Optimism on the Dollar: An Economic Driver and a Rider

Dollar strength since Election Day has signaled financial market confidence that expansionary fiscal policy will work. Yet, too much or too little movement in the dollar might challenge market optimism.

The Economics Iron Triangle: Dollar, Growth, Interest Rates

Economics is a science of interrelationships between markets, and the value of the dollar reflects the confluence of exchange rate, goods & services and credit markets. The value of the dollar is both a driver and a rider in economic activity.

Financial markets have discounted a combination of easier fiscal and tighter monetary policy. In an economy with a floating exchange rate and open capital markets, as associated with a Mundell-Fleming model, an easier fiscal policy/tighter monetary mix would typically be associated with a stronger dollar. This pattern adheres to a traditional economic framework. Yet, little of recent experience is anything like typical.

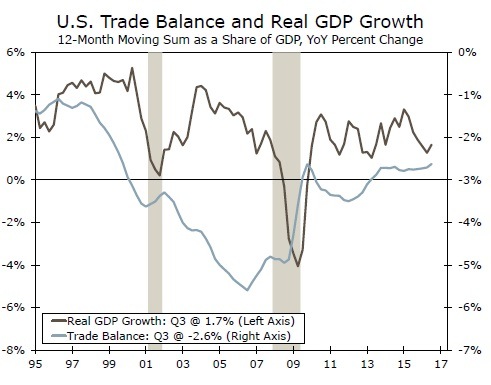

Going forward, policy and the character of this expansion have the opportunity to create a path for the dollar of moderate appreciation. This path would not too harshly limit growth in exports and GDP while also helping keep a lid on inflation through import prices. Moreover, concerns linking the trade deficit to the exchange rate may be overstated as growth, both here and abroad, plays a larger role than the dollar in determining trade deficits (top graph). The elasticity of import growth with respect to growth in domestic demand is much higher than the elasticity of import growth with respect to changes in the exchange rate–the same holds for export growth. Given the policy focus on boosting U.S. economic growth, a wider trade deficit would be expected to follow.

After Accounting For Growth: Dollar and Interest Rates

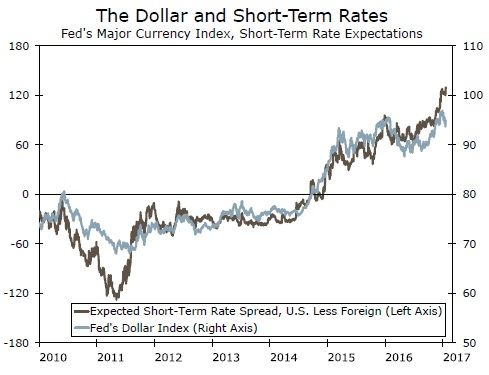

Divergence among global short-term rates has been a persistent phenomenon for some time. On the side of the U.S., the Fed raised rates in 2015 and increased the benchmark fed funds rate again in December 2016. With the labor market continuing to tighten and inflation trending up, the Fed will likely raise rates multiple times in 2017. Meanwhile, other major central banks, such as the Bank of Japan, Bank of England and the European Central Bank, have shown few signs of raising short-term interest rates in the near future. As illustrated in the middle graph, recent dollar strength follows the difference in relative interest rates.

Stronger Growth Drives Multiple Factors

A policy to pursue stronger growth also brings it with the prospect of drawing in capital from abroad that can finance economic growth as well as limit the rise in interest rates. Fiscal and monetary policymakers, however, will have to walk a fine line. Too much dollar appreciation would inhibit exports and boost imports, thereby exerting a drag on economic growth. A depreciation of the dollar, however, would lead to higher import prices and potentially losing hold of the inflation target. Economics is also a science of trade-offs, a fact policymakers will need to bear in mind moving forward.

Author

Wells Fargo Research Team

Wells Fargo