One more time

Wild FOMC day is over, and markets are repricing the perceived fresh hawkishness when there was none really. It‘s nice to start counting with 5 rate hikes this year when taper hasn‘t truly progressed much since it was announced last year. The accelerated taper would though happen, and the following questions are as to hikes‘ number and frequency. I‘m not looking the current perceived hawkishness to be able to go all the way, and I question Mar 50bp rate hike fears. Not that it would even make a dent in inflation – as the Fed just stood pat, open oil profits are rising.

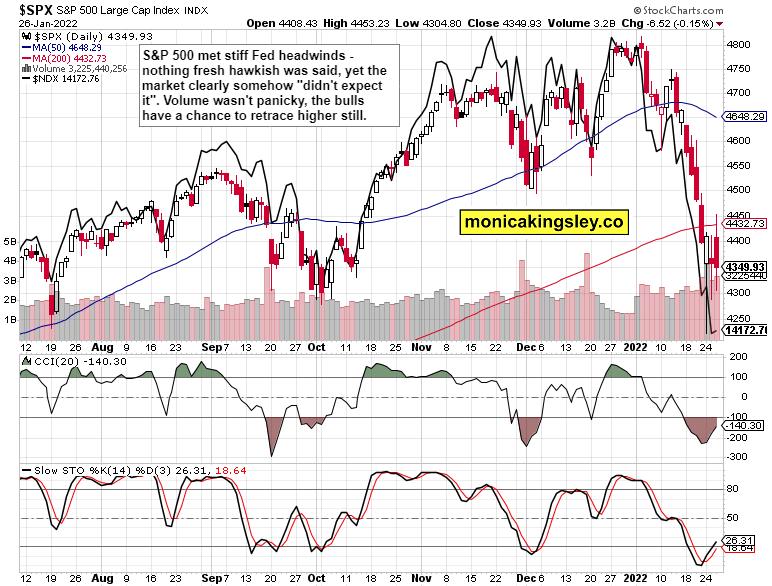

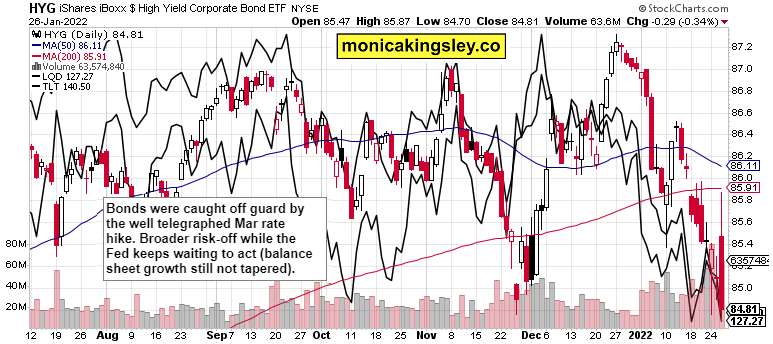

But stocks took a dive before recovering, carving out a fourth in a row lower knot – the bulls are invited to participate, and open stock market profits are moving up again. Also note the divergence between HYG trading at its recent lows while S&P 500 clearly isn‘t. The immediate pressure would be to go higher, and that concerns also copper, and to a smaller degree cryptos. All that‘s needed, is for bonds to turn up, acknowledging a too hawkish interpretation of yesterday‘s FOMC – key factor that sent metals down and dollar up. While rates would continue rising, as the Fed overplays its tightening hand, we would see them retreat again – now with 1.85% in the 10-year Treasury, we would overshoot very well above 2% only to close the year in its (2%) vicinity.

That just illustrates how much tolerance for rate hikes both the real economy and the markets have, and the degree to which the Fed can accomplish its overly ambitious yet behind the curve plans. Still time to be betting on commodities and precious metals in the coming stagflation.

Let‘s move right into the charts.

S&P 500 and Nasdaq outlook

Setback and reversal of prior gains - S&P 500 is though still carving out a tradable bottom. I‘m looking for the index to return above 4,400 and then take on the 4,500 point of control next.

Credit markets

HYG reversed, the panic is there – higher yields across the board without a clear risk-on turn holding. Today is a time for reprieve.

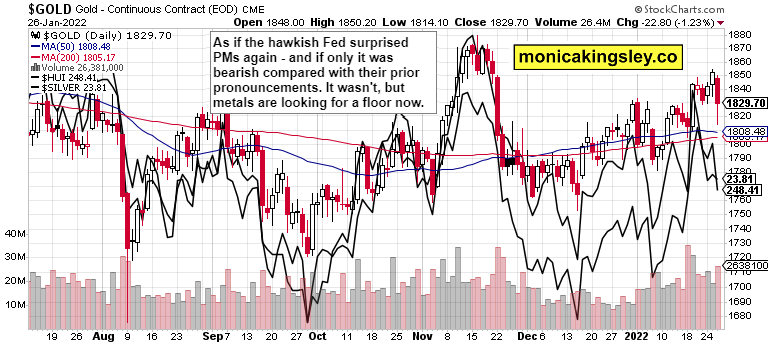

Gold, silver and miners

Gold and silver declined as yields moved sharply up and so did the dollar – but inflation or inflation expectations didn‘t really budge. The metals are anticipating the upcoming liquidity squeeze, which won‘t be pretty until the Fed changes course. Not that it truly started, for that matter.

