Negative real interest rates and post-pandemic era can significantly boost blockchain and decentralized finance

People deposit their money in bank accounts, mainly for three reasons:

-

The first reason is that through their bank account they make all kinds of transactions, therefore by using this medium they satisfy their claims and their liabilities.

-

The second reason is that they know that the banking institution, for their cash account will reward them with an economic benefit called an interest rate.

-

And the third and probably most important reason is that they have the certainty that their deposits are safe against any unexpected risk that could create a loss on their deposited cash.

These three reasons seem to apply over time. Or maybe not?

The reality is probably different from what was described above and this is because the reasons mentioned above do not seem to be fully confirmed. This non-confirmation is especially true in times of uncertainty such as the one we seem to be experiencing since the beginning of the 2008 financial crisis.

Under normal circumstances, the depositor when depositing his money in a bank account knows that the bank will lend it to someone else by collecting interest rate from the borrower. Suppose the bank actually lends this money to borrowers at an average interest rate of 4% per annum. As part of this interest rate, the bank will return it to the depositor, as a reward for the deposit made to the bank. So, let's assume that the bank gives the depositor a fee of 1.5% per annum. Therefore, the depositor has a profit of 1.5% per year. But this is a nominal profit. To measure the real profit of the depositor we will need to subtract inflation. If inflation is higher than the bank account rate, then the depositor actually loses part of his deposits, even if these deposits appear to be secured by the banking institution.

Let's see if this happens in the real world.

The truth is that unfortunately for depositors, it happens. In developed countries from 2008 to date depositors lose part of their deposits every year because, for most of the last 12 years, inflation has exceeded the deposit rate.

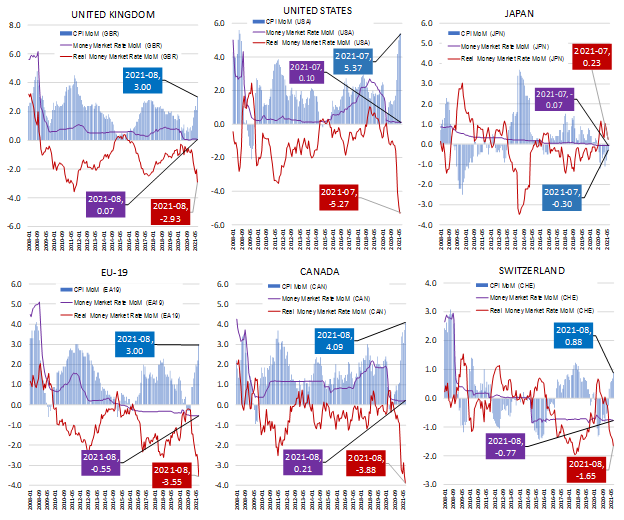

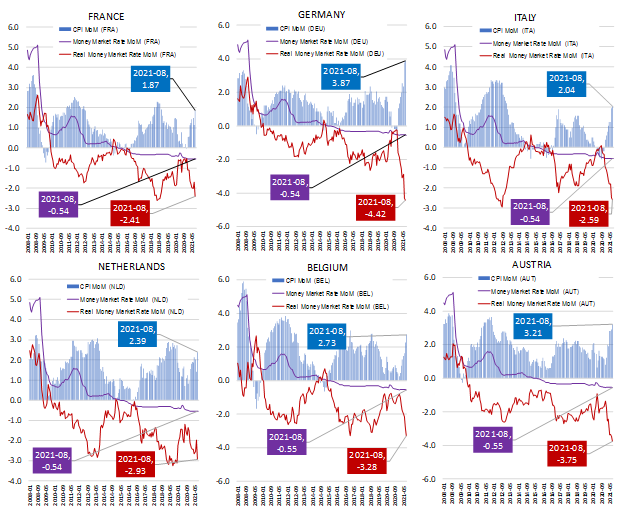

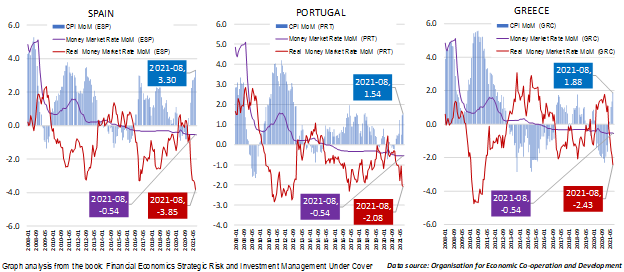

The charts below are indicative, with losses becoming even more intense in recent times where inflation has skyrocketed as the world returns to a new post-pandemic normalcy.

In the charts below, we use the money market rate as an indicator of the deposit rate, and we find that the depositors of developed economies have been recording continuous losses in the wealth of their bank deposits since 2008. This happens for two reasons:

-

Deposit rates are close to zero or even below zero.

-

Deposit rates are usually significantly lower than inflation.

-

So, depositors' real interest rates are, for most of the last 12 years, substantially negative.

In a snapshot of the moment for the month of August 2021 we see that the real interest rate for depositors in the United Kingdom was -2.93% in Germany was -4.42%, in France -2.41%, in Austria -3.75%, in Belgium -3.28% in the Netherlands -2.93%, in Spain -3.85% in Italy -2.59% in Portugal -2.08%, in Switzerland at -1.65% in Canada at -3.88% and in the Eurozone at -3.55%. Even in Greece, which due to the debt crisis experienced a period of high-interest rates, the real interest rates are now negative after they fell to -2.43% in August. Respectively for the month of July 2021, the real deposit rate in the US was -5.27% and in Japan 0.23%.

But what we see in these charts so what we can see all these years is just the tip of the iceberg. The reality is that banks after the financial crisis of 2008 are obliged to give depositors negative interest rates. They are essentially required by the central bank for commercial banks to use depositors' money to buy bonds and government bonds with zero or negative interest rates. Thus, depositors through banks participate in the repayment or in other words in the indirect restructuring of the large public debt of developed countries.

All this shows that the interest rate incentive for a bank deposit account is not valid, at least for the last twelve years, since the reality is that a depositor from 2008 until today, in most developed countries is constantly losing part of his deposits.

