December central bank overview

Major central bank rundown

It’s time for your central bank catch up. The link to the latest statement is at the bottom of each section, so just click there to read the bank’s central statement. Remember, there is no substitute for actually reading a central bank statement yourself and it will almost certainly be of great benefit to your trading. However, here is a summary analysis of the major central banks’ positions.

Reserve Bank of Australia, governor Phillip Lowe, 2.85%, meets 06 December

RBA: Slowing down on hikes?

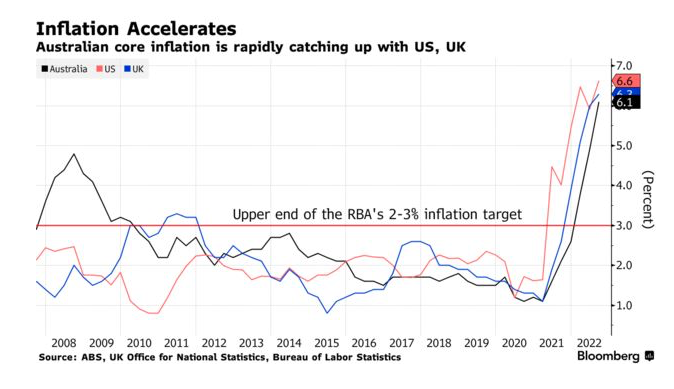

The RBA hiked rates by only 25bps early on Tuesday morning sending the AUD lower. Once again, taking the RBA meeting in balance, it was a more dovish response. Going into the November meeting markets were fully expecting a 25 bps rate hike. This was despite the latest trimmed mean reading of 6.1% CPI which was on the high side, so there was always a chance of a surprise 50bps hike. In the event the RBA hiked by only 25bps.

The RBA revise growth lower Central banks around the world are trying to balance hiking interest rates to control inflation without over-tightening. The risk, for example, that many economists see is that the Fed is on the brink of over-tightening. So, the RBA have one eye on growth and one eye on inflation. The RBA is concerned about slowing growth. They revised growth projections lower to 3% this year and 1.5% in 2023 and 2024. So, the RBA will not want to overreact to inflation by going too hard on rates for too long.

Inflation is now forecasted to peak at 8% this year before falling to 4.7% over 2023 and just over 3% in 2024. The expectations of slower rate hikes from the RBA are broadly supportive for Australian stocks. The Short Term Interest Rate market reaction the day after the decision is also affirming for a slower rate path ahead. The terminal rate is expected to be just over 4% down from 4.24% prior to the meeting. However, one worrying sign for the RBA will be accelerating inflation which shows a core y/y reading now over 6%.

The Board remains resolute in its determination to return inflation back to the 2-3% target range and repeated that it expects to still hike rates over the coming period. Governor Lowe said that the board will return to larger rate hikes if deemed necessary, so watch incoming CPI data carefully. Please keep in mind that the AUD is closely impacted by the outlook for China’s economy. So, with the AUD outlook remember that a surge higher in China’s prospects also lifts the Australian dollar.

European Central Bank, president Christine Lagarde, 1.50%, meets 15 December

Avoids 2023 recession projections for now

Slowing eurozone growth is continuing to weigh on the euro and the risk of fragmentation from highly indebted countries like Italy and Greece still remains. Inflation is stubborn, but the ECB’s decision to hike rates by 75bps was expected, but the communication from the meeting was considered dovish as hints of slowing rate hikes were read into some of the details. The first point that traders looked at was the change in the wording of the statement. The previous statement read, “the Governing Council took today’s decision, and expects to raise interest rates further”. In contrast, previously the text had read, “over the next several meeting the Governing Council expects to raise interest rates further”. The omission of the word ‘several’ led investors to believe that the ECB may be slowing the path of rates going forward.