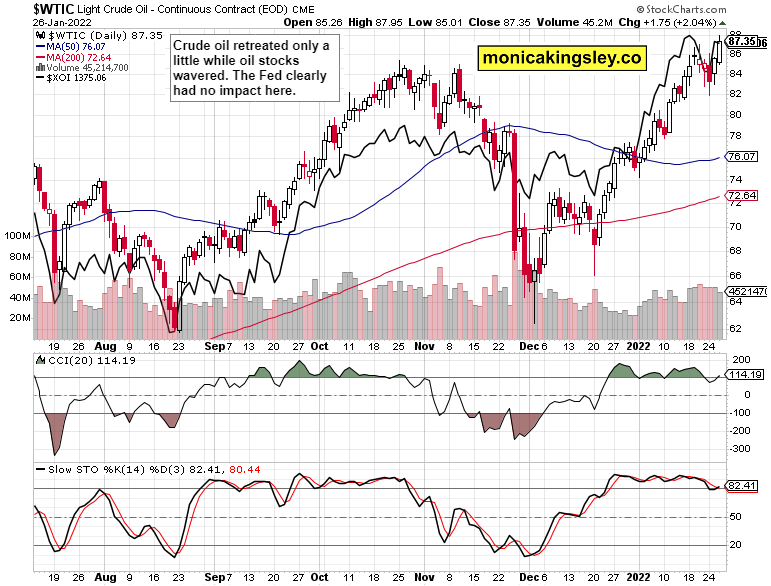

Crude oil

Crude oil bulls have confirmed they were back, and are ready for more – clearly not daunted by the Fed messaging, and that has implications for inflation ahead. It would really be more persistent than generally appreciated, I‘m telling you.

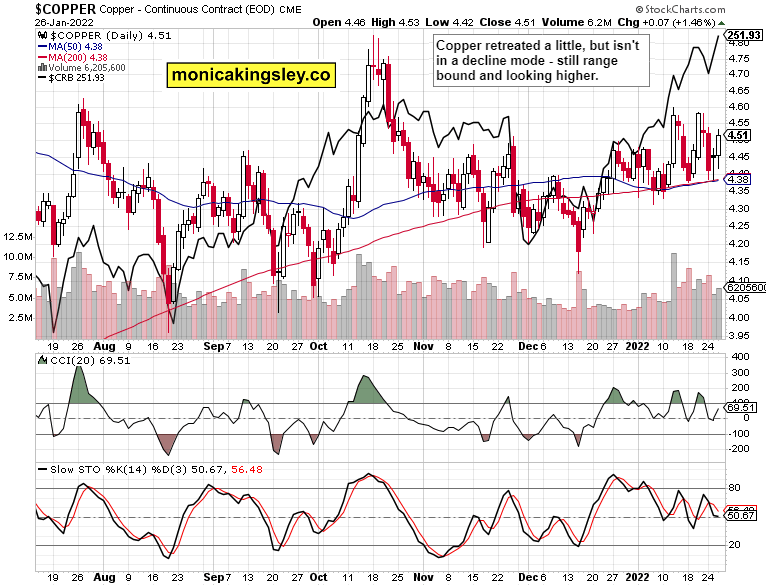

Copper

Copper is still in the catching breath phase – not yielding, and that‘s still saying something about inflation and real economy.

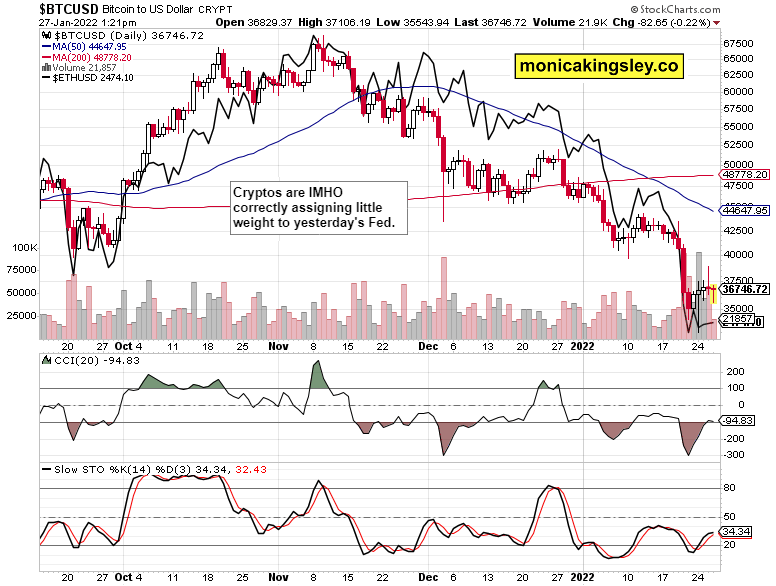

Bitcoin and Ethereum

Bitcoin and Ethereum are on guard, and ready to move somewhat higher next – for now, lacking conviction, there is no Ethereum outperformance either.

Summary

S&P 500 bulls are ready to come back, and prove that the first FOMC move, is the fake one – no, I don‘t mean the moonshot to 4,450 in the first moments. That would be the move I‘m looking for still, and it would be led by the coming tech upswing. Check the commodities resilience to the rising rates prospects – gold and silver need a reprieve in bonds badly to catch breath again, and it would come at the expense of the dollar. For now, markets are afraid of the looming liquidity crunch and Fed policy mistake as the yield curve continues compressing.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.