Only “Trump risk” left to lift the yen

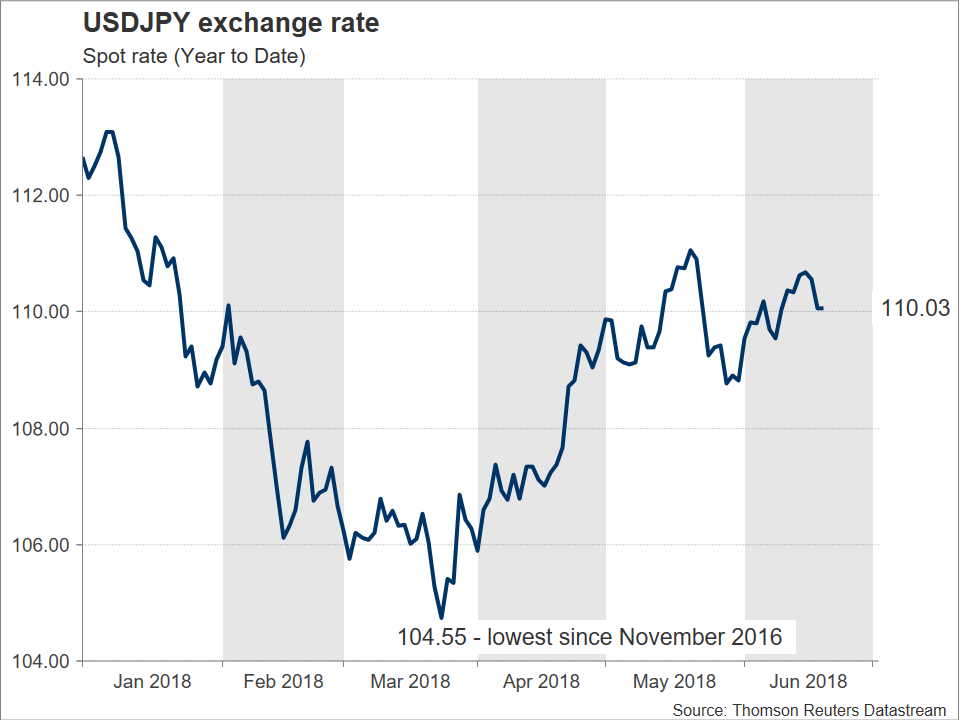

The yen appreciated by 3.9% versus the US currency in 2017, which marked the worst year for the greenback since 2003. During the first few months of the current year, the Japanese currency managed to build on last year’s positive momentum, in part due to rising market expectations for a Bank of Japan that is getting closer to normalizing policy. Indicatively, the dollar/yen pair touched its lowest since late 2016 of 104.55 on March 26. However, as we’re approaching the end of Q2 the BoJ normalization story has lost steam. Instead, it seems as if only safe-haven flows can prevent a rally in USDJPY.

As of late June, then yen remains the only major currency that is decisively trading in the green in 2018 against the dollar (the Norwegian krone is only marginally up versus the US currency during the same period). Specifically, at 110.03, dollar/yen is down by 2.3% year-to-date. However, and as evidenced by the chart below, the pair has been in an uptrend for almost the whole of Q2 and there are numerous factors supporting the view for a continuation of the trend in place.