Growth was still the focus of the statement

The decision was never going to be about the amount the ECB hiked. Whether it was a 75bps hike or a 100bps hike the focus was always going to be on the future growth outlook of the eurozone. In the Press Conference, Christine Lagarde said that the APP reduction (Quantitative Tightening) would be discussed in December’s meeting. This was seen as more dovish that this would not be started until 2023 now. Sources afterwards said that the ECB does not start to plan to set the QT date in December, pushing the start of QT even further back. In a seeming contradiction to the statement sources also said that the ECB did not mean to imply a slower rate of hiking with the ‘progress’ remark and played down the removal of the word ‘several’ from the guidance on further rate hikes. Given the decision was not unanimous, with 3 voting for only a 50bops hike, it seems probable that there was something in the decision to keep both the hawks and the doves happy. The terminal rate is fluctuating from day to day and recent market pricing now sees a terminal rate above 3% and that rise above 3% to come in the summer of next year. See the financial source implied interest rate tracker below.

The main takeaway

Nothing really tradable from this last meeting. The ECB is keeping the option open to hike rates more aggressively if it needs to, but also showing that the ECB can slow down rate hikes if it needs to. There was something for both the doves and the hawks in the last meeting though the decision was taken as dovish as a whole. Since the last meeting expectations are rising for a steeper rate hiking path and the terminal rate is now seen as above 3%. The path of the EURUSD will likely still remain USD driven. When you consider that the relentless USD strength has weakened the JPY, NZD, AUD, GBP and the EUR the best chance of a EURUSD pickup will come from a more dovish Fed.

Bank of Canada, governor Tiff Macklem, 3.25%, meets December 07

In the prior meeting, the BoC noted that the housing market was cooling, as anticipated with higher mortgage rates, and down from the ‘unsustainable levels’ during the pandemic. The BoC takes a more dovish path. Going into October’s 26th BoC meeting short-term interest rate markets were split between a 50 and 75 bps rate hike. In the end, the BoC hiked by only 50bps and flagged some concerns about slowing growth.

The BoC sees lower growth ahead

The Bank of Canada once again flagged areas sensitive to rising interest rates like the housing sector. The BoC noted that housing activity has fallen sharply and household spending is falling. Furthermore, in the released statement prior to the Q&A BoC’s Macklem stated that the tightening phase will draw to a close, ‘but not there yet’. He added that it expects growth to fall in the next few quarters. As a balance to this statement, the BoC still stated that policy interest rates will need to rise further to counter elevated inflation. The Council also repeated that the bank’s preferred measure of inflation (core) is not showing meaningful signs of price pressure easing.

The bottom line

The tone of the slower growth comments means the BoC is starting to start thinking about slowing the path of rates. This is a more dovish stance from the BoC and should allow the CAD to weaken somewhat over the medium term. After the rate statement, Governor Macklem highlighted that he expected a ‘significant slowing of the economy to occur’.

In terms of the USDCAD, it may be trickier to pick a direction. If the Federal Reserve starts to hint that it will be slowing down then the USD could find itself experiencing a period of weakness too. A GBPCAD long may be an option as the battered GBP recovers on the reassurance of a new fiscally prudent PM. The next meeting is on December 07, 2022.

Federal Reserve, Chair: Jerome Powell, 3.875%. meets 14 December

Federal Reserve holds the line on the inflation fight

The Fed hiked by 75 bps as expected and initially had bullish stock hopes firing. The Fed said, in its statement, that it would consider the impact of monetary tightening lags as it moved forward. This was a dovish statement as it suggested that the Fed was not going to just automatically keep taking large rate hikes. It was the Fed trying to reassure the economists who thought the Fed risked over-tightening. See below for the Bloomberg survey which showed that nearly 75% of all economists surveyed thought the Fed risked over-tightening. However, all bullish hopes for stocks quickly faded once the Press Conference started.

-638034317444529650.png)

Higher terminal rate signpost sinks stocks out of the meeting

The key statement was when Powell said that he thought it was appropriate for rates to be higher than previously thought. This was a hawkish statement and the terminal rate, according to Short Term Interest rate Markets, has now gone up to over 5% from under 5% a week ago. Jerome Powell also made it clear that there was a need for ongoing rate hikes with ground left to cover.

