Why a hawkish RBA is no longer enough to lift the Australian Dollar

The Reserve Bank of Australia delivered more than what markets expected: a hawkish hold that should have supported the Aussie. But markets widely ignored it, focusing instead on slowing economic growth and proving that central bank messaging alone isn’t always enough to drive currencies.

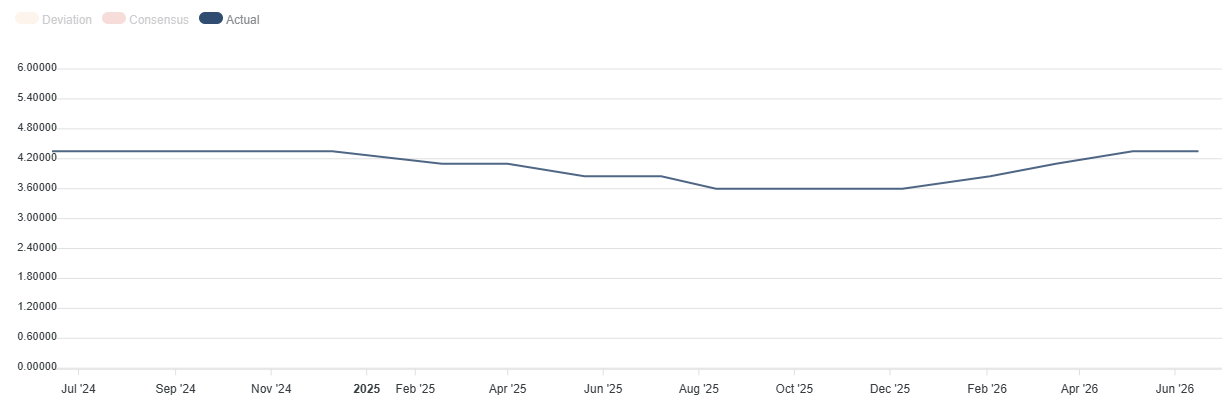

The Reserve Bank of Australia left its cash rate unchanged at 4.35% at its June meeting, in line with market expectations. The decision ends a sequence of three consecutive 25-basis-point rate hikes since the beginning of the year.

At first glance, the statement and Governor Michele Bullock’s press conference can be seen as hawkish as the central bank stresses that inflation remains too high, highlights persistent upside risks, and repeats that it is ready to raise rates further if needed.

The most important line in the statement is probably the one saying that the RBA will do “what it considers necessary” to bring inflation back to target, “including increasing the cash rate target further if required.”

During the press conference, Bullock also refused to rule out more tightening. “We might have to do more,” the governor said, while stressing that the board remains concerned about underlying inflation pressures.

