Markets wary of a booming service sector ahead of US payrolls: It all comes down to the Fed

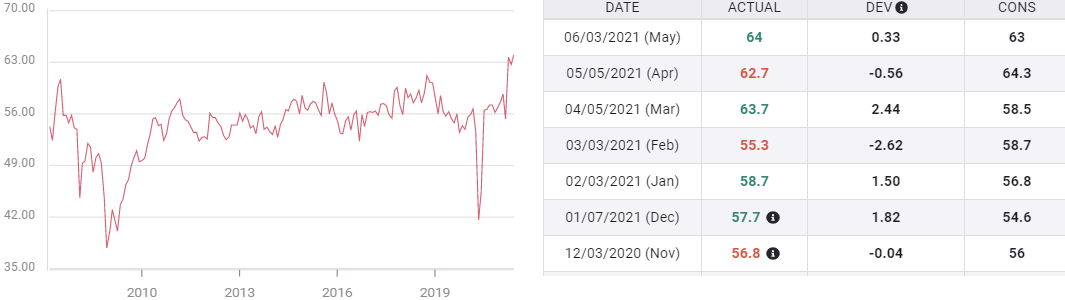

- Services PMI sets series record at 64 in May.

- Prices vault to 80.6, highest since September 2006.

- Employment Index falls despite surging business activity.

- Dollar and Treasury yields rise, equities recover to end slightly lower.

Traders were reluctant to take the excellent service sector report to the bank on Thursday, preferring to wait until Nonfarm Payrolls delivers its verdict on the US economy in May.

Despite indications that the US economy is fast shifting into overdrive, equities finished down small after recovering from early losses. Treasury yields rose modestly. The dollar was the biggest winner, gaining almost a figure on the euro and closing above 110.00 against the yen for the first time in two months.

%20june%203-637583699504422466.png)

The Purchasing Managers Index from the Institute for Supply Management (ISM) rose to 64 last month, setting an all-time record for this 24-year old series. New Orders climbed to 63.9 from 62.7 and the Prices Paid index jumped to 80.6, its highest score in 15 years. Only the Employment Index, mimicking its manufacturing cousin declined, dropping to 55.3 from 58.5. Readings over 50 indicate expansion.

Services PMI

FXStreet

Market response

Equity markets are concerned that a strong payrolls report, making up for last month’s huge disappointment, combined with surging inflation will push the Federal Reserve into curtailing and eventually ending the bond purchases that have restrained interest rates.

Instituted in March 2020 at $120 billion a month, the bond buying program has kept the short end of the yield curve stationary for more than a year.

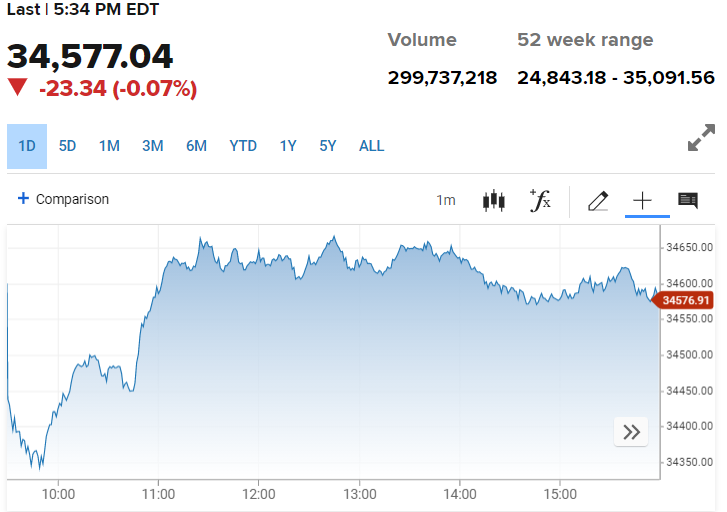

Equities dropped sharply on their open after the 8:30 am ISM release. Within 20 minutes the S&P 500 had lost 40.19 points from Wednesday’s close. After the opening plunge, the recovery was swift and by noon the average had regained almost all of its decline and finished down 15.27 points, -0.36%, at 4.192.85. The Dow shed 265.97 points in the same time frame, recovered in similar fashion and concluded at 34,566.04, off 23.34 from Wednesday, -0.07%.

Dow

CNBC

Treasury yields improved with the 5-year return adding just over 4 basis points to 0.841%, the 10-year increasing 4 points to 1.628% and the 30-year rising 1 point to 2.310%.