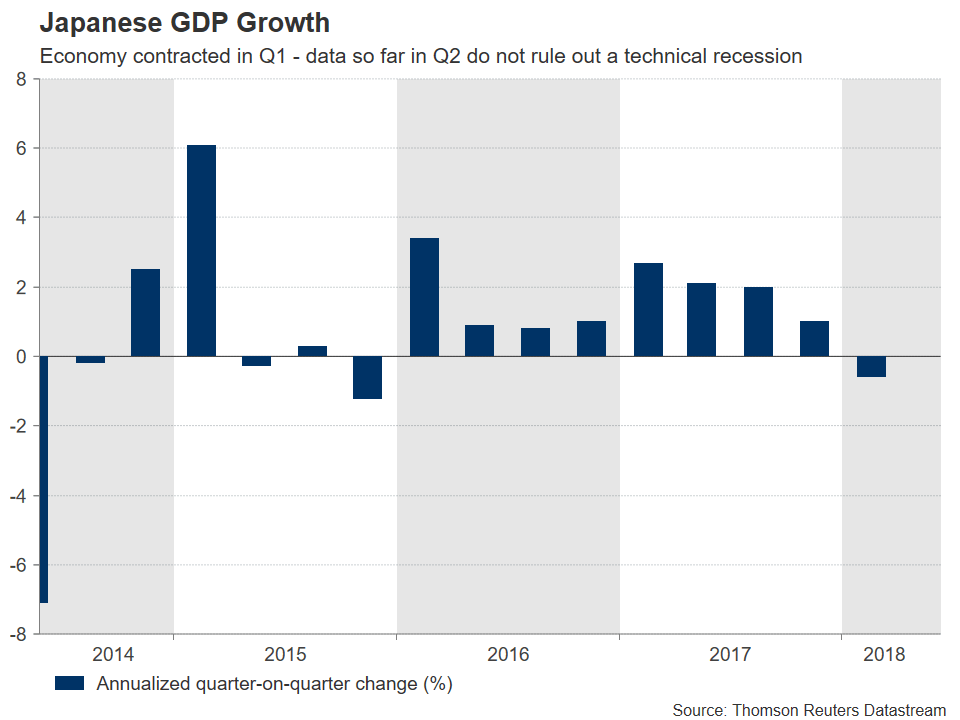

Firstly, economic fundamentals as reflected by recent data releases are not painting a rosy picture for the Japanese economy. After economic activity contracted in Q1, April’s industrial output and household spending numbers came in well short of analysts’ forecasts, with the latter recording its third straight month of negative growth in April. On the bright side, machinery orders strongly rebounded during the same month. Overall though, the figures out of Japan are such that they are not ruling out a technical recession – defined as two consecutive quarters of GDP contraction – in Q2.

Contrast the above with the situation in the US and the greenback emerges as the likely “victor” versus the yen: US releases feeding into GDP forecasting models are putting growth in the world’s largest economy at the 4-handle on an annualized basis during Q2, the highest pace since 2014. In particular, one such estimate derived by the Atlanta Fed’s GDPNow model, places the annual rate of expansion in Q2 at 4.7%.

Turning to monetary policy, in late 2017 - early 2018, the BoJ normalization story appeared so engrained in traders’ minds that they were much more willing to short the dollar/yen pair on the back of any hawkish-perceived comments by BoJ Governor Haruhiko Kuroda, compared to going long on remarks that cast doubt on monetary policy tightening expectations, pushing them way back into the future.

Fast forward to the present: market participants seem to have come to terms with a Japanese central bank that will remain ultra-accommodative for the foreseeable future; easing inflationary pressures have also contributed to this “cause”. Attesting to this is the fact that despite the BoJ once again reducing the amount of Japanese government bonds (JGBs) it will purchase as part of its operations in June, the markets are largely shying away from viewing this as tapering as they have in the past. Instead, they see it for what it is: achieving the BoJ’s target of a yield of around zero percent on 10-year JGBs happens to require the purchase of fewer bonds.

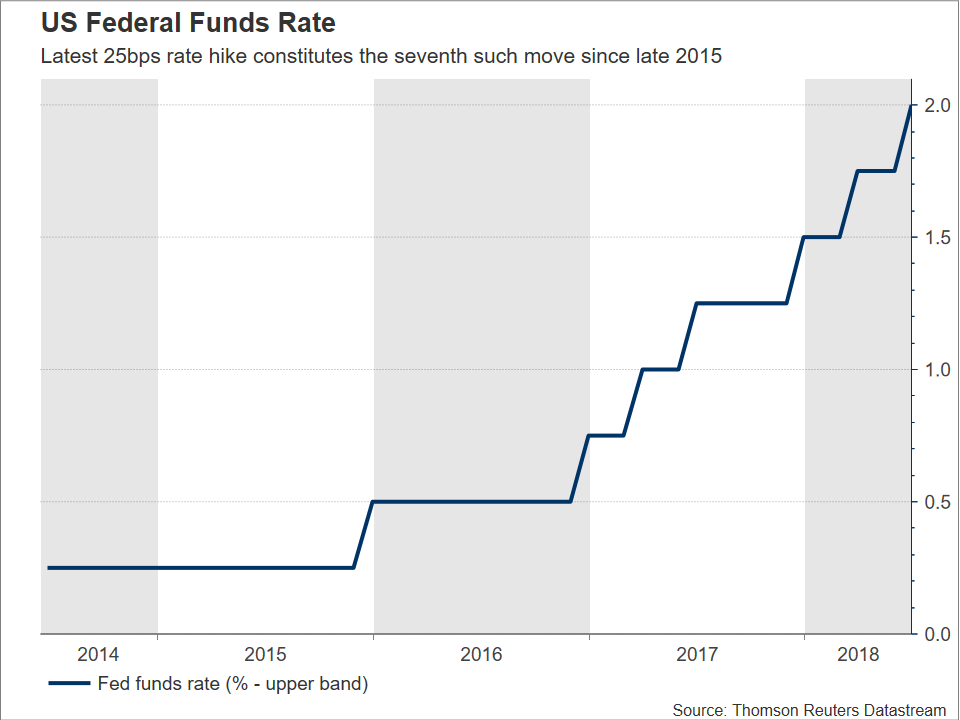

Again, contrast with the US: the Federal Reserve remains firmly on a path of policy normalization, having recently delivered its seventh quarter percentage point interest rate increase since it started hiking rates in late 2015. Meanwhile, the meeting concluding on June 13 saw FOMC policymakers tilting hawkish by revising their rate-path projections for 2018 to signal four rate increases in total, from three previously. Putting everything together, in the absence of a market shock, peak policy divergence between the US and Japan, translating into higher yield differentials and favoring a stronger USDJPY, has yet to materialize.