Markets did not buy the RBA hawkish message

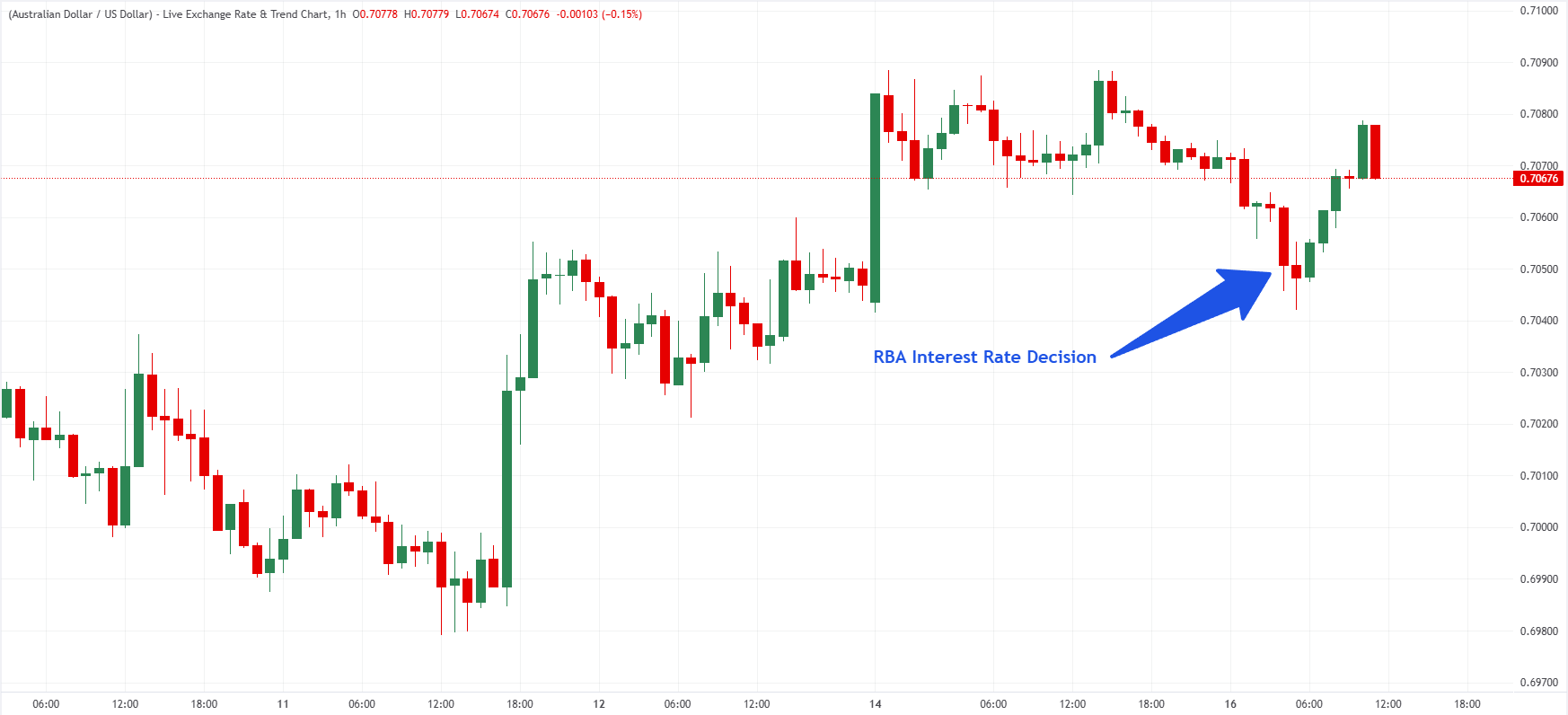

Despite this firm tone, the market reaction was telling. The Australian Dollar (AUD) fell immediately after the decision, while short-term swap rates also moved lower. This reaction suggests that investors now require a much higher bar for hawkish communication to support a currency, even though the Aussie recovered following Bullock’s press conference.

Francesco Pesole, FX strategist at ING, summed up the situation clearly: “Australia is an example of the higher bar for hawkish communication set by markets.” According to the strategist, investors are focusing more on Australia’s slowing economy than on the threat of further rate hikes.