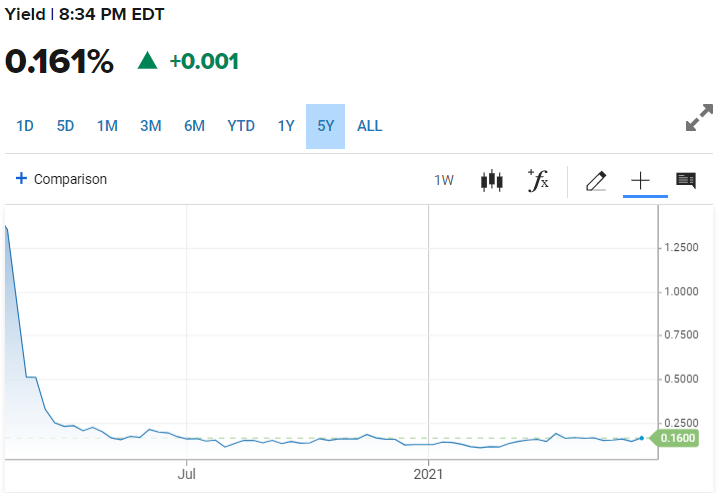

At the short end of the curve, where the Fed purchases are focused, the 2-year rose just over 1 point to 0.161% and the 3-month bill added less than a point to 0.023%.

The 2-year yield has remained unchanged for more than a year. On May 31, 2020 it closed at 0.164%, on Thursday the finish was 0.161%, a testimony to the effectiveness of the Fed’s program..

2-year Treasury Yield

CNBC

Federal Reserve policy has not interfered directly in the longer duration bonds, but the markets have been restrained by the overall intent of the governors to keep rates low until, in the words of Chair Jerome Powell, the economy and labor markets are fully recovered.

The 10-year return has more than tripled from its August 4, 2020 low close of 0.515% and is up more than 70 basis points this year, finishing at 1.627% on Thursday. It remains far from its historical range between 2% and 3%.

10-year Treasury yield

CNBC

Fed rate policy

Credit markets are waiting for the Fed to signal that the economy has recovered sufficiently to consider tapering its bond purchases. It will not take much more than a whisper from the Fed to set the bond market running, but until recently the governors, and especially Chair Powell, have steadfastly refused to provide the hint.

That may have changed with the release of the minutes of the April FOMC two weeks ago. Included was a note that “a number of participants” thought the time might be approaching “to begin discussing a plan for adjusting the pace of asset purchases.”

Since then Dallas Fed President Robert Kaplan has voiced similar sentiments.

Inflation

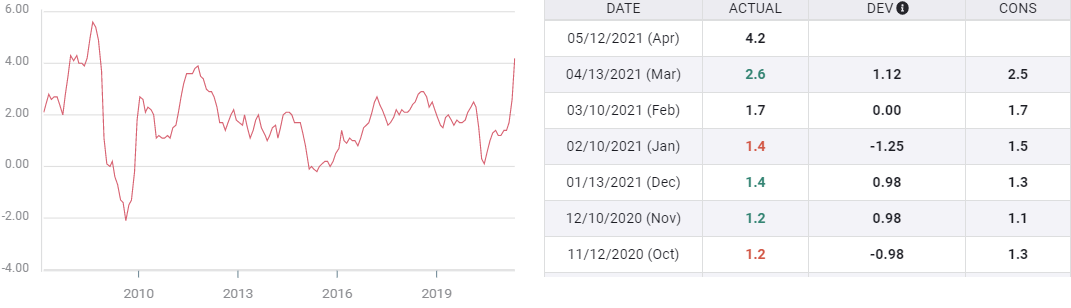

Inflation in the US has tripled this year. The Consumer Price Index (CPI) has gone from 1.4% annually in January to 4.2% in April.

CPI

The largest part of this jump in inflation is due to the statistical effect from last year’s lockdown induced price crash, as the Fed has repeatedly averred.

There are signs, however, that price gains are more widespread and caused by factors related to the sharp economic rebound and the lingering effects of the lockdowns.

Commodity prices are near a six-year high, driven by demand and anticipated demand. Wages in the US are rising as employers try to convince workers to return to jobs that are going begging. Shortages are common in many consumer goods from lumber and bicycles to cars. A scarcity of computer chips, has pushed prices higher for a wide array of products.

Conclusion

A strong NFP report, particularly when added to the inflationary tendencies swirling through the economy, may be enough to let the Fed begin the slow process of ending its pandemic monetary policy.

When pressed at the April press conference about tapering its bond purchases, Chair Powell said with uncharacteristic asperity, ‘We’ve had one great jobs report [March], that is not enough.’

Perhaps he will take two out of three.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.