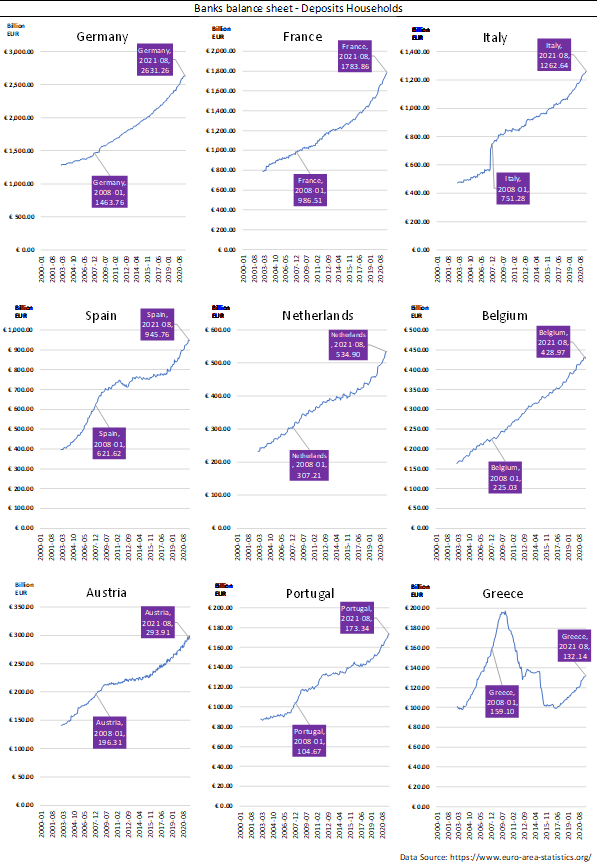

In such an environment of negative real interest rates, one would expect deposits to fall steadily. The interesting point, however, is that the exact opposite happens. Indeed, for example in most of the eurozone countries, as shown in the graphs below, according to the "euro-era statistics org", the increase in household deposits since the beginning of the financial crisis has been significant. In fact, in Belgium, deposits since 2008 increased by 90.6%, in France by 80.8%, in Germany by 79.8%, in the Netherlands by 74.1%, and in Austria by 49.7%. Even in Italy, Spain and Portugal, despite being at the center of the debt European crisis, deposits increased by 68.1% in Italy, by 52.1% in Spain, and by 65.6% in Portugal, while the only country that decreased was Greece where deposits fell -16.9%, however, have been strengthening in recent years.

The question is: Why do depositors, while seeing the decrease of their real deposits, insist and increase the amount of deposits household? The reasons are many. However, two are the main reasons for this.

-

Inflation is something that is difficult for depositors to perceive so they refuse to realize that every year they are losing part of their deposits. This behavior of refusing reality is related to the second reason.

-

The second reason is that people, especially in times of crisis, avoid risk exposure, and they target what they think is secure, thus strengthening their bank deposits as they trust the banking institutions as the “safe haven”.

However, nothing is a given especially in the current era.

After all, according to Heraclitus, “Everything flows” “Panta rhei,” which means that depositors' behavior can change.

The change can happen because the post-pandemic era already creates euphoria and reduce uncertainty by pushing inflation to a positive trend, while the high public debt will continue to force the money market and deposit rates to remain low for a long time. If uncertainty does decrease and real interest rates remain negative, a scenario that is likely to be confirmed in the distant future, then household depositors, although they will retain most of their cash in deposit bank accounts, are likely to look for alternative deposit forms.

In fact, already, one of the main reasons why depositors maintain a deposit account, namely its use for transactions that satisfy their claims and their liabilities, has found alternative avenues. Cryptocurrencies, blockchain, peer-to-peer decentralized financing, financial commodity, and foreign exchange trading platforms are some of the most shocking examples of a future that has already entered the money and trading market and it seems that it is preparing to change the entire banking and financial landscape.

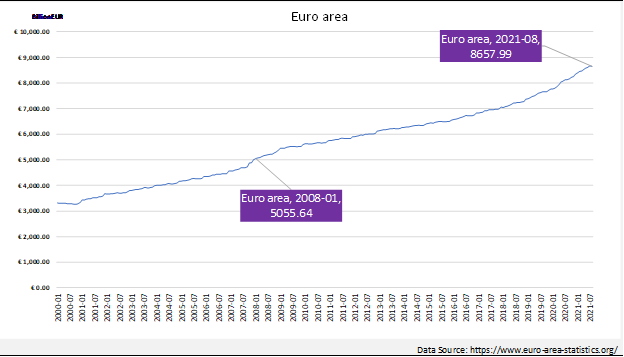

The time seems ideal. Think, today in the euro area as shown in the chart below, household deposits reached the level of 8.65 trillion euros. If some of these huge household deposit amounts are absorbed by the emerging new financial and banking environment, then decentralized and blockchain forms of banking and finance can lead to rapid changes capable of ushering in a new era in deposits and cash transactions.

The challenge of a new banking is already here, and it seems great. So, inevitably we have to manage it both on a business level and at a compliance level because it is very likely that what we considered to be a traditional bank deposit in the near future will change significantly.

While in the coming years the traditional bank account does not seem to be able to offer real interest returns to depositors, in the current era of huge technological expansion, and based on blockchain and decentralization, it seems to be a matter of time for traditional deposits to be replaced by a new form of deposit account, and so the traditional banking to be replaced by a new type of banking that will offer financial products and services able to produce positive real interest rate returns.

Author

Nikolaos Akkizidis

Independent Analyst

Nikolaos Akkizidis is an Independent Financial Writer, Economist, Author, and Speaker with more than two decades of experience in financial services, capital markets, investment advisory, portfolio management, trading, risk manage