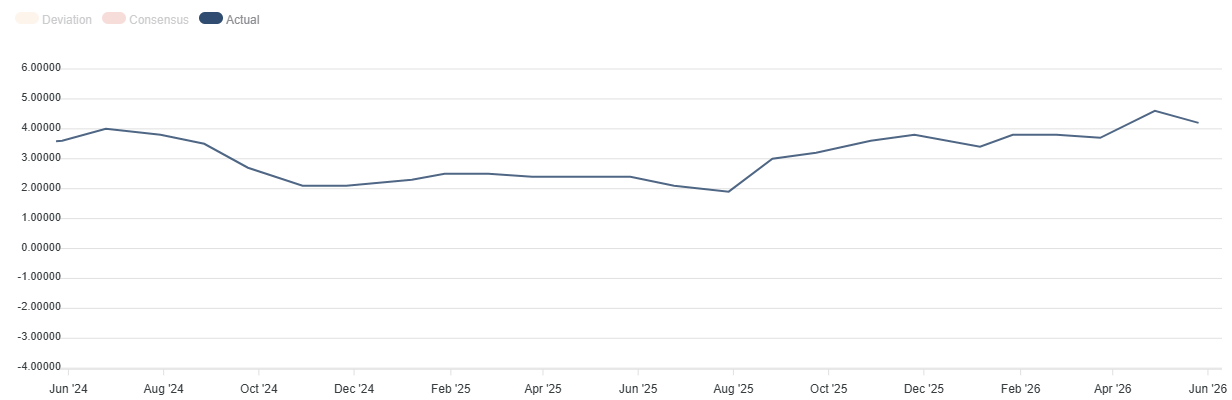

Recent economic data confirm this shift in perception. First-quarter Gross Domestic Product (GDP) rose only 0.3% QoQ, down from 0.9% in the previous quarter.

Inflation remains a problem, but growth is slowing

The RBA faces a difficult balancing act. On one side, inflation is still well above the 2%-3% target range. Headline Consumer Price Index (CPI) grew by 4.2% YoY in April, while some underlying measures remain sticky. Energy costs also remain a concern, while the RBA believes global Oil supply disruptions will continue to put upward pressure on energy prices and inflation for some time.

And inflation may rise further in the coming months. Harry Murphy Cruise, Head of Economic Research at Oxford Economics Australia, said to Reuters: “Much of the CPI hit from higher input, shipping and agricultural costs is still working its way through to consumer prices.”

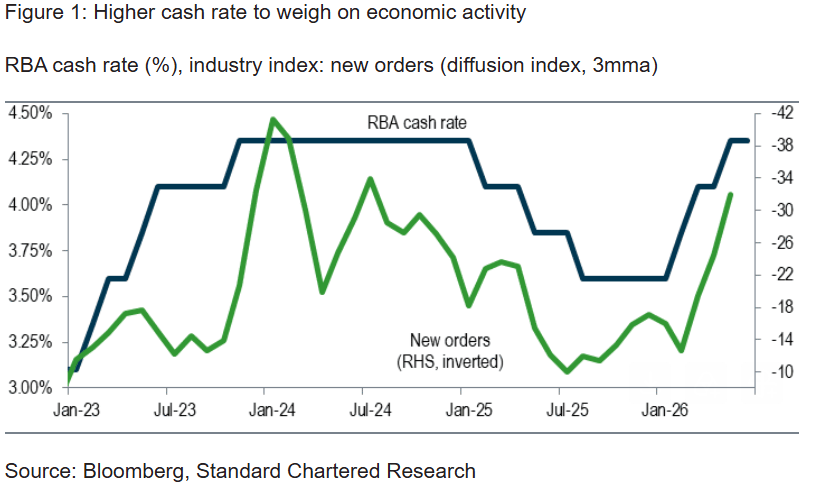

On the other side, the effects of tighter monetary policy are increasingly visible. Growth is slowing, the Unemployment Rate has risen to 4.5% in April, household spending is weakening, and confidence surveys point to softer activity ahead.

Nicholas Chia, FX and Macro Strategist at Standard Chartered Bank, said: “We expect a further slowdown in economic activity and loosening of the labour market to alleviate longstanding capacity pressures.”

RBA’s Bullock also acknowledged that demand needs to slow to bring inflation sustainably back to target.

The debate now shifts to the peak in rates

One of the most important developments after the meeting is the debate over whether Australian interest rates have already peaked. Several institutions now believe the cash rate is either at its peak or very close to it.

TD Securities has dropped its call for additional hikes this year and now expects the cash rate to remain at 4.35% for an extended period. TD Securities argues that the RBA’s explicit reference to the three hikes already delivered this year often signals a shift toward a waiting phase.

Westpac, however, remains more hawkish. Chief Economist Luci Ellis says the RBA’s message was designed to push back against speculation that the tightening cycle is over. Westpac still expects another rate hike, potentially in August if upcoming inflation data remain strong.

