Not batting an eyelid

S&P 500 didn‘t correct much intraday, and the risk-on turn has continued unabated with value pulling ahead sharply – unlike the day before when the revesal came about because of tech. The dust is settling in the market‘s mind, VIX has indeed moved and the dollar weakened noticeably. That was the subject of Friday‘s analysis – the disappearing safe haven premium over many assets such as gold, crude oil and Treasuries (Treasuries though kept their cool the most, not losing the focus on Fed‘s tightening).

Risk-on appetite returned to stocks with a vengeance, and market breadth has significantly improved – within the context of the ongoing correction, must be said. While we made local lows on Thursday after all, the upside momentum is likely to slow down next – this week would bring a consolidation within a very headline sensitive environment. It‘s looking good for the bulls at the moment – till the dynamic of events beyond markets changes.

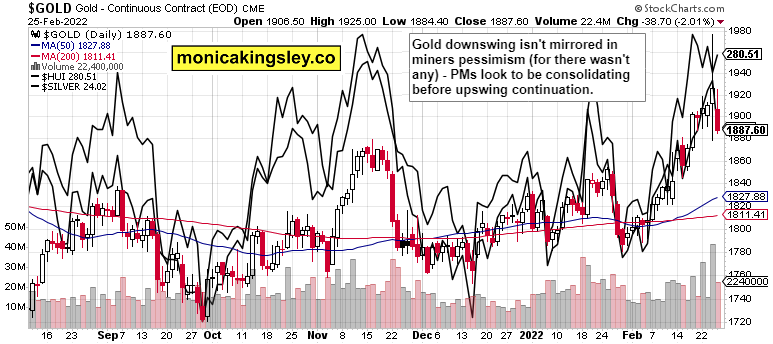

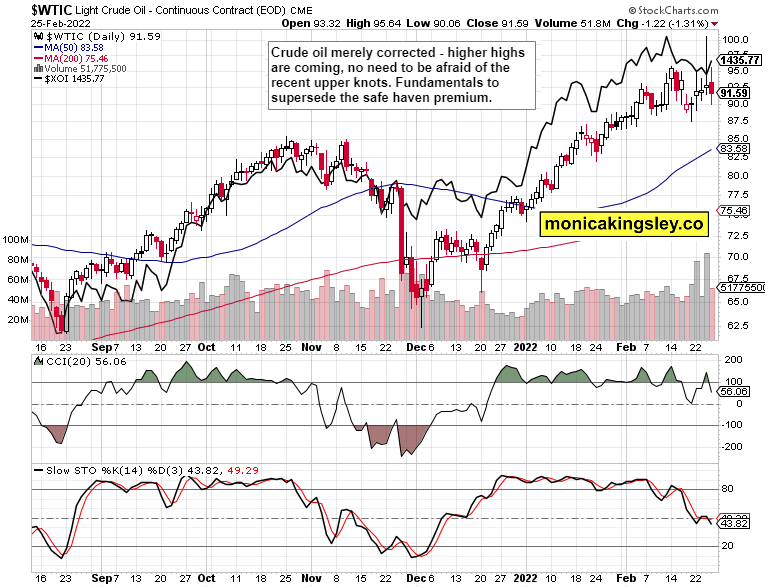

Inflation isn‘t wavering, and I‘m not looking for its meaningful deceleration given the events since Thursday, no. Friday is likely to mark a buying opportunity beyond oil and copper – these longs have very good prospects. Another part of the S&P 500 upswing explanation were the still fine fresh orders data – while the real economy has noticeably decelerated (and Q1 GDP growth would be underwhelming), solid figures would return in the latter quarters of 2022. That‘s also behind the gold downswing on Friday, which hadn‘t been confirmed by the miners – the very bright future ahead for precious metals is undisputable. And the same goes for crude oil as oil stocks foretell – the fresh long crude trade together with long S&P 500 one, are both solidly in the black already..

Let‘s move right into the charts.