The takeaway

Was the Fed hawkish? Yes. Are they expecting higher rates ahead? Yes. Does this mean that the Fed will 100% move rates higher? No. The Federal Reserve will look at three key things. Inflation, the US labour market, and the impact of the rate hikes it has done so far. So, this is a good time for volatility. If inflation looks like peaking, expect stocks to rally in anticipation of a Fed pause. If the US labour market shows signs of stress, then again expect stocks to rally on the hopes of a Fed pause. So, seeing the medium-term path clearly has just got harder. However, the potential for short-term volatility on certain key Fed-focused economy data points has just increased. There is now a 50/50 chance of a 75 bps hike in December. The other option is a 50bps hike.

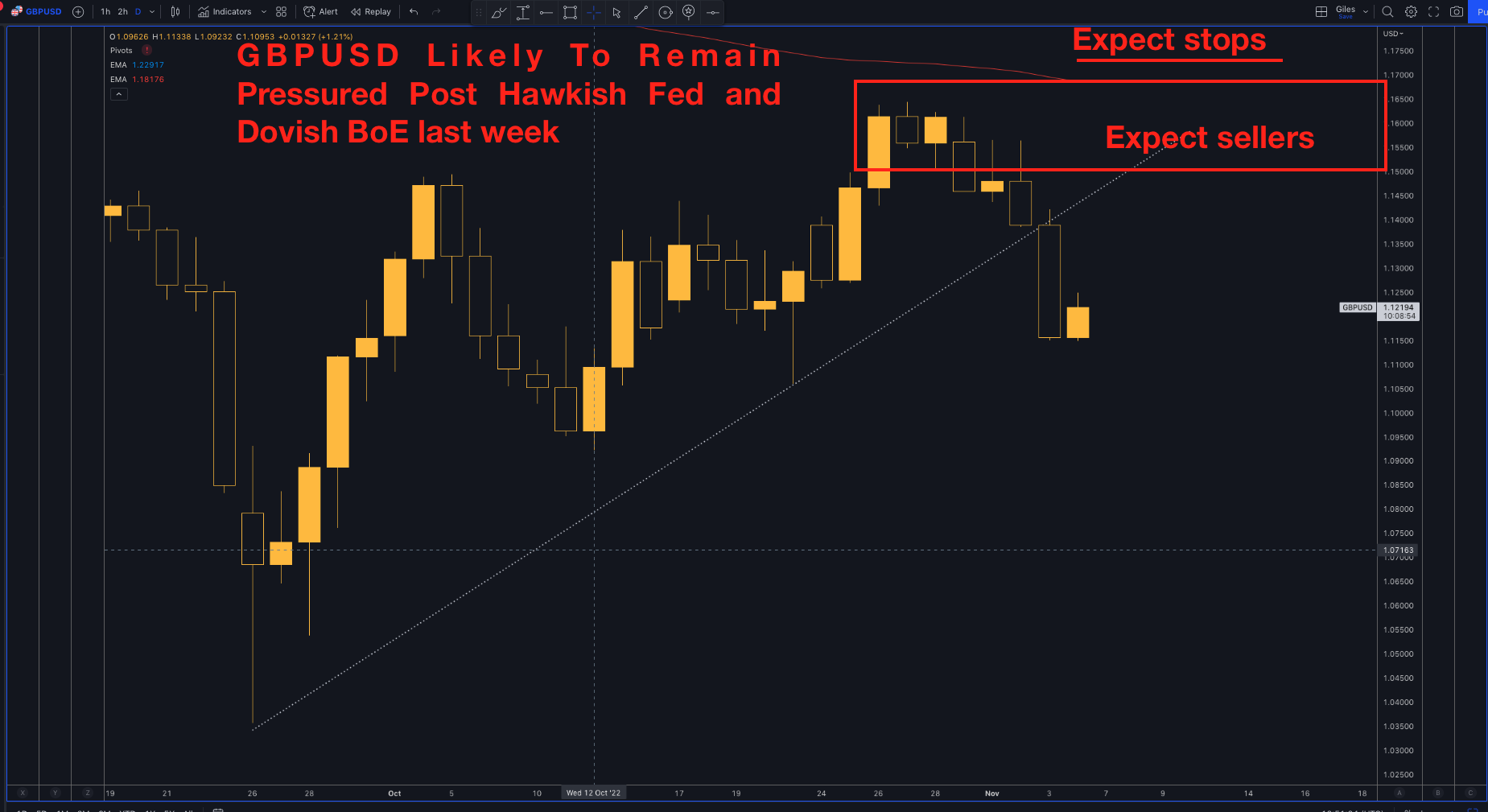

Bank of England, governor Andrew Bailey, 3.00%, meets 15 Dec 2022

BoE senses it can do less as it expects inflation to cool

What a difference a new Prime Minister has made to the Bank of England! The Bank of England hiked rates by 75 bps to 3% last week in the biggest hike in over 30 years. However, the Bank of England signposted that it would be able to bring rates to a lower level than it had previously anticipated. This was reflected in Short Term Interest Rate markets on Friday of last week with the high rate now seen as 4.68% (down from 4.89%). That’s the good news for UK mortgage owners, but the bad news is this. The Bank of England is only able to tighten less because the fiscal pain is going to come from the UK’s budget on November 17. After the meeting, Bank Of England’s Mann reminded markets that rates do not need to be as high as the market suggests. This could mean a high of 4.5% or perhaps 4.25% next year. Bank of England’s Baily said that rates lie closer to the constant rate curve than the market rate curve.

Lower inflationary pressure ahead due to the Energy Price Guarantee

The Bank of England’s projection for inflation were mainly lower due to the success of the Energy Price Guarantee. Inflation is now seen at 5.20% for Aug 2023. This is down from August’s forecast of 9.53%. In two years time inflation is seen at 1.43% and this is down from August’s forecast of 2%. So, reassuring sounds from the BoE around inflation and hence in part why the BoE needs to do less.The path for GDP has been revised lower longer out. So although the near-term GDP for 2022 is now seen as 4.25% (vs 3.% prior) the longer-term 2024 GDP outlook is seen as -1% (vs -0.25% prior).

The bottom line

The BoE sees the need to do less, but that could be because a painful UK budget is on the way. So, this means that all eyes will be firmly on the November 17 budget and in the meantime the GBPUSD will likely be pressured lower as long as the Fed is seen as needing to maintain its hawkish stance.

