Moderation in all things – Except consumer spending

Summary

Today's retail sales report for December showed consumer spending picked up speed in the final month of the year. Not all the dollars spent found their way into holiday spending categories, but a surge in control group sales means upside risk for Q4 PCE forecasts.

December to remember sales event

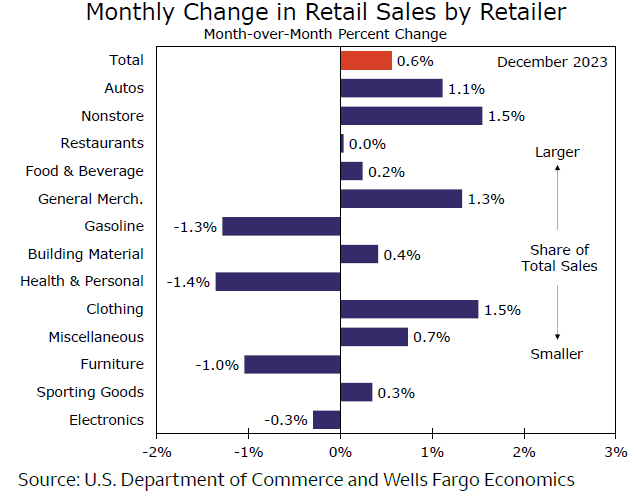

For anyone thinking that the consumer was losing momentum at the end of last year, think again. Retail sales rose 0.6% in December, handily exceeding expectations. Auto sales were expected to be a key driver, and that category was indeed up 1.1% in the month, but the strength extended beyond motor vehicle sales (chart).

The biggest monthly gains, in fact, were reserved for some of the categories that comprise holiday shopping. The biggest percentage gainer was department stores where cashiers rang up 3.0% more sales in December. Clothing stores tied for second place with a 1.5% increase in December. Clothing store sales were up 4.3% over the past year which means that more than a quarter of all last year's sales at clothing stores occurred in December, at least in dollar terms.

Although a lot of holiday shopping took place in person this year, e-commerce still saw gains with a 1.5% increase in December, enough to tie the percentage gain at clothing stores (e-commerce is almost four times the size of clothing stores).

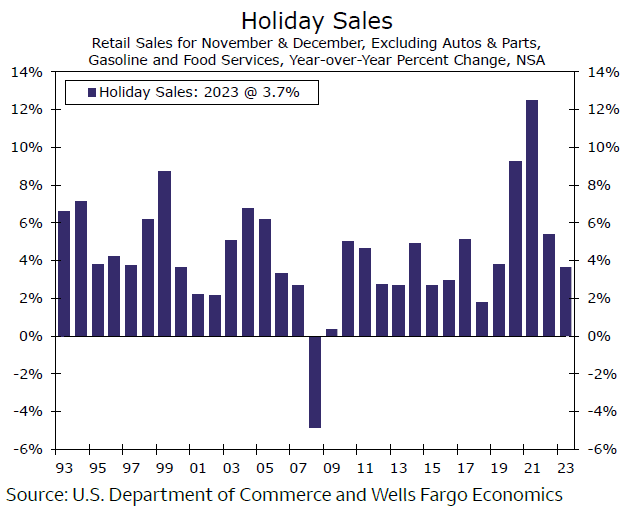

Overall our measure of holiday sales, which includes total retail sales less sales at auto dealers, gasoline stations and restaurants, rose 0.7% in December (10.5% on a non-seasonally adjusted basis). Holiday sales were thus up nearly 4% over last year, which is slightly below our initial estimate for a 5% annual gain. As seen in the nearby chart, this puts the 2023 holiday sales season essentially in line with the pre-pandemic average.

Cruising control

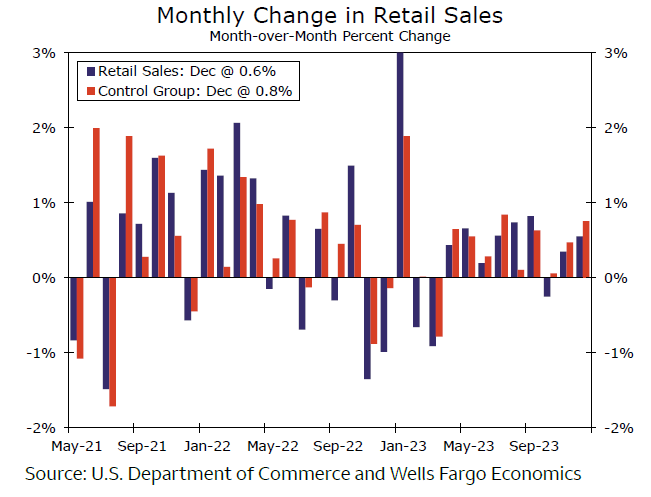

Control group sales, which are the best read for personal spending in the GDP accounts, rose 0.8%, and these retailers saw sales revised higher in November as well (chart). Once adjusting the estimates for inflation, these data suggest modest upside to Q4 real personal spending. That is, our measure of inflation-adjusted retail sales rose at a 3.5% annualized pace in Q4, compared to an estimated 3.3% prior to today's release. This implies some upside risk to our estimate for total real personal consumption expenditures to rise 2.2% in Q4. We'll get the full personal income and spending release next week in which we'll get a cleaner read on the larger services side of consumption.

Yet, with 12 full months of data, some patterns are evident in the composition of retail sales. More than any other category, the one that saw the largest gain in 2023 was bars and restaurants, which were up 11.3%. As this is the lone services category in this release, it shows that while goods spending remained resilient in 2023, there was an ongoing wallet transition back to services happening under the surface. A distant second and third place finish go to health and personal care stores (+8.5%) and ecommerce (+8.0%).

Overall it appears that the staying power that has helped prop up spending over the past year remains. It may be shifting away from excess liquidity to a reliance on borrowing and real income growth, but it's intact as consumer resilience helped stave off an economic contraction. For 2024, we still anticipate a moderation in spending as most likely. As the labor market continues to moderate, we expect to see renewed pressure on real disposable income. At the same time, households' reliance on borrowing does not look like a sustainable source of purchasing power ahead.

Author

Wells Fargo Research Team

Wells Fargo