Oil inflation shock may hit harder than that from Covid

The Iran war inflation shock could be larger than that of the Coronavirus pandemic. You think it’s overstretched? It’s not.

At the worst moment of the pandemic aftermath, annual inflation rose to between 10% and 12% across major economies, while after the first month of the Iran war, it hovered around 3%. Indeed, it’s still well below the multi-year peaks reached in mid-2022. But we are heading there, regardless of whether the war ends today.

The Bureau of Labor Statistics reported that the cost of living in the United States surged in March, with annual inflation rising by 3.3%. Such an increase was driven by a significant 10.9% rise in energy costs, including a 21.2% jump in gasoline prices and a 30.7% surge in fuel oil.

The shocking figures are not US-exclusive: reports from Canada show that gasoline spending surged 9.1% in the same month, while in the EU, petrol prices are about 15% higher and diesel prices around 30% higher in early April compared to late February, according to CaixaBank Research. And the list goes on and on.

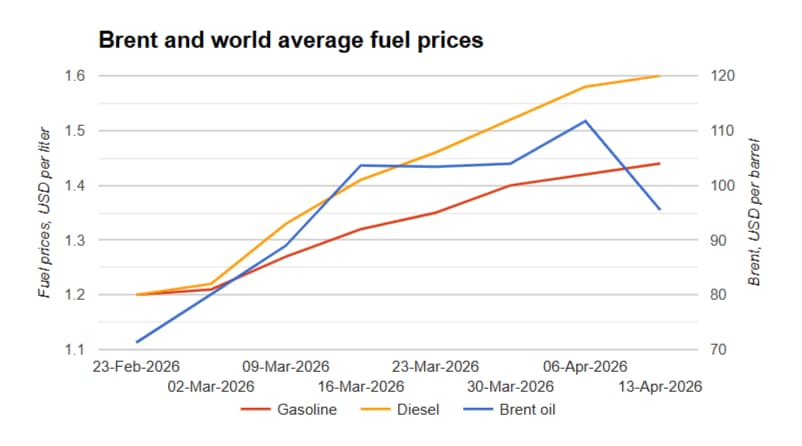

The following chart from globalpetrolprices.com shows the magnitude of price changes for world average fuel prices and prices in individual countries since mid-February.

Source: https://www.globalpetrolprices.com/fuel_price_trend_Iran_war.php

Let’s go a few years back. What triggered the post-pandemic inflation?

The main factor was supply-chain disruptions due to the global spread of lockdowns, pushing energy and food prices higher, alongside a shift in consumer spending. Households cut back on services and increased demand for goods because they couldn’t go out. Massive monetary stimulus was part of the equation, exacerbated by the Russian invasion of Ukraine in February 2022, which led to an additional and substantial increase in the price of energy and food, particularly in European countries.

It’s not easy to measure which one was the main culprit, the war or the pandemic, but no doubts both contributed to inflation spikes to multi-decade highs.

The dramatic shift in consumer preferences from services to goods took years to rebalance. Macroeconomic data has been tricky, as growth in services output over the last few years was stronger than that in manufacturing, but that’s because of the dip during pandemic times. Expansion in both sectors of the economy is finally taking place.

Back to the present

And here we are, the Middle East crisis came and in a little over a month, wiped years of economic progress, despite the fact that data may not yet fully reflect it.

For sure, a long-term peace deal could be a game-changer. The damage incurred so far could be controlled in a few months, but for that to occur, Oil prices need to return to pre-war levels no later than May. Quite an unlikely scenario if you ask me.

Should energy prices remain at current or higher levels, inflation is inevitably returning to post-pandemic levels.

Why would the scenario be worse this time?

Because there is no way to shift energy sources fast enough to avoid the Oil shock. In fact, Europe decided to become “green” in 2019, and the first stage of the process will be complete in 2030, while its full plan will be finished in 2050. The EU decision to change was based on a more sustainable future and climate action, yet it would take 30 years to complete. Furthermore, the so-called European Green Deal requires an estimated €1 trillion in clean investments over the next decade, with calls for over €477 billion in additional yearly investments to meet 2030 targets.

Besides, even if economies had the budget to change immediately, there are not enough alternative energy sources to replace fossil fuels.

And one step more: guess which country is ahead in alternative energy sources? Yes, China. Over the last few years, the administration led by Xi Jinping has been preparing for a crisis like this. The country still relies on Oil and coal but has curbed its dependence, investing in wind, solar, and hydropower, which, to date, generate roughly 30% of China’s electricity. The country also dominates global manufacturing and exports of solar modules and battery storage, yet, of course, if the crisis intensifies, most of that production will likely be used locally to counter the Oil crisis.

The spike in inflation we’re seeing is just the tip of the iceberg. A resolution to the Iran war is very unlikely in the short term, and even that wouldn’t immediately solve all the disruptions in energy markets. The longer Oil prices stay elevated, the larger the pass-through to consumers will be, as firms will ultimately choose to preserve their margins. Markets may still be pricing a temporary price spike, but we are more likely to be heading toward a far more persistent inflation regime.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.