Money supply expansion: This is inflation

Despite the prevailing notion that the Federal Reserve has implemented “tight” monetary policy, the money supply has expanded by more than $600 billion since its low point in mid-2023.

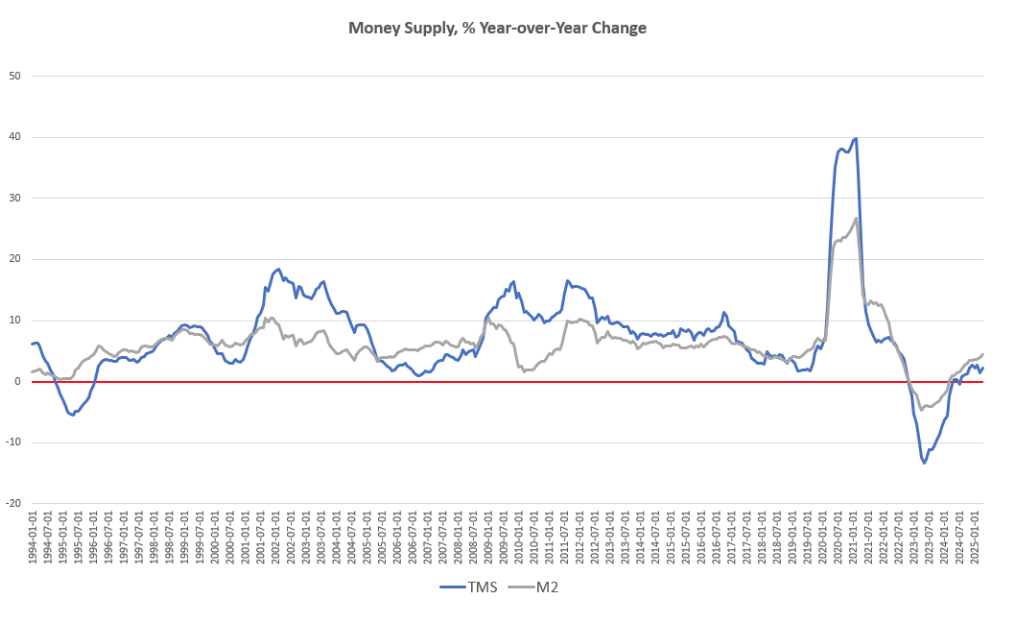

Based on the “true,” or Rothbard-Salerno, money supply measure (TMS), the money supply expanded by 2.2 percent year-over-year in April. That was up from a 1.4 percent increase in March.

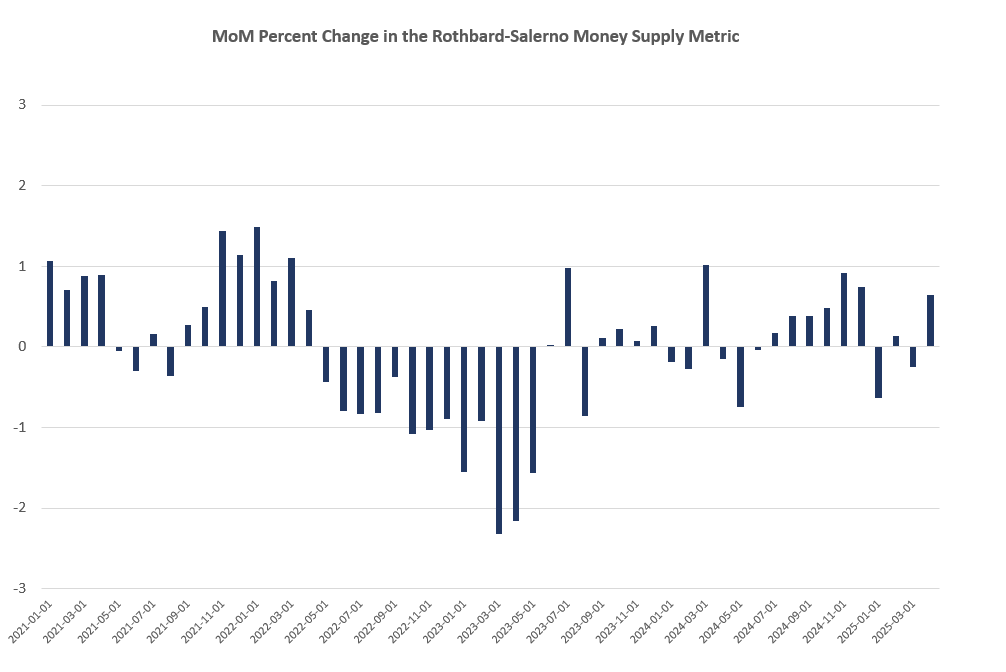

On a month-on-month basis, the money supply grew 0.6 percent from March to April. Over the past year, it has increased month over month during eight of the 12 months.

Economists Murray Rothbard and Joseph Salerno developed the TMS metric to provide a more accurate measure of money supply fluctuations.

Money supply growth as measured by the Fed’s M2 metric is surging even faster. Year-over-year, it grew by 4.5 percent, up from 3.9 percent in March.

As of May, the M2 money supply stood at $21.94 trillion and is above the peak reached during the pandemic.

As you can see from the chart, M2 and the TMS measures both show a similar money supply trajectory – up.

Looking at the bigger picture, we can see just how much the central bank has expanded the money supply.

There was a massive spike during the COVID era, when the Fed injected nearly $5 trillion into the money supply through quantitative easing (QE) alone. That was on top of the nearly $4 trillion in QE injected during the Great Recession. This doesn’t even account for the new money created by lending incentivized by well over a decade of zero percent interest rates.

Mises Institute Ryan McMaken explained just how much the money supply has expanded since the 2008 financial crisis.

“Since 2009, the TMS money supply is now up by nearly 194 percent. (M2 has grown by nearly 156 percent in that period.) Out of the current money supply of $19.4 trillion, nearly 26 percent of that has been created since January 2020. Since 2009, in the wake of the global financial crisis, more than $12 trillion of the current money supply has been created. In other words, nearly two-thirds of the total existing money supply have been created just in the past thirteen years.”

This is inflation

Despite this, President Trump and many others have been highly critical of Jerome Powell and the Federal Reserve for holding rates higher. They argue that CPI and other inflation indicators prove that the inflation dragon is dead.

However, given the expansion of the money supply, one could argue that the central bank never did enough to put inflation in the grave.

During the Fed’s inflation fight, the M2 money supply contracted. This is exactly what needs to happen to wring out inflation from the economy. The money supply bottomed a little over a year ago at $20.60 trillion.

That sounds like an impressive inflation fight, until you realize that the money supply would need to fall by at least another $3 trillion to get back to the trend of 2019. Clearly, that’s not the trajectory.

While inflation watchers focus almost exclusively on price measures such as the CPI, an expanding money supply drives price inflation. In fact, inflation used to be defined as an increase in the amount of money and credit in the economy, or more succinctly, an expansion in the money supply.

Economist Ludwig von Mises defined it this way in his essay "Inflation: An Unworkable Fiscal Policy":

Inflation, as this term was always used everywhere and especially in this country, means increasing the quantity of money and bank notes in circulation and the quantity of bank deposits subject to check.

Henry Hazlitt is best known for his brilliant book Economics in One Lesson. In another essay titled “Inflation in One Page,” he explained why using a more precise definition of inflation is crucial.

Inflation is an increase in the quantity of money and credit. Its chief consequence is soaring prices.

Therefore inflation—if we misuse the term to mean the rising prices themselves—is caused solely by printing more money. For this the government’s monetary policies are entirely responsible. (Emphasis added)

This confusion of terms is precisely why so many people believe inflation is a thing of the past. They are only looking at one symptom of inflation (rising prices), completely ignoring the inflation pumping into the system as you read this.

Here’s the rub: those calling for lower rates aren’t wrong. The U.S. economy is addicted to easy money. It is loaded up with debt and simply can't function in a normal interest rate environment over the long term. Higher interest rates don’t play well with massive levels of debt.

A higher interest rate environment will eventually crack the debt-riddled economy and pop the bubbles. The economy needs its easy money drug. However, a few good CPI reports notwithstanding, inflation is far from dead.

Simply put, the Federal Reserve is in a Catch-22. It simultaneously needs to cut rates to prop up the easy money-addicted economy and hold rates steady (or even raise them) to keep inflation at bay.

Powell and his fellow central bankers have been walking this tightrope for quite a while. He acknowledged it in April during a speech at the Economic Club of Chicago. As the AP described it, “The Fed would essentially have to choose whether to keep interest rates high to fight inflation or cut them to spur growth and hiring.”

“Our tool only does one of those two things at the same time,” Powell said during a Q&A session.

History indicates that the central bank will ultimately cave and pick inflation. In fact, it already has.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

Author

Mike Maharrey

Money Metals Exchange

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.