Moody’s is far more than a day late and a Dollar short

We can expect little of lasting meaning from the G7 finance ministers’ meeting in Banff.

And the jury is not yet in on the Moody’s downgrade. See the chart showing the different responses to the two previous downgrades. We think this time it will be more like the S&P event—higher yields needed to hold newly skeptical investors. After all, a slice of the “Sell America” movement is the excessive debt. Important economists predict it foreshadows The End of US world financial dominance, including the dollar.

On the other hand, Moody’s is far more than a day late and a dollar short. It’s so late in the current movement into over-indebtedness that Moody’s announcement is \quaint—and trivial.

Ratings of the US are not needed. “Modern monetary theory” says the US can issue as much debt as it wants to because it owns the printing press. It can literally always pay back the debt, even if it’s with devalued dollars. This idea runs counter to everything we think we know about economic history, but then, so do a lot of things today. And as noted before, there is a distinct shortage of alternatives, at least yield-bearing alternatives. Gold and bitcoin do not qualify. And we have been here before, and each time the press gets all hot and bothered about the deficit, things return to normal very quickly. As critics say, the US keeps getting away with breaking the rules.

You have a credit rating. I have a credit rating. Everybody has a credit rating and for good reason—can the person borrowing the money be trusted to pay it back? And does it have the means to pay it back? Trust comes first. In bank credit training, newbie bankers are taught the “3 C’s” and the first is “character.” Another one if the “Five P’s” and the first is “person.” The world is now inching toward the assumption that while the citizens would never want to default, the same can’t be said of Trump. On the other hand, TreasSec Bessent would not allow default. A dyed in the wool Wall Streeter would talk Trump out of it, right?

Deficits matter more if there is a recession that dries up tax collections and worsens the deficit, Deficits matter if they need to get remedied/alleviated in a financial crisis. Jamie Dimon still has his socks on fire. Yesterday he warned that the probability of stagflation is higher than the market now thinks, and credit spreads are failing to account for it. He’s worried about bank troubles and perhaps failures because “Credit today is a bad risk. The people who haven’t been through a major downturn are missing the point about what can happen in credit.”

And yet the bond gang seems not overly concerned about the sovereign ratings downgrade, deficits, tariffs, possible stagflation, the loss of soft power, etc. At least not yet. The bond vigilantes are not out in force. Trading is like a game to them in which they buy on dips and all the other tricks. The 30-year up near 5%? Time to buy. Bond market complacency, to be fair, arises from the sense that no other market can compete with the American bond market, and even if a few foreigners leave, there’s plenty of domestic demand.

Swiss National Bank Pres Schlegel said yesterday "There is currently no alternative" to US Treasuries, "and it's not foreseeable that there will be an alternative."

Then there is the Fed. If fiscal policy is a known, monetary policy is the known unknown. We are pretty sure we are getting inflation, so it can’t cut rates. But it must cuts rates to prevent or manage a slowdown that threatens to become a recession and raise the unemployment rate.

Everybody and his brother is pretty sure we are going to get inflation, even if it doesn’t show up for another few months. Those betting in rate cuts ruled out the June meeting, while September looks like a dead cert. But Steven Englander at Standard Chartered (another must-read guy) is cited by Bloomberg as being “…”puzzled that the market is pricing in 75bps of policy rate cuts between the September 2025 and September 2026 meetings. That period will see both tariff-induced price increases and the impact of the tax bill, which most analysts expect to add to structural deficits. We see a limited window for cutting policy rates, and we expect it to close relatively quickly.”

Two things: don’t be surprised if the Fed cuts rates in June, whatever the Fed funds bettors think. Secondly, perhaps those additional rate cut into the next year are based on the idea that the US economy is so robust that even Trump can’t harm it much. It remains to be seen if this is true. We should note that all those small companies going out of tariff-ruined business means a release of labor newly available to the bigger companies facing the labor shortage. Instead of a baby goods retail store, that lady can go work on an assembly line. Three guesses who she votes for next time.

Forecast

The trade war is not over. We are more than halfway through the 90 days with no actual deals, just a “framework” with the UK. In 2-3 weeks we need to expect Trump to deliver some more tariff upsets, as he has committed. Trump lies, so nobody is paying much attention, but we should probably be afraid.

The Moody’s downgrade is already being downgraded itself to a minor event, although it must have some effect somewhere on someone.

Given US mismanagement, the deficit, the pending stagflation, disobedience to the law, Trump’s vulgarity and cruelty, and all the rest of it, it’s hard to see the dollar getting much of a recovery.

As noted above, we shouldn’t worry too much just yet about any dollar consolidation today and tomorrow—it’s customary for the euro to give back gains that were driven by a shock. Or, if the Moody’s downgrade is a triviality as some say, the move can fizzle. Because of the holiday on Monday and the unreliability of Trump keeping his mouth shut, we may not know until a week from now.

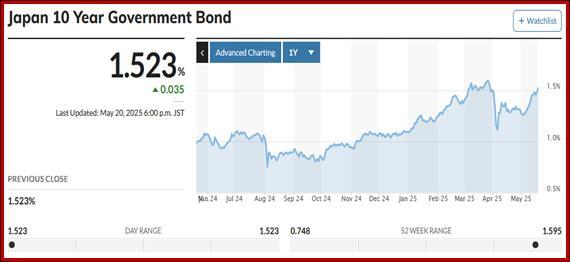

Tidbit: Japan has a worse deficit situation than the US. The PM just told parliament that taxes cannot be cut when the deficit is at a historic high, even if it might be nice ahead of July elections. The debt-to-GDP is a whopping 250%.

The latest 20-year JGB auction was a flop and set off a sell-off, with the yield the highest since 2000, according to Reuters. See the one-year high-low range—nearly double. The 30-year also jumped to “the highest this century.”

This is the shiny new thing getting headlines today, but honestly, we have been here before and it’s not all that relevant to the US situation and not the top factor in the dollar/yen, either.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat