Markets remain on a knife edge amidst mixed signals on trade dispute

Market Overview

You would have thought that after over three years of a Donald Trump presidency, financial markets would be rather more desensitized to trading his headlines. It would appear not, certainly not looking at market moves of recent days. As the deadline of the 15th December for the next round of tariffs between the US and China approaches, markets are becoming increasingly on edge again. Although unnamed US officials suggest that “phase one” is close to agreement, legislation in the US Congress still threatens the relationship, whilst Trump has thrown around some very mixed statements in recent days. We have subsequently seen volatility on equities having spiked higher this week, whilst Treasury yields have been all over the place. Major markets don’t know whether they are coming or going. After an initial move against the dollar earlier this week, several markets hang in the balance. EUR/USD is neutral around $1.1100, whilst Dollar/Yen is struggling at 109.00 again and gold is around key resistance at $1480. One such currency not in a bind is sterling, as Cable has broken out to multi-month highs and just seems to want to keep going. The breakout comes as the opinion polls seem to be wide enough in favour of the Conservatives to allow traders to now take a view. We believe this is still rather premature and that a far tighter election result is likely than is currently anticipated. Any tightening in the polls could give rise to a pullback on sterling, but for now, traders seem adamant to back a Tory win. Watch out for further volatility on oil in the coming days with the OPEC meeting today, followed by OPEC + (i.e. to include Russia) tomorrow.

Wall Street continued the bounce back yesterday with gains on the S&P 500 of 0.6% to 3113. US futures are a little more cautiously positive, trading +0.1% higher. This has all helped Asian markets higher, with the Nikkei +0.7% and Shanghai Composite +0.7%. In Europe, there is a mild positive reaction again with the FTSE futures +0.2% and DAX futures +0.1%. In forex, there is a relatively quiet open, with a slight hint of USD underperformance. It is interesting to see CAD continuing to perform well in the wake of the BoC decision yesterday, whilst NZD is also improved on the lighter than anticipated banking regulations. In commodities, gold is a buck higher, still under the $1480 resistance area, whilst oil is steady ahead of OPEC.

For the economic calendar, the second reading of Q3 Eurozone GDP is at 1000GMT and is expected to see no change to the prelim of +0.2% (+0.2% in Q1) or +1.2% on a year on year basis. Eurozone Retail Sales for October are expected to decline by -0.3% (after +0.1% in September) which would mean year on year growth at +2.2% (+3.1% in September). The US Trade Balance is at 1330GMT and is expected to see the deficit improve to -$48.7bn in October (from -$52.5bn in September). Weekly Jobless Claims are expected to increase marginally to 215,000 (from 211,000 last week).

