Narrowing in Current Account Deficit in Q3 To Be Reversed

The current account deficit narrowed in Q3 due, at least in part, to a one-off surge in soybean exports. The deficit should widen again, but the country is having little trouble financing the red ink at present.

Soybean Exports Contribute to Smaller Deficit

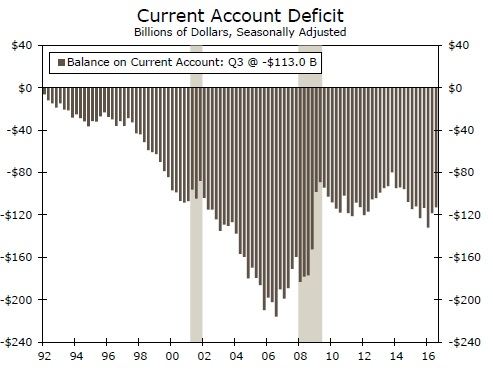

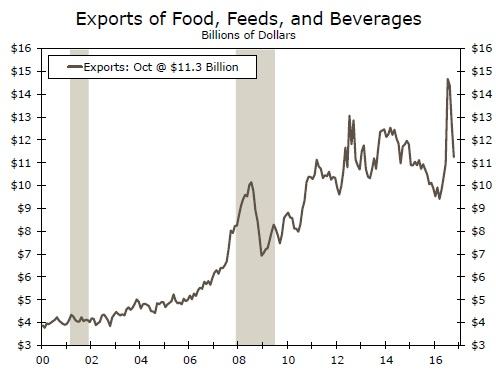

The U.S. current account deficit narrowed to $113.0 billion in the third quarter relative to the $118.3 billion (revised) deficit that was registered in Q2-2016 (top chart). The narrowing in the current account deficit came as little surprise because previously released monthly data showed that the trade deficit, which comprises the bulk of the current account, had narrowed considerably in Q3. As we explained in reports on the trade deficit in recent months, a one-off surge in soybean exports, which was related to a poor harvest in soybean-producing countries in South America, accounted for much of the decline in the trade deficit in the third quarter (middle chart).

The overall current account deficit would have narrowed a bit more had not the surplus in the income balance edged down a bit. Specifically, Americans paid out $1.5 billion more in dividends and interest payments to foreigners in Q3. In addition, the amount of transfer payments, which includes remittances that foreign workers send to their home countries (among other items), rose by $2 billion in the third quarter.

As noted above, a one-off surge in soybean exports accounted for much of the narrowing in the current account deficit in the third quarter. With that surge largely in the rear-view mirror, it seems likely that the current account deficit will widen anew in coming quarters. Indeed, the red ink in the monthly trade balance rose by more than $6 billion in October as soybean exports weakened from their previous jump. Moreover, dollar appreciation and slow economic growth in many of America's major trading partners likely will cause import growth to outpace export growth in coming quarters.

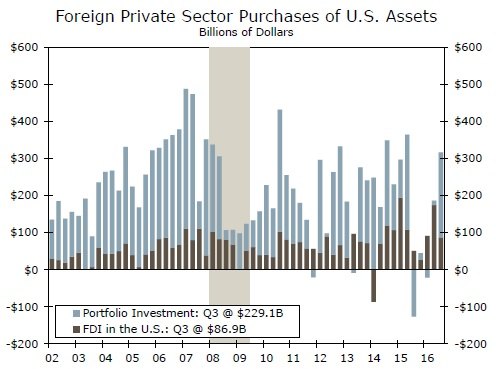

The U.S. dollar was generally stable in the third quarter, which implies that the country had little trouble financing its current account deficit via net capital inflows in Q3. Although the value of foreign direct investment inflows dropped from $174 billion in Q2 to a still impressive total of $87 billion in Q3, foreign purchases of U.S. stocks and bonds surged by more than $200 billion in the third quarter (bottom chart). Indeed, foreigners swung from net sellers of U.S. equities in Q2 ($48 billion in net sales) to large net purchasers ($130 billion) in the third quarter.

The trade-weighted value of the U.S. dollar has risen about 5 percent since the U.S. election last month, and the greenback is currently setting multiyear highs versus many individual currencies. We'll need to wait until Q4 balance of payments data are released in March to confirm, but the sharp run-up in the U.S. stock market and the appreciation of the dollar suggest that foreign purchases of U.S. assets likely has strengthened significantly in the past month.

Author

Wells Fargo Research Team

Wells Fargo