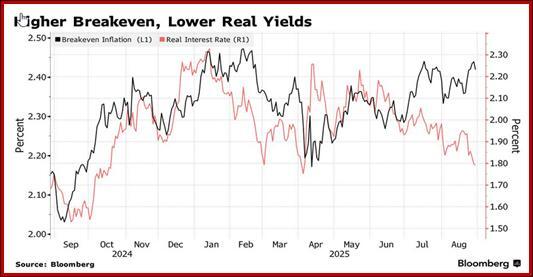

We guess that the Trump assault on the Fed’s independence is the top factor, not the data. Bloomberg points out “The 10-year breakeven rate reached a six-month high of 2.46% Wednesday, driven by a decline in yields on inflation-protected securities as demand for hedges increased.”

Given that you need a PhD in math and another in physics to use the TIPS market and volume in low compared to the primary bond market, we are not sure this isn’t stretching things. But the point is probably valid—the market is starting to acknowledge that OF COURSE tariffs are inflationary. See the Bloomberg chart. But also see the TIPS ETF, which has yet to match the high from March. Inflation fear is not yet stalking the land.

This leads to the loss of Fed credibility if Trump gets control. Credibility in what way? Surely it’s the ability to manage inflation in the eyes of the public and the financial sectors.

Forecast

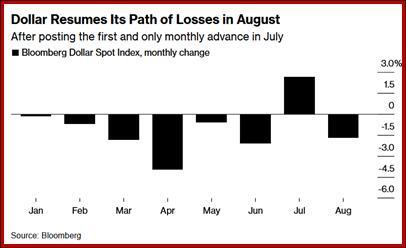

We continue to get the dollar chopping up and down. The dollar index yesterday closed up from the day before but failed to match the high. Very messy. See the chart of the Bloomberg version of the dollar index. Bloomberg writes that “Wall Street” now thinks the dollar has nowhere to go but further down, on the Sept rate cut and Fed war. This chips away at the dollar’s safe haven status and the dollar needs to deliver a “premium” for outsiders to buy it.

Oh, dear. When a prime site like Bloomberg summarizes the position like this, that’s precisely when we need to question it. Consensus is all fine and good, but what on earth caused the July bump and why should we not expect it to happen again?

Go back to our euro chart showing the triangle with support/resistance at 1.1575 to 1.1750. We say an authentic breakout is needed before we can say the dollar is toast. Treasury auctions are not showing foreigners departing the dollar in droves.

Besides, at some point, the inflation-obsessed bond vigilantes are going to kick in and deliver that premium. To say the dollar is downward-facing for the next 6-8 months, as Bloomberg does, is to assume ceteris paribus, nothing else is changing. But something is always changing.

What is not changing is the US still with the biggest, most varied and most resilient economy and financial markets. Alternatives are not appearing. Granted, it’s early days, but the idea of the euro taking over most-favored status is not developing, in part of the fiscal issues and also the political (France). So, don’t be too sure of an endless downward trajectory for the dollar. Maybe it really is so strong not even Trump can wreck it.

Ahead of the US holiday on Monday, expect some pullbacks as we already see in equity futures. But don’t assume the Big Picture—dead dollar—will come right back.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat