Mixed outlook for Metals – Base VS precious

The Commodity market is mixed, with precious metals finding a near-term lift following the announcement of a double QE program from RBNZ, the comments from Fed Chair Powell on Wednesday and the US Jobless claim release this week. Gold spiked today to its April 23 high at the $1,738 level on safe haven demand, but interestingly according to RBC the poor jobs data yesterday has translated to a boost for Gold. According to RBC comments to Bloomberg, the jobless claims, from the human perspective, translated to more stimulus in the near future and to continued lower interest rates , and things that are ‘very friendly for gold’.

The concerns for more stimulus measures to cushion the fall out of the coronavirus outbreak were also raised after the mixed Chinese data, with production rebounding while retail sales remain under pressure. Chinese production figures are normally considered a bellwether data release, both for the Asia-Pacific region and the globe, though the scope for an enduring recovery in activity looks to be limited, with many world economies remaining in a state of semi-lockdown. Hence the uneven recovery picture from China signalled a still bumpy road ahead, especially as new virus hotspots seem to be emerging.

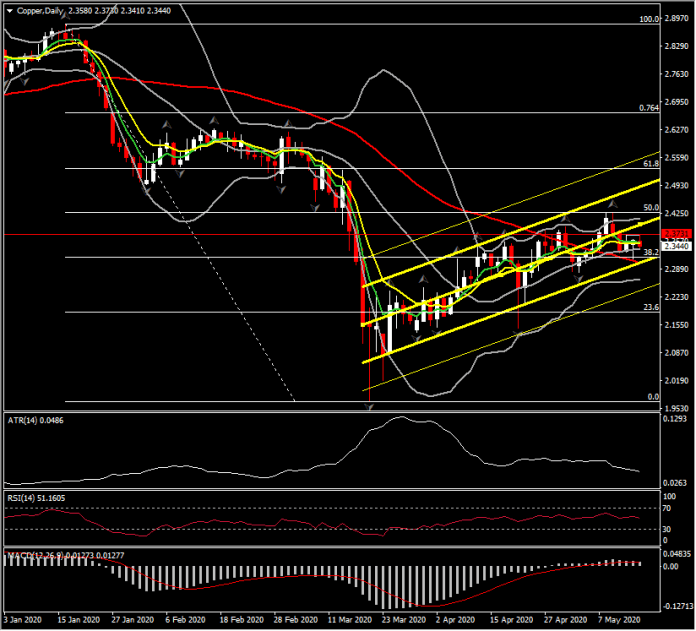

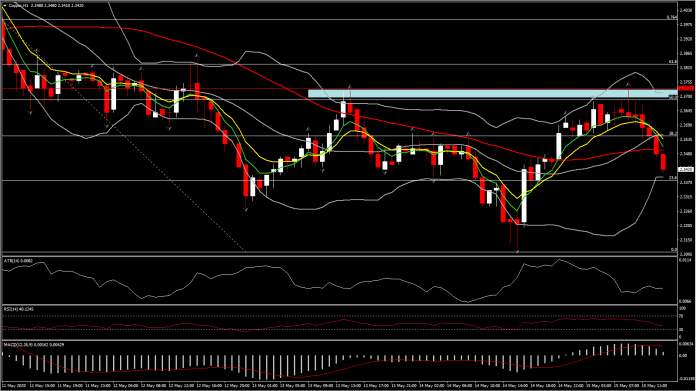

Copper

Other than Gold, Copper prices advanced today on data showing a solid recovery in top consumer China and hopes of more stimulus measures in the global economy. Copper retested the week’s high at 2.3731 (above 50% retracement level on downleg from 2.4270). However from the technical and fundamental perspective , Copper in contrast with Gold faces a limited boost. The 50% retracement level could provide a reversal level for the asset, while from the fundamental perspective, the large copper inventory inflows into LME warehouses and reports of the restarting of mining operations in Peru are adding to the overall bearish sentiment for the asset. As ING stated, LME warehouses yesterday saw copper inflows of around 55.7kt. These large inflows made up for the withdrawals that the market had been seeing since mid-April, and pushed inventories to YTD highs of 282.7kt.

However, for all commodities and energy assets, demand hits and supply hits are what matters the most .Hence for as long as the economy doesn’t get back to pre-virus levels and as long as smelters and refiners do not resume full operations in China, raw materials are expected to remain in tight supply.

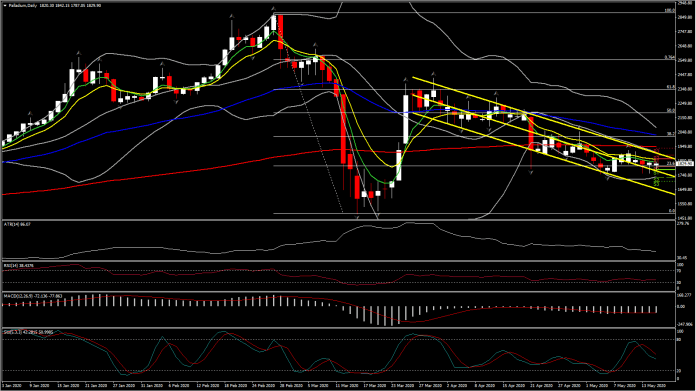

Other precious metals including platinum and palladium are also suffering from weak industrial demand amid lockdowns around the world. Price movements for all three have been negative year to date. Palladium prices have fallen around 35% from the recent highs seen in February, given the pressure that the global auto industry is under at the moment – a key source of demand for palladium.

Therefore, beyond this near-term lift, we assume that the demand-hit from the coronavirus will remain bigger than the supply hit into mid-year, leaving a downward impact on net for global commodity prices. A firm Dollar provides an additional headwind.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in