Overview of US session last Friday

US session: Bullard, Bostic, Barkin then a bounce

Markets

-

JPY leads, NZD lags.

-

Gold down $14 to $1979.

-

US 10-year yield down 2.8 bps to 3.37%.

-

WTI crude oil down 64 cents to $69.32.

-

S&P 500 up 22 points to 3971. On the week up 1.4%.

The mood was poor at the opening of North American trade, as concerns about banks, particularly Deutsche Bank, hung over the market. Regional US stocks were also under pressure, while bonds were in high demand. As a result, as US 2-year rates touched post-SVB lows, traders sought safe havens in the US dollar and yen.

The mood changed as Fed speakers and data were released. The PMIs, in particular, served as a reminder that the majority of US economic data has surprised to the upside this year, with no tangible signs of a slowdown; in fact, the reverse is true.

This resulted in some bond selling, and the dollar began to gradually trim gains ex-JPY. Later in the day, equities took a more pronounced swing, following regional bank shares once more. The news that Yellen would be meeting with regulators was positively received, but it may have raised expectations of weekend action. If nothing happens on Monday, this might lead to disappointment.

Overall, it was a volatile week, and no one will be unhappy to see the weekend arrive. The intrigues of Fed Week and nonstop banking news have left the market in need of a break.

The weekly charts show the yen making good gains, but it paused today and began to reverse. That is where the emphasis will remain.

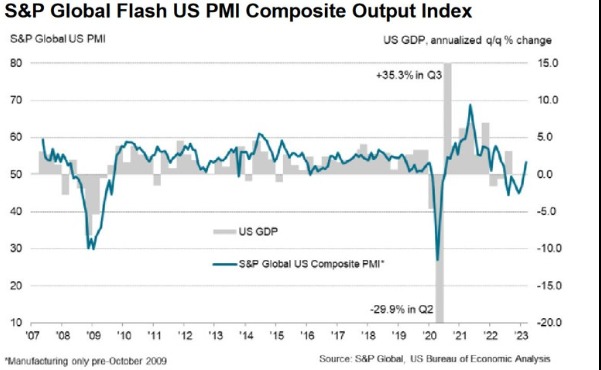

S&P Global March flash US services PMI 53.8 vs 50.5 expected

-

Prior was 50.6.

-

Manufacturing 49.3 vs 47.0 expected.

-

Prior manufacturing 47.8.

-

Composite 53.3 vs 50.1 prior.

This is a hot number that highlights the Fed's inflation dilemma. Equities have dropped even more because of this.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, commented on the US flash PMI data:

“March has so far witnessed an encouraging resurgence of economic growth, with the business surveys indicating an acceleration of output to the fastest since May of last year. “ The PMI is broadly consistent with annualised GDP growth of around 2%, painting a far more positive picture of economic resilience than the declines seen in the second half of last year and at the beginning of 2023.

“The upturn is uneven, however, being driven largely by the service sector. Although manufacturing eked out a small production gain, this was mainly a reflection of improved supply chains allowing firms to fulfill backlogs of orders that had accumulated during the post-pandemic demand surge. Tellingly, new orders have now fallen for six straight months in manufacturing. Unless demand improves, there seems little scope for production growth to be sustained at current levels.

“In services, there are more encouraging signs, with demand blossoming as we enter spring. It will be important to assess the resilience of this demand in the face of the recent tightening of interest rates and the uncertainty caused by the banking sector stress, which so far only seems to have had a modest impact on business growth expectations.

“There is also some concern regarding inflation, with the survey’s gauge of selling prices increasing at a faster rate in March despite lower costs feeding through the manufacturing sector. The inflationary upturn is now being led by stronger service sector price increases, linked largely to faster wage growth.”

Canada Retail Sales for January 1.4% versus 0.7% estimate

-

Prior month 0.5% revised down to 0.0%.

-

Canada retail sales 1.4% versus 0.7% expected. (The preliminary estimate last month was at 0.5%).

-

Ex autos 0.9% versus 0.6% estimate. Prior revised to -0.7% from -0.6%.

-

The preliminary estimate for next month suggests a decrease of -0.6% February.

-

Retail sales excluding gasoline stations and fuel vendors and motor vehicle and part dealers rose 0.5%.

-

Retail sales increase in seven of nine subsectors represented 88.7% of retail trade.

-

Motor vehicles and parts dealers rose 3.0%. This was the six consecutive monthly increase. New car dealers rose is 3.0% which was the second largest increase since May 2022.

