Nonfarm Payrolls Preview: Five reasons to expect a win-win release for the dollar

- Economists expect job growth to cool down to 300,000 in August, after 528,000 in July.

- ADP's relatively downbeat data further lowers estimates.

- White House comments about a slower labor market also push estimates down.

- Hawkish Fed rhetoric means it would take a disastrous hit to change the bank's path.

- Fears around China's quick economic deterioration indicate the dollar could benefit from safe-haven flows.

September is a month to remember in markets – stocks tend to fall before autumn leaves do, and this year will likely be similar. Pressure on equities is only one reason to expect the Nonfarm Payrolls report to send the dollar up. There are more in store.

Here are five reasons I expect the greenback to respond positively to the data.

1) Expectations were too low in the past four months

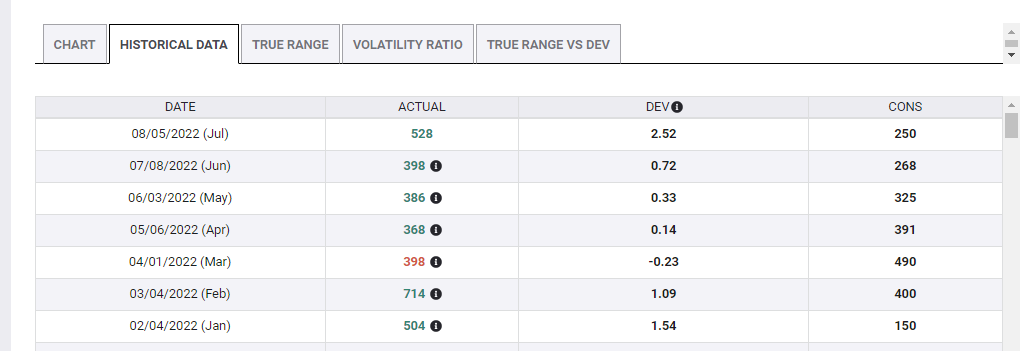

With rising wages and ongoing reports of labor shortages, economists expected job growth to slow down. The pre-pandemic average hovered around 200,000, and many expected a substantial slowdown. After every surprisingly strong NFP, economists expected a "payback" – but it never came.

Source: FXStreet

Despite the NFP's notorious volatility, it is hard to see a hiring drop from 528,000 to 300,000 – what the economic calendar shows.

2) ADP is back with a vengeance

Automated Data Processing (ADP) is America's largest payrolls provider, and its report for August showed an increase of only 132,000 private sector jobs. The firm took a two-month break from publishing its labor figures to revise its formula, after failing to predict the official Nonfarm Payrolls report, especially since the pandemic broke out.

The new statistical model and the low figures have arguably lowered expectations, making the 300,000 seen on the calendar as a "best case scenario." Bloomberg's "whisper number" is likely lower than what economists told surveyors late last week. The weak data also goes hand in hand with the next reason to expect a low bar.

3) White House damage control

Karine Jean-Pierre, the White House's spokeswoman, said on Monday that officials expect the job market to cool down. President Joe Biden receives an early notice about labor market figures and in the past, he seemed to provide reasons for high inflation ahead of the publication.

Are Biden and his team preparing the public for bad numbers? The question I would ask is: are markets taking White House comments seriously? My answer is yes. It adds to lower expectations, which in turn, makes surpassing them easier.

These first three reasons all paint a positive picture for the dollar – a stronger Nonfarm Payrolls implies an advance for the dollar, as the Federal Reserve would have to further raise interest rates. It would also need to keep them higher for longer.

4) Fed willing to accept pain

If you think that economists got it right this time, that ADP's numbers remain unrelated to the NFP, and WH warnings have failed to lower expectations – it does not mean the Fed will ease its policy.

Officials from the central bank have come out in tandem to signal that they are not only expecting to see their policy inflict damage, but are also fully willing to accept pain. It would take a truly catastrophic report to trigger a rethink at the central bank.

Before the upcoming Fed decision on September 21, officials at the central bank still have an opportunity to respond to the jobs report and clarify it does not change their minds, clearing any doubts. Markets know that.

5) Safe-haven flows

Even if the jobs report is a complete disaster – a substantial loss of jobs, not only a meager increase – it would probably be dollar-positive. Why? As mentioned at the outset, September tends to be a negative month for stocks, and this year, there are good reasons to be fearful.

China's zero-covid policy remains in full force well over two years after the pandemic broke out – and it piles onto a downturn in the housing sector. Russia's war in Ukraine has no end in sight, and high energy costs are crippling the economy. The US is doing better, but uncertainty about inflation and the Fed's policy are weighing on sentiment.

This gloomy mood boosts the dollar, the ultimate safe-haven currency – and more may be in store if the US economy shows signs of vulnerability. If the US sneezes, the world catches a cold – and the global economy seems vulnerable now.

Final thoughts

There are good reasons to expect Nonfarm Payrolls will beat estimates, which are lower than what the calendar shows. Even if my assessment is mistaken, the greenback would still benefit from safe-haven flows. It is hard to see the greenback giving any ground.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.