Mirror, mirror on the wall

Emboldened by the praises bestowed upon it by the magical mirror, but also by the casually favourable economic and agricultural cycle, the Romanian government has found itself prepared to take the Romanian nation to the next level of prosperity. And it did it urgently. Or perhaps the urgency was actually due to another fact, reflected by the harsh reality of a budget execution which at the end of November has already cumulated 2.7% of GDP, leaving for December a net spending of 2.5 bln RON, i.e. less than half of November's deficit, something that was not possible to achieve ever since we have data on execution of the general consolidated budget. Or perhaps the urgency came from the need to construct a budget for 2019 where special dividends, savings on investment spending and special refunds from the European Union could no longer make up for the increase of the personnel and social assistance expenditures, especially in the context of the implementation of the new pensions law and of the slowdown in nominal GDP growth that even de National Prognosis Commission expects, from 10.6% in 2018 to 7.7% in 2019. Maybe we will have an answer for the rationale behind the swift adoption of the recent deep measures once we have final execution data for the 2018 budget and the details of the 2019 budget plan. Or maybe not. In the meantime, what we know is that with the adoption of the Emergency Ordinance 114/2018, the Romanian financial system is indeed confronted with an emergency situation. First and foremost, this is because urgent clarifications are needed on several fronts in order for the financial system to function under normal parameters. In a market economy, if we indeed have one, the rules of the game must be set in advance, so that the players can play by them and set their business strategies in accordance. In case of banks, this means that there is a need to clarify whether the quotas set in the EO 114/2018 are calculated quarterly or annually. In case of quarterly calculation, at the current ROBOR levels, the tax would amount to an estimated 70% of the 2018 profit for the banking system, a fiscal burden unheard of by the private sector, at least in the civilised world. Even if ROBOR would fall below 3%, since it can't fall lower than 2.5% which is the floor set by the NBR's policy rate, the bank financial asset tax would still be the highest in Europe if calculated quarterly, even though Romania has the lowest financial intermediation in the EU. For banks, clarifications are also needed with respect to another package of laws passed by Parliament – by „coincidence", on the same day as the EO 114 –, among which there is one which introduces a cap on Annual Percentage Rate for mortgage rates at the NBR policy rate plus 3%. Such a level is below the current average mortgage lending APR and it will certainly constrain the supply of mortgages, especially those at fixed interest rates.

Clarifications are also needed for and by the National Bank of Romania, which through its setting of the policy interest rate and through its liquidity and forex operations exerts a major impact on ROBOR rates. Given the link introduced between those ROBOR rates and the bank tax, will the central bank act as a fiscal agent of the state or will it be exclusively guided by monetary policy considerations when setting the policy rate and deciding on its market operations? Also, what will the NBR do when a conflict will arise between monetary policy and financial stability objectives, such as in the case when rising inflationary pressures will require a higher policy rate, but a higher rate will lead to a much higher tax rate for banks, affecting their solvency ratios and their financial resilience in the face of shocks?

For managers of Second Pillar pension funds and even for contributors in those funds, clarifications are an existential matter, as the current form of legislative changes has transformed the management of these funds into a liability, given that the revenues arising from the business have been drastically reduced, while capital requirements have been severely raised, while simultaneously an exit option was offered to clients (but only for their future contributions). Under such circumstances, the mandatory private pensions system as we know it has been de facto disintegrated, without however the "disintegration" process being an orderly and planned process, as was the case in Hungary and partially in Poland, which were probably the inspiration for the Romanian authorities. In such a process, the Financial Supervisory Authority should definitely have a say, given the high asset volumes managed by pension funds and their significant holdings of shares in the largest companies listed on the local stock exchange.

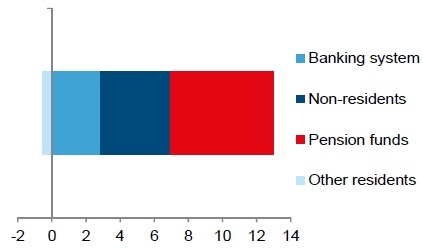

In the above context, when the ability to buy local government bonds will most likely be impaired for the two local investor categories (banks and pensions funds) which together hold almost two thirds of local market debt and which in the year between September 2017 and September 2018 were responsible for 72% of the purchases financing the increase in outstanding local currency government bonds, there is also a need for the state's treasury to clarify its financing strategy for 2019 and beyond.