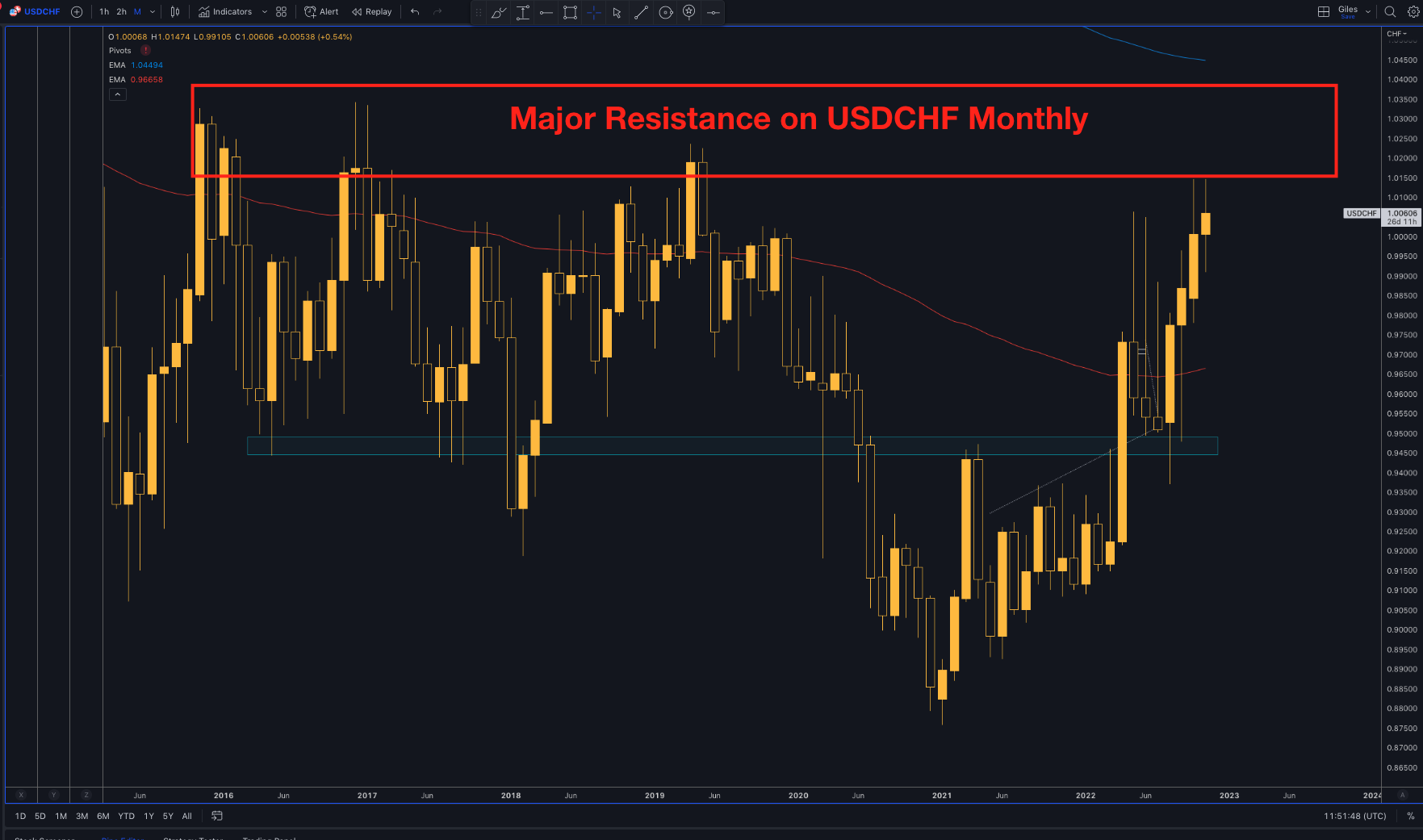

Swiss National Bank, Chair: Thomas Jordan, 0.50%, meets December 15

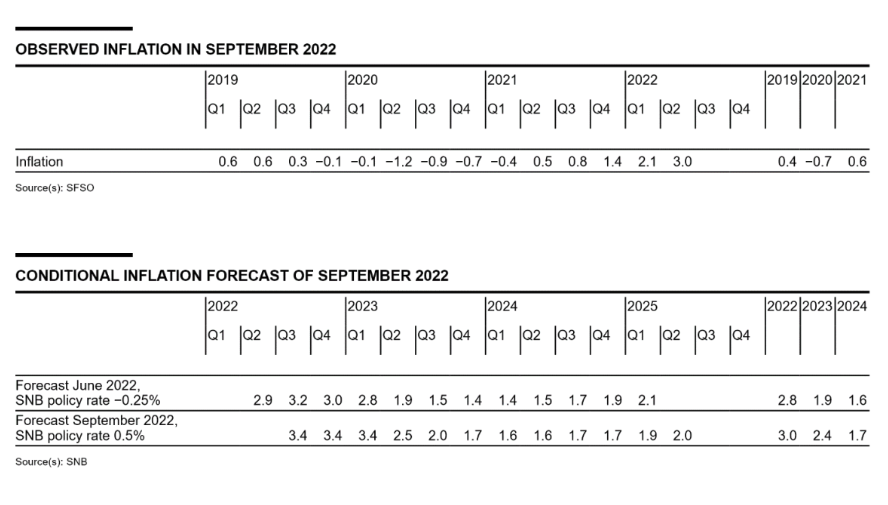

The latest SNB decision was a continuation of its June meeting and it raised interest rates from -25% to 0.50%. The largest rate hike in recent history and a measure of the concern that the SNB has over rising inflation. However, the initial reaction was dovish as markets had been pricing in a 100bps rate hike and a 75 bps hike was a surprise. Aside from day-to-day moves the big picture remains the same that the SNB is likely to get tough on inflation with further rate hikes. SNB’s Jordan stated on October 07 that domestic inflation above 3% is clearly too high and the central bank will not tolerate above-target inflation. The SNB acted again to combat spreading inflation in a bid to keep inflation out of Swiss goods and services. The SNB now sees inflation higher than it did in the June meeting. Q1 2023 inflation is now seen at 4.3% vs 2.8% from September. However, inflation is still expected to fall back down in 2023 Q4 to under 2%.

