Oil Gushes Lower Leading Commodity Exodus

Oil prices tanked overnight as an overbought commodity market finally ran out of steam.

The long-awaited short-term correction in oil prices finally occurred overnight with Brent and WTI, both plunging some 3% as commodities prices, in general, were cratered on fears of slowing growth in China. To be fair, given the bullish run and extended long positioning across commodities in general in recent times, it was only going to one straw to break the camel’s back and see a mass rush for the fire exits by long positioning.

Oil, in fact, received a series of camel straws across its back which all came together to produce the overnight sell-off. The American Petroleum Institute’s (API) Crude Inventories came in at +6.5 million barrels against an expected drawdown of -1.6 million barrels. China data yesterday was slightly on the soft side. Finally, the International Energy Agency (IEA) Report put the boot well and truly into crude. The IEA forecast that demand would drop with prices at these levels, that American shale would continue to ramp up production and said temporary chances in production rather than structural ones were responsible for much of the recent rally.

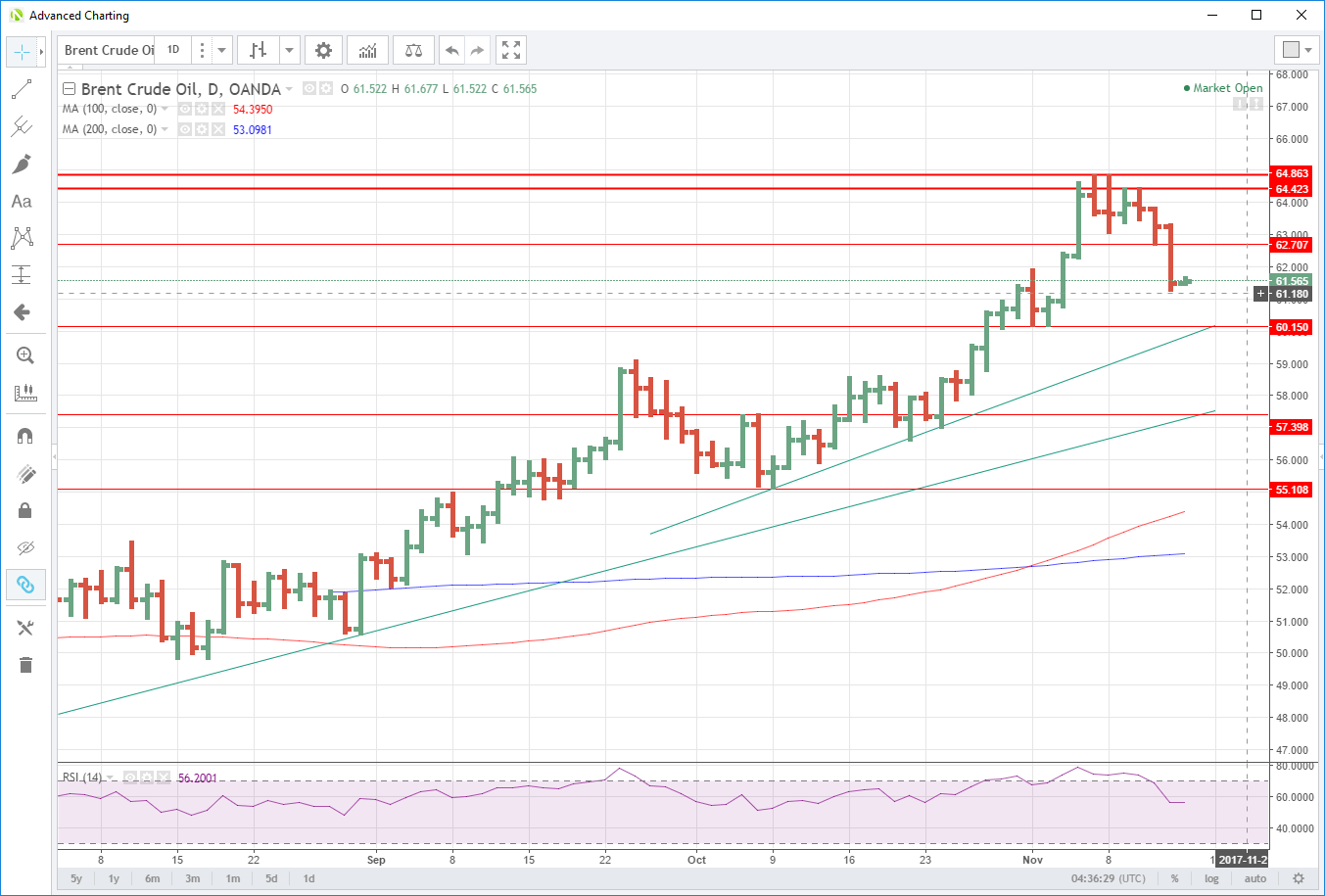

Brent crude’s double tops at 64.80 and 64.45 are now well in place as strong medium-term resistance with interim resistance at 62.70. Below its present level at 61.60, critical support for the rally currently sits at 60.00, a daily triple bottom and also trend-line support this morning. A daily close under this level opens the doors to a test of the long-term trend line at 57.30.