If we move further to other sectors, major uncertainties are also present, for instance in the case of the announced capping of the electricity prices. In the Energy and Telecom sectors, private operators certainly need clarifications with respect to the Romanian authorities' attitude towards investments in those sectors: if these operators should face the permanent danger of new taxes and price ceilings being introduced overnight, why should they bother to make such investments? The situation of the state-owned companies in the Energy and Utilities sector is also becoming fuzzier and fuzzier given the new regulations, but also the clear contradiction between the much needed infrastructure investments and their continued haemorrhage of capital through the special dividends having become regular ones.

These are a lot of questions that are so far left unanswered and which create an environment of uncertainty which by itself is likely to discourage private investments, especially foreign ones. And this comes at a time when Romania actually needs those investments more than any time in the last 10 years, not only for boosting its economic growth and its longterm potential, but also for the short-term financing of its fast rising current account deficit, which seems on course to breach 4% of GDP already in 2018. If the wage and consumption led growth model will continue also in the next year, this deficit will continue to rise and its financing will become more and more difficult. If on top of that the central bank will also implement an exchange rate stability policy, the country's international reserves could enter a downward trend, which combined with the other elements of the business and economic environment will sooner or later raise the flags for the rating agencies. If the latter were to put Romania on watch together with vulnerable Emergencies and especially if they were to downgrade Romania from the current investment grade rating to a speculative grade rating, the spiral of negative economic consequences will become very difficult to reverse.

Given the above mentioned uncertain environment, it's most difficult to make macroeconomic predictions, especially in a year when also two elections rounds will be also held. As such, I will only mention a few directions in which we can expect economic and financial indicators to head, without at this stage settling for new point forecasts. With respect to GDP growth, we see few reasons why the current slowdown trend should reverse into 2019. Before the recent changes, we were expecting a GDP growth of 3.4%, but in light of the new measures (in case they remain unaltered), we would hardly expect growth to exceed 3%. This is because bank lending is to step into a lower gear, given the multiple hits faced not only by the supply side, but also by the demand side – among which some impact will also come from the enforcement of the central bank's new regulation on the indebtedness level. The harshness and the sudden nature of the fiscal measures is also likely to lead to some degree of bank disintermediation and the rise of risk premia for local entities, which are likely to affect economic growth prospects. Coming against the prospects of global and European growth slowdown, Romanian GDP could advance by a maximum of 2.5%, unless above mentioned effects were to be partially offset by a strong recovery of public investments. The latter remain elusive for some years now and they will continue to be constrained by a limited fiscal space in the budget and by the revealed lack of coordination between various branches of the public authorities in the face of the challenge to move investment projects forward. With respect to inflation, there will be some favorable impact coming from capping of energy prices and lower VAT on some regulated services, but these should be at least partly offset by other upward pressures, such as those coming from rising excise taxes (on tobacco, alcohol, car fuel and energy), as well as potential materialization of risks to meat prices (swine fever), pass-through of turnover taxes (especially in telecom) and the exchange rate. On balance we expect inflation to end this year at around 3%. At this level and given the likely GDP growth slowdown, the central bank is unlikely to change the monetary policy rate this year, even if the recent fiscal changes are likely to diminish potential GDP growth and thus maintain the output gap at a significant positive level, which would ceteris paribus justify some policy intervention. It is therefore quite likely that 3M and 6M ROBOR rates to remain stable or even decline to a range between 2.5%-3%. As it happens however every time the state makes a brutal but partial intervention in the economy, when it constrains a market it moves the pressure to another channel. The first such escape route would lead to the exchange rate channel, which as mentioned before would reflect especially the rising external imbalances. If the NBR were to block that channel via forex interventions, the pressure would move back to interest rates, but instead of the over-regulated money market rates it would be rather the less regulated and often more liquid segment of the market which would be hurt, i.e. that of financial instruments traded by non-resident investors, such as Fx swaps or Fx forwards. RON financing for these investors would thus become scarce, which would constrain their interest in entering the local bond market. Combine that with the above mentioned weakening capacity of banks and pension funds in increasing their demand for local government paper, but also with the unconstrained financing need of the state, in the context of a planned deficit that seems to remain stuck at the magical GDP 3% level, despite Romania's commitment to the European Commission to start reducing it as of 2019. The result is that government bond yields would have to rise sharply in order to keep foreign investors interested to buy, especially when longterm paper is concerned. Given such considerations, as well as the obvious need to help rebalance the external commercial accounts, we think that some leu depreciation, to the tune of 2%-3% should rationally be allowed to happen in 2019 if external market conditions will require it. In such a case bond yields would rise less, with the magnitude of such rises depending on global market circumstances and the concrete developments of the Romanian state's financing needs, especially in the context of the 2019 budget execution.