Case closed then? Should the growth trajectories of Japan and the US, as well as monetary policy divergence (of course the two are directly related), allow us to safely predict a dollar/yen that will be on the rise as the year unfolds? Yes and (partially) no: this is where “Trump risk” gets into the equation and complicates matters.

Japan is the world’s biggest creditor nation and there is a broadly held assumption that Japanese investors will repatriate funds in case of a crisis. This renders the yen a safe-haven harbor, gaining at times of heightened uncertainty. The US-China trade relationship has been put to the test numerous times over the course of the year, with the Japanese currency rising whenever Sino-US tensions intensified. The latest threat from US President Donald Trump for tariffs on an additional $200 billion of Chinese goods imported in the US is pushing the world’s two largest economies closer to a trade war.

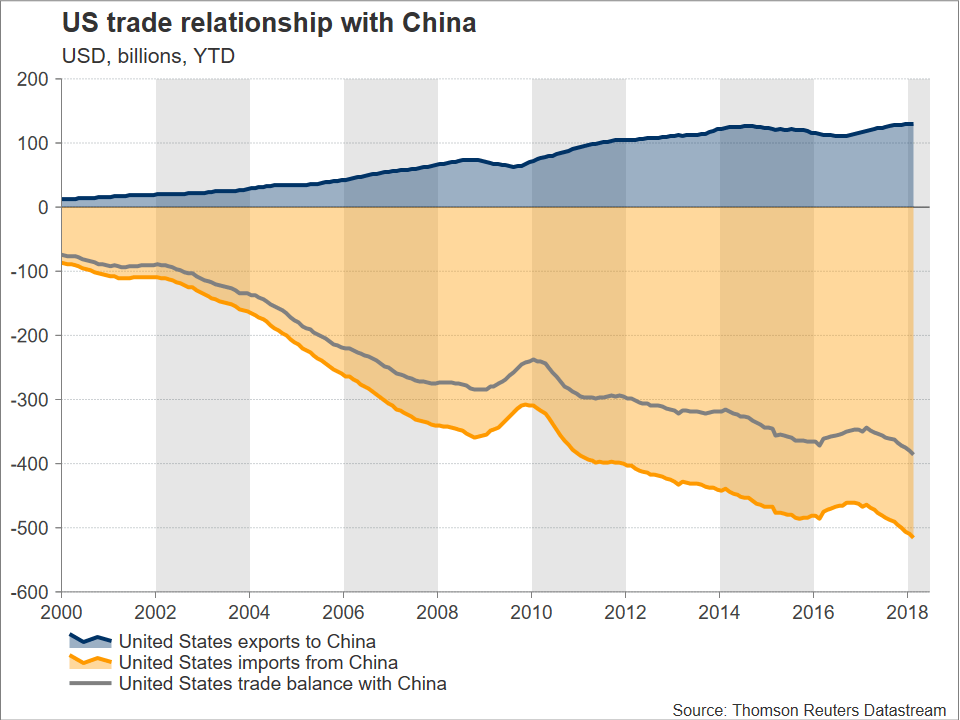

It has long been argued that the aforementioned trade spat does not have much room to run. The Trump administration’s rhetoric was seen as merely a negotiating tactic to generate leverage ahead of talks, and China’s disadvantage of having far more to lose in case of increased barriers to trade (see chart below), were enough to ease concerns over a trade war.

However, the US keeps on exerting pressure on China, and the latter – much to the surprise of many market commentators – responds in retaliatory fashion, at least up to now. A tit-for-tat escalation that will drive the situation out of hand is anticipated to lend support to the yen, driving dollar/yen even lower.

Overall on trade, it is clear that the risk for a full-blown trade war has dramatically risen lately. Despite this, given that such an outcome would be a “lose-lose” situation from an economic standpoint for China and the US, it remains an unlikely – tail risk – event.

Taking everything into account, and under a base case scenario that does not see a trade war materializing, if a projection for dollar/yen were to be made spanning until the end of Q3, then it would be one for an elevated pair. A dollar/yen piercing through the 112 handle, coming close to neutral year to date, should not be ruled out.

Author

Andreas holds an MSc in Finance from Warwick Business School in the UK and a BSc in Business Administration (Finance major) from the University of Cyprus.