The problem remains for the SNB, like the RBA, the BoE and the Fed, that it does not want to see a ‘wage-price’ spiral. All of this means the SNB is tackling inflation on the front foot and it doesn’t want inflation to go into wages. With inflation at 3.0% on November 03, the SNB still has more work to do to get rates down sub 2%. Remember, If the US starts to show falling inflation or a slower path of rates ahead then USDCHF can move sharply lower. You can read the full SNB statement here.

Bank of Japan, governor Haruhiko Kuroda, -0.10%, meets 20 December

The main issue that remains for the BoJ is the JPY weakness. JPY weakness has been extreme recently as the US10Y yields kept pushing higher on US inflation fears. However, the key aspect of this is whether there will be action from the BoJ. Going into the BoJ meeting there had been expectations that the BoJ may signal hiking interest rates as a way to deal with the pervasive weakness in the JPY. In the event, the BoJ kept rates at -0.10% and also maintained its yield curve control at 0%. The focus then quickly changed as to whether BoJ’s Governor Kuroda would give any hints on FX intervention in the press conference. The BoJ hold its dovish line for another meeting

BoJ’s Kuroda said that he had ‘no comments’ on FX intervention. However, he did say that the Government had taken appropriate action against excessive FX volatility and the yen weakening had been one sided. It was also interesting to see Kuroda pushing back against the interest rate differentials between Japan and the US. Kuroda said that it is not correct to explain the USD strength only based on interest rate differentials. He said that the US-Japan interest rate differentials had little correlation with the USDJPY rate when looking at past levels, This seems a strange statement given how the interest rate differentials have been driving the USDJPY higher all year and have been in virtual lockstep for years.

-638034319292535033.png)

The main point

The takeaway here is that the BoJ is really continuing to hold out for the Fed to start slowing the path of hiking rates. This is the most likely source of more straightforward JPY strength that does not have to be artificially generated by the BoJ. Also, it means that speculation the BoJ is going to exit its ultra-loose monetary policy can end for now. It also means that a dovish Fed pivot later today, if it should happen, would make a USDJPY short attractive for some traders. However, in the meantime, further potential BoJ action in the USDJPY pair can not be ruled out. The next meeting is on December 20.

Reserve Bank of New Zealand, governor Adrian Orr, 3.50%, meets 23 November

RBNZ: Another hawkish hike

The last RBNZ meeting was in line with its recent hawkish bias. Rates were raised by 50bps to 3.50bps and the RBNZ maintained a robust view of the domestic economy. Reuters reported that the board even debated hiking by 75bps and was expressing concerns over a weaker NZD which posed threats to the inflationary outlook. The RBNZ noted that domestic spending has been strong despite slowing growth. Employment levels are high and households have managed to keep higher levels of savings. The household debt levels are still historically low and this gives the RBNZ confidence in hiking rates.

The country, like many other places, is also still seeing labour shortages. Unemployment is low and the committee wants to see monetary conditions tighten so that it achieves its inflation target. Inflation is still high in New Zealand with CPI y/y at 7.3%.

The RBNZ has affirmed that it will not pull back from hiking rates and this hawkish stance should keep the NZD supported. However, it is worth noting that the NZD has been tricky to trade recently. Despite some pretty strong fundamentals the currency does not always strengthen in the way you might expect.

Therefore, a more prudent approach might be to step aside and avoid trading the NZD until it becomes more predictable. Although it should also be said that an AUDNZD sell bias made sense on the divergence between the RBA and the RBNZ after the last RBNZ meeting, but that boat has passed now.

Author

Giles Coghlan LLB, Lth, MA

Financial Source

Giles is the chief market analyst for Financial Source. His goal is to help you find simple, high-conviction fundamental trade opportunities. He has regular media presentations being featured in National and International Press.