US labour market: Overall well balanced

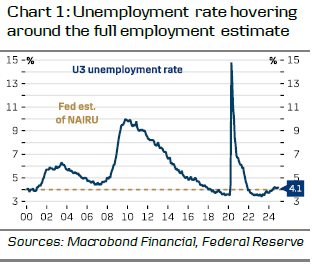

The cooling trend observed in the US labour market since the late 2022 appears to have paused, but at a level where the labour market generally remains well balanced. The December Jobs Report came in stronger than expected, with nonfarm payrolls ticking up by 256k (cons: 160k), corroborating solid job growth after hurricanes and strikes distorted past readings. Prior figures were revised modestly down by a cumulative 8k. The unemployment rate edged down somewhat to 4.1%, hovering around most fullemployment estimates (chart 1).

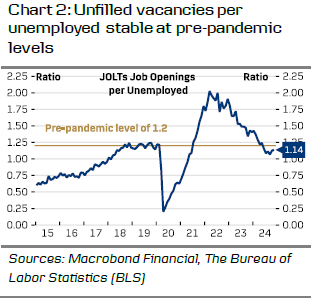

The November JOLTs report provided some mixed signals, as job openings beat expectations (8.1m, cons: 7.7m, prior: 7.8m) but hiring slowed and involuntary layoffs ticked slightly higher. Altogether, it seems labour demand remains at healthy levels, with job openings reaching the highest level since May 2024. The ratio of unfilled vacancies per unemployed is stable, close to its pre-pandemic average (chart 2).

Wage growth declined to 0.28% m/m SA in December (prior: 0.4%) with the yearly measure at 3.9% y/y. For now, wage growth remains somewhat elevated, but with past years’ solid productivity gains, firms’ unit labour costs have remained in check. Recent signs of consumers’ inflation expectations ticking higher – both 1y and 5y according to data from the University of Michigan – could pose an upside risk to labour costs if workers begin to demand higher wages again. For the time being, Atlanta Fed’s estimation has suggested that job switchers no longer earn unusually high wage increases relative to those staying at their jobs.

Leading indicators provide a somewhat ambiguous picture. On the one hand, the ISM employment indices suggest that employment is weakening in the manufacturing sector but remains strong in services. Conversely, the PMI employment indices signal increasing employment across the board. We recommend interpreting the volatile data with caution.

Overall, data affirms the notion of well-balanced labour markets with no clear signs of overheating. This is good news for the Fed, and a key reason for why we still believe the Fed will cut rates in March despite the strong jobs report. However, conditions could become uncanny if labour markets begin to show signs of renewed tightness – particularly as the unemployment rate remains close to most full-employment estimates.

Weakening growth in labour supply, which was the backbone of past year’s stronger than expected macro environment, could pose two-sided risks to current labour markets conditions. BLS’ data shows that native-born labour supply growth stalled in 2024, and that immigration was the main driver of positive supply growth (chart 3). At the same time, a study from CBO suggest that 73% of the past year’s net immigration was undocumented workers – and as we have flagged before, inflow of undocumented immigrants already slowed in H2 of 2024. Importantly, while strong labour supply growth was one of the key reasons the US economy outperformed expectations last year and inflation continued to moderate – tighter labour supply could put upward pressure on labour costs, reigniting inflation concerns or forcing some companies to reduce staff.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.