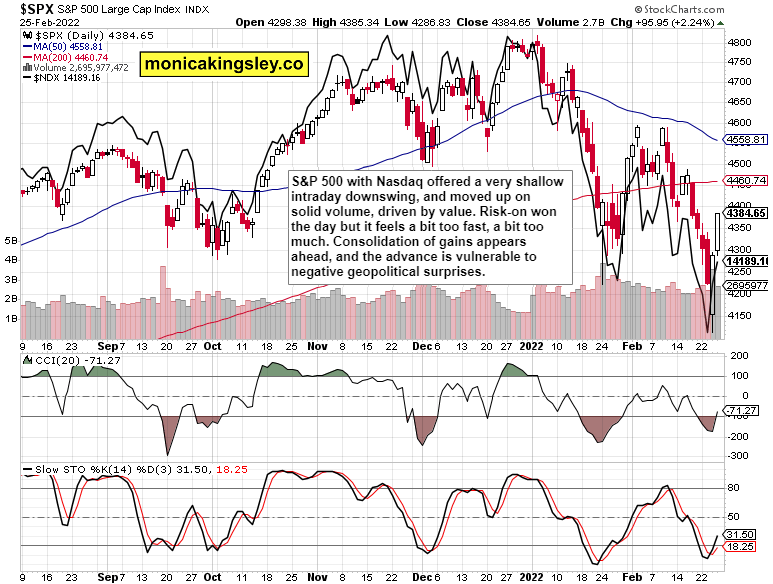

S&P 500 and Nasdaq outlook

Sharp S&P 500 upswing on solid volume – the gains can continue but their pace would slow down. Negative sentiment is departing stocks as the existing bad news has been priced in. The pendulum is swinging the other way now.

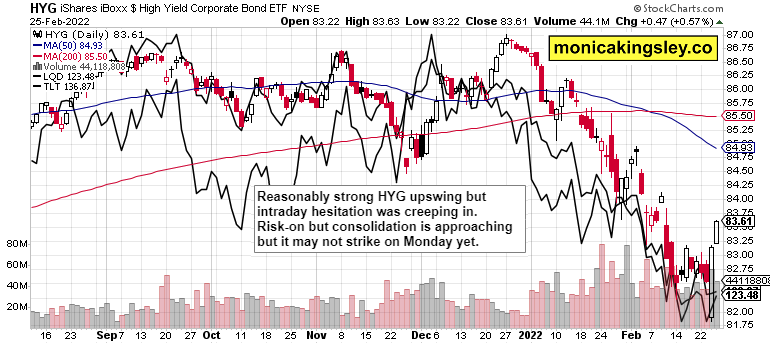

Credit markets

HYG is confirming the stock market upswing, but bonds are remaining more cautious overall – it‘s that the focus would shift over the coming 2 weeks again to the Fed. The yield spread keeps compressing and the 2-year bond didn‘t stop pressuring the Fed.

Gold, silver and miners

Precious metals have corrected a little but the upswing goes on – GDX performance is a good omen. The decline in prices wasn‘t sold heavily into anyway – we‘re still moving higher next as the rate raising cycle start is soon here.

Crude oil

Crude oil bears are totally unconvincing, proving that the prior price upswing was about way more than geopolitical uncertainty – the chart remains strongly bullish, and we have higher to run still.

Copper

Copper upswing is indeed taking time to develop, but commodities strength remains in spite of the daily setback, which just illustrates the risk-on euphoria in stocks. The commodities upleg hasn‘t run its course, and the red metal would join in.

Bitcoin and Ethereum

Cryptos are refusing to extend Sunday‘s decline – while the worst appears to be over, the short-term direction can turn out in both directions. I‘m though slightlly favoring the bulls.

Summary

S&P 500 turnaround continues, and price gains are frontrunning the events on the ground. The upswing is vulnerable – to a consolidation at most as a full reversal would require fresh setbacks, including in Asia. Risk-on trades have the momentum, and credit markets agree. It certainly looks like a good time to take advantage of the precious metals and commodities discounts as momentary optimism in the markets that has nothing to do with the progress on inflation. Further, we‘re still in the real economy slowdown phase, and the Fed hasn‘t even started hiking yet.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.