Gasoline stations and fuel vendors +2.9%. In volume terms though gasoline stations and fuel vendors fell -0.6% as gasoline prices increase 4.7% versus January. The rise in prices was due largely to refinery closure in the southwestern United States.

This month's gain was higher than the preliminary estimate of 0.5% from the previous month. However, the previous month's figure was sharply reduced to 0.0% from 0.5% previously reported. NOTE: The official estimate for February was calculated using responses from 51% of the companies polled. Over the previous 12 months, the average final review response rate for surveys was 89.9%.

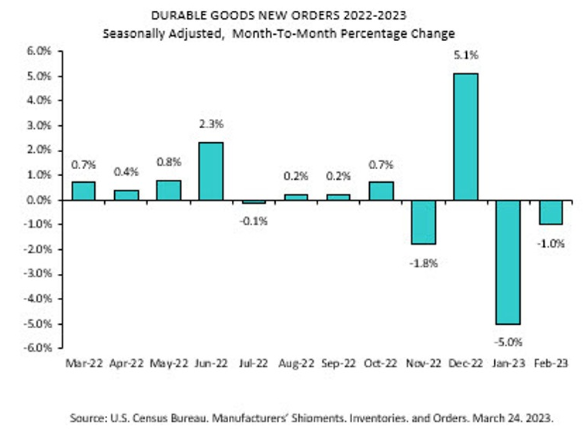

US February durable goods orders -1.0% vs +0.6% expected

-

Prior was -4.5% (revised to -5.0%).

-

Durables ex transportation 0.0% vs +0.2% expected.

-

Prior ex transportation +0.7% *(revised to +0.4%).

-

Capital goods orders non-defence ex-air +0.2% vs 0.0% expected.

-

Prior capital goods orders non-defence ex-air +0.8% (revised to +0.3%).

-

Core orders were somewhat higher, but the scale of the change negates all of the good news.

Fed's Bullard: Sees 80% chance financial stress abates

-

US remains in a position to see disinflation in 2023, will see if Fed needs to react more or not.

-

Expects Fed will be dealing more with the strong economy into the spring and summer months and not worrying as much about financial stresses.

-

Could be downside if financial stress gets worse and would react to that.

-

Wide variety of jobs data pointing to continued strong labour market.

-

In most likely scenario, Fed will have to 'ratchet up' more as financial stress abates and economy remains strong.

-

Sees 80% chance financial stress abates and discussion shifts back to inflation; a lower-probability outcome is recession.

-

Probability of global crisis from recent stress is low.

Here, I agree with Bullard, which puts me in an awkward situation.

He's not exactly hitting the table for rate hikes, which is unusual for him. It's more of a wait-and-see attitude, which is understandable.

Fed's Bullard: Inflation remains too high, macro data 'stronger than expected'

-

Inflation expectations relatively low, a good sign for disinflation this year.

-

US response to bank stress has been swift and appropriate.

-

Regulators can do more as needed to contain financial stress.

-

It's not uncommon for some firms to fail to adjust to changing financial conditions.

Bullard isn't generally bashful, but he's not saying much on the course of rates today.

Fed Barkin: The case for raising rates this week was pretty clear

In an interview with CNN, Richmond Fed President Thomas Barkin (nonvoting member in 2023) stated:

-

Case for raising rates this week was pretty clear.

-

Labour markets are tight.

-

People hate inflation. Inflation is unfair.

-

People want the Fed to get control of inflation.

-

Bringing inflation down creates better conditions for jobs.

-

The economy remains it too high that.

-

Every decision is hard and fully debated.

Fed's Bostic: Fed rate rise was not an easy decision

-

Inflation still too high, Fed needed to remain focused on that.

-

Clear signs the banking system is safe and resilient.

The Fed has exited the blackout period, so we can expect waves of commentary. Bostic had been hawkish, but he has since stated that he no longer believes that way. But it's something to keep an eye on.

Baker hughes US Oil rig count +4

-

Natural gas rigs unchanged.

-

Total rigs +4.

At some point, real discipline in the natural gas space would be welcome, but many players are hoping to ride out the low prices for the time being and benefit from a cold winter in 2023-24 or the build-out of LNG in the second half of the decade. Overall, LNG will be a significant tailwind, but this year has shown that it is simple to bring on additional supplies, so it may be a long time before we see $9 gas again.

Author

ACY Securities Team

ACY Securities

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis. The key pi