For its part, Standard Chartered maintains its baseline scenario for the near future, which is that the RBA’s cash rate has peaked at 4.35%.” A decline in energy prices following a sustained cessation of US-Iran hostilities would also help the RBA maintain price stability,” added the bank.

China remains a key driver for the Australian Dollar

Beyond domestic monetary policy, China remains one of the most important external drivers for the Australian Dollar. Recent Chinese data have disappointed. Retail Sales fell 0.6% YoY in May, while Fixed Asset Investment declined more than expected.

This matters because Australia remains heavily dependent on Chinese demand for commodity exports.

Even if the RBA keeps a restrictive bias, a sharper slowdown in China could continue to weigh on the Aussie in the months ahead.

What it means for the Australian Dollar

For the Australian Dollar, the message from the RBA meeting is clear: The central bank remains hawkish, but that alone is no longer enough to lift the currency.

In the short term, markets are more focused on Australia’s slowing growth, weak Chinese data, and the outlook for US monetary policy.

ING argues that the Federal Reserve (Fed) will remain the main driver of AUD/USD over the coming months. The bank still sees room for AUD/USD to recover later in the year if markets start to price in a more dovish Fed outlook.

However, if Australian data continue to weaken and inflation gradually slows, investors may become more confident that the RBA has already reached its terminal rate, limiting the upside for the AUD.

The Aussie outlook hinges on whether the RBA has reached peak rates

The RBA’s June meeting sends a message of caution rather than victory in the inflation fight. The central bank keeps a hawkish tone and refuses to close the door to another rate hike. However, markets now see slowing growth as almost as important as inflation risks.

For the Australian Dollar, this is crucial. As long as investors believe growth is slowing faster than inflation is accelerating, the threat of more rate hikes may have only a limited impact on the currency. The debate is no longer only about whether the RBA will hike again, but whether the central bank has already reached, or nearly reached, the peak of its tightening cycle.

RBA FAQs

The Reserve Bank of Australia (RBA) sets interest rates and manages monetary policy for Australia. Decisions are made by a board of governors at 11 meetings a year and ad hoc emergency meetings as required. The RBA’s primary mandate is to maintain price stability, which means an inflation rate of 2-3%, but also “..to contribute to the stability of the currency, full employment, and the economic prosperity and welfare of the Australian people.” Its main tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will strengthen the Australian Dollar (AUD) and vice versa. Other RBA tools include quantitative easing and tightening.

While inflation had always traditionally been thought of as a negative factor for currencies since it lowers the value of money in general, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Moderately higher inflation now tends to lead central banks to put up their interest rates, which in turn has the effect of attracting more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in the case of Australia is the Aussie Dollar.

Macroeconomic data gauges the health of an economy and can have an impact on the value of its currency. Investors prefer to invest their capital in economies that are safe and growing rather than precarious and shrinking. Greater capital inflows increase the aggregate demand and value of the domestic currency. Classic indicators, such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can influence AUD. A strong economy may encourage the Reserve Bank of Australia to put up interest rates, also supporting AUD.

Quantitative Easing (QE) is a tool used in extreme situations when lowering interest rates is not enough to restore the flow of credit in the economy. QE is the process by which the Reserve Bank of Australia (RBA) prints Australian Dollars (AUD) for the purpose of buying assets – usually government or corporate bonds – from financial institutions, thereby providing them with much-needed liquidity. QE usually results in a weaker AUD.

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the Reserve Bank of Australia (RBA) purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the RBA stops buying more assets, and stops reinvesting the principal maturing on the bonds it already holds. It would be positive (or bullish) for the Australian Dollar.

Author

Ghiles Guezout

FXStreet

Ghiles Guezout is a Market Analyst with a strong background in stock market investments, trading, and cryptocurrencies. He combines fundamental and technical analysis skills to identify market opportunities.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)