Brent Crude Daily

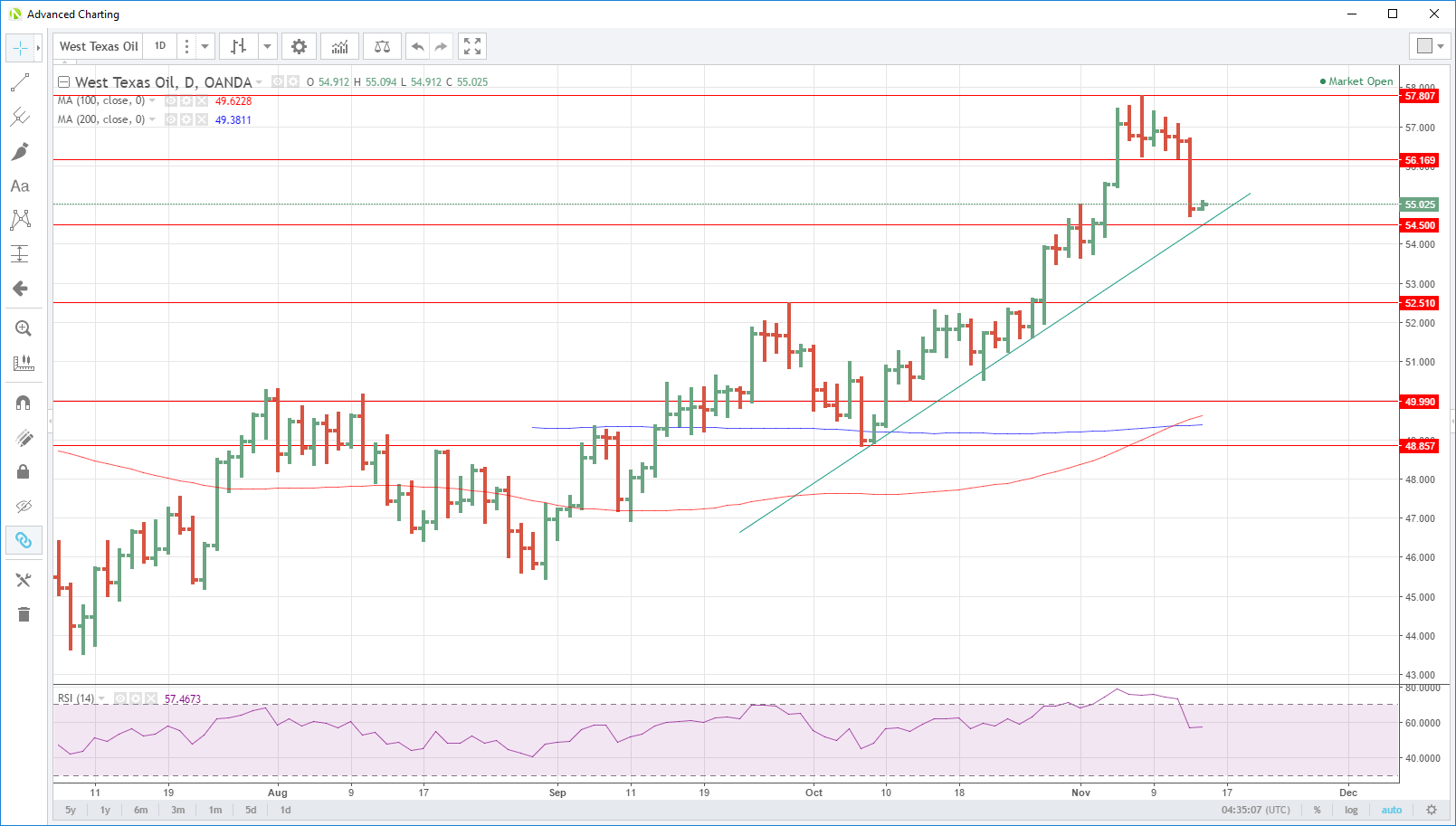

WTI sits at 55.00 barely above its overnight close. 56.15, the approximate low of the week is now formidable resistance. This is followed by last week’s high at 57.80. WTI’s downside looks less secure with trend line support nearby at 54.50 with a break opening up 53.50 and then 52.50.

WTI Daily

On a positive note, the technical indicators have unwound their extremely overbought levels and then some. Whether this is enough to support crude prices, as we negotiate tonight’s official U.S. Crude Inventories, remains to be seen.

Author

Jeffrey Halley

MarketPulse

With more than 30 years of FX experience – from spot/margin trading and NDFs through to currency options and futures – Jeffrey Halley is OANDA’s senior market analyst for Asia Pacific, responsible for providing timely and relevant