Overall, Romania's balancing act in 2019 will look something like walking on a tightrope above a safety net that has started to crack. Any wind gust will become adverse and can cause an economic and financial accident. Such dangers however are not to be seen Through the Looking-Glass, where Alice imagines herself to become a queen. There, in the world of fairytales, books (including Economics textbooks) are read upside down, Don Quijote is fighting imaginary enemies in order to justify his status as knight, while the boy who cries wolf one too many times is no longer believed to be a true herald. Maybe is such a world I would also be able to escape my middle-age crisis, by imagining myself in my peak years of mental and physical capacities. Except I would have to wake up sometime in the mid-nineties, when in Romania prices were still being controlled by the state and yet inflation was running at two and sometimes even three digits, banks were mostly state-owned and were offering preferential loans to influent people that were never going to return them, the National Bank of Romania had only flimsy international reserves, the favourite slogan of the politicians was „We won't sell our country to foreigners!", even though the country was actually mired in extreme poverty. Well, Alice, I think it's time to shake that Red Queen and transform it back into a black kitten and meanwhile get back to the real world...

Macro Monitor

Slower economic growth to ricochet on budget deficit

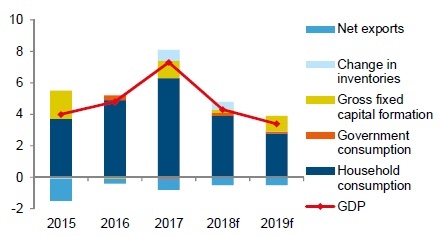

With a weak structure of economic growth in 2Q18 and 3Q18 already behind us (the unusually high contribution of change in inventories to real GDP puzzled us here), a key question is what the economic growth will look like in 2019. Our scenario about an economic slowdown is unchanged because we think that both the domestic and external growth engines will deteriorate next year. Recent signals from Romania's main trade and investment partner, the Eurozone, are negative and PMI indicators reached multi-year lows in December. While part of the Eurozone's slowdown in December reflected the transitory effects associated with the protests in France, core issues already lasting for some time, like Brexit, the trade war between the US and China and political tensions within Europe weighed on businesses across the Eurozone.

Domestic demand does not look great either in 2019, as the effects of the fiscal stimulus already started to wear off and household consumption is set for a lasting slowdown. With 2018 another lost year in terms of investments, our forecast about a recovery of gross fixed capital formation looks moderately optimistic.

Graph 1: Real GDP by demand (contributions to growth, pp)

Package of controversial fiscal measures announced by government in late-December will put a damper on economic growth in 2019 and beyond if it is implemented in a harsh way. With technical details of new sector taxes and disruptive reform of the private pension system still missing and no budget for 2019 in place, it is hard to put a number of this year's economic growth. From what we see now, we could cut our economic growth forecast below 3% in 2019 (our current estimate is 3.4%).

Will inflation be bright spot in 2019?

After entering the target in November at 3.4% y/y, inflation could remain there in the coming quarters in the absence of strong supply-side shocks. Temporary upside pressures could emerge at the beginning of next year, explained by increases in excise taxes for tobacco, alcohol, car fuel and energy. Core inflation has also been on a slight downward trend in recent months, reaching 2.6% y/y in November and alleviating most of the pressure on the NBR to hike rates.

Graph 2: Inflation and NBR's target (y/y, %)

Even if inflation is our preferred candidate for a positive surprise in 2019 among key macroeconomic variables, this does not mean that inflationary pressures are entirely gone. Our forecast shows headline inflation close to the upper limit of the NBR's target for most of 2019 (i.e. between 3% and 3.5%), making it vulnerable to agriculture, oil or taxation shocks.

Flat policy rate in 2019

We changed our outlook for the NBR's monetary policy and we now foresee the policy rate flat at 2.5% throughout 2019. Controversial path followed by government for keeping budget deficit under control will be a game changer for the monetary policy because it would reduce the space of maneuver for the NBR. A potential rate hike in the future would trigger an increase of ROBOR, affecting thus the stability of the banking sector through the tax on banks' financial assets. A potential rate cut at any moment in the future would undermine NBR's pledge to keep inflation under control and would endanger the stability of the leu in a moment when other central banks have already tightened or are planning to tighten monetary policies, making Romania an outlier in the world.

We see chances that short-term market rates would trade around the policy rate in 2019 (2.5%). Relatively volatile liquidity conditions will probably prompt the NBR to be active in the money market but its interventions will also depend on exchange rate developments. One should bear in mind that, in 2018, the 1W money market rate (mid) was below the policy rate almost half of the time. If lending will slow but deposits will continue to grow, it could be that excess liquidity will once more be the norm, hence a more benign outlook for money market rates.

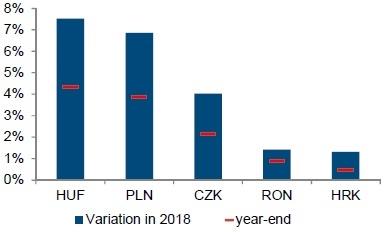

Fundamentals speak in favor of weaker leu

Leu was unusual strong in December, reaching levels close to 4.6350 around Christmas and shrugging off news about planned fiscal measures. At beginning of January, leu started to suffer but its depreciation was quite similar to other episodes from the past, making it hard to distinguish between the effects of the new fiscal measures and usual movements in the market.

We favor the scenario of gradual and modest depreciation of the leu in the coming quarters (up to 2-3%), due to risks related to twin deficits and limited capacity of the NBR to implement an independent monetary policy. A key ingredient for a weaker leu nevertheless remains the willingness of the NBR to allow higher volatility of the local currency.

Graph 3: CEE currencies in 2018 (variation interval versus euro and year-end value)

Bond monitor

Fear the unknown

If technical details of the emergency ordinance with new fiscal measures and the state budget for 2019 confirm that the government really wants to inflict serious damages to the banking sector and private pension industry, then the financing of the government's gross funding needs will be difficult. Gross funding needs are estimated at RON 76bn in 2019 (7.5% of GDP), almost unchanged as a percent of GDP in the past two years.

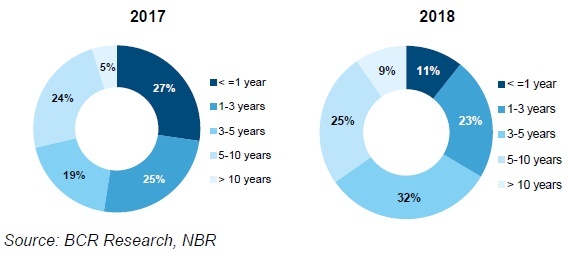

Graph 4: Primary market bond issuance by residual maturity

In absence of the tax on banks' assets which diminishes the willingness of local banks to increase their balance sheets and with a functional private pension system in place, financing the gross funding needs would have been an easy task in 2019. Otherwise, government's dependence of foreign investors would increase significantly and long-term yields would go up because investors will have to be compensated for putting their money in an unpredictable country which risks a serious fiscal slippage at any moment.

A key issue is that in other episodes of market stress, the NBR provided additional liquidity to the market and local banks were active buyers on the primary market of government bonds. Now we might be in a position when these investors will be no longer active in the market and nonresidents would show little if none determination to buy short-term bonds. With different investors having different degrees of buying appetite on the yield curve, one should definitely think twice before removing entire classes of investors from the bond market.

Graph 5: Change in stock of RON government bonds between Sep- 17 and Sep-18 by investor type (RON bn)

Author

Erste Bank Research Team

Erste Bank

At Erste Group we greatly value transparency. Our Investor Relations team strives to provide comprehensive information with frequent updates to ensure that the details on these pages are always current.