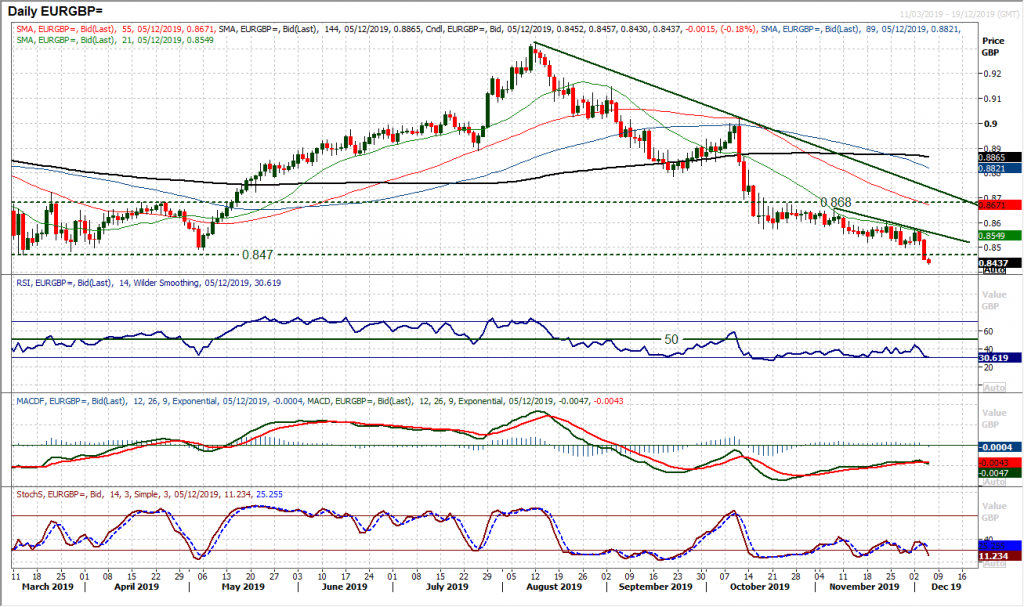

Chart of the Day – EUR/GBP

An incredible breakout on sterling across the major forex crosses has significant implications across the charts. Key moves have come against the yen, dollar and also the euro. EUR/GBP posted a decisive negative candle to see a break to a new two and a half year low. A key floor throughout Q2/Q3 2019 at £0.8470 has now given way. The question is whether the market will run with this breakdown. On a technical basis, this is a key move with downside potential on momentum indicators. RSI is again struggling in the low 30s and on big moves has moved well below 30. Furthermore, the MACD and Stochastics lines are again turning lower in bearish configuration. The hourly chart shows a near term oversold position on EUR/GBP which could induce an unwinding move initially. There is resistance around £0.8500/£0.8520, but any failure now around there or below will be seen as a potential chance to sell. It is important to caveat that this view is predicated on what seems to be market positioning for a Conservative majority in the election. Any polling data that hints at a tightening could be a drag back on sterling.

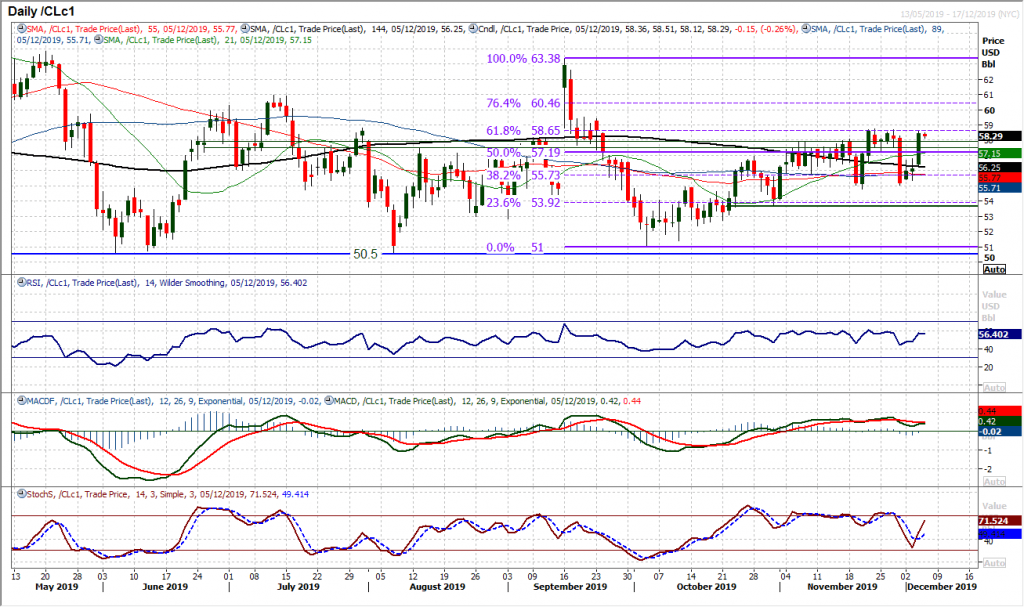

WTI Oil

As we look towards the OPEC meetings (today and OPEC+ tomorrow), oil has spiked back higher again. Over the past few weeks there have been a variety of conflicting signals on oil as traders try to weigh up the various factors at play. It means that we have been left with a very uncertain technical outlook. Taking a step back will find a continued run of higher lows, and broadly higher highs. However we see the 61.8% Fib level (of $63.40/$51.00) at 58.65 has acted as a ceiling in recent weeks. Once more this has been the case. However, unless the market can breakout, then this resistance will just strengthen. Momentum indicators are not calling for a breakout, with the RSI tight between 43/60. Can the OPEC meeting drive a catalyst for breakout? Key support at $54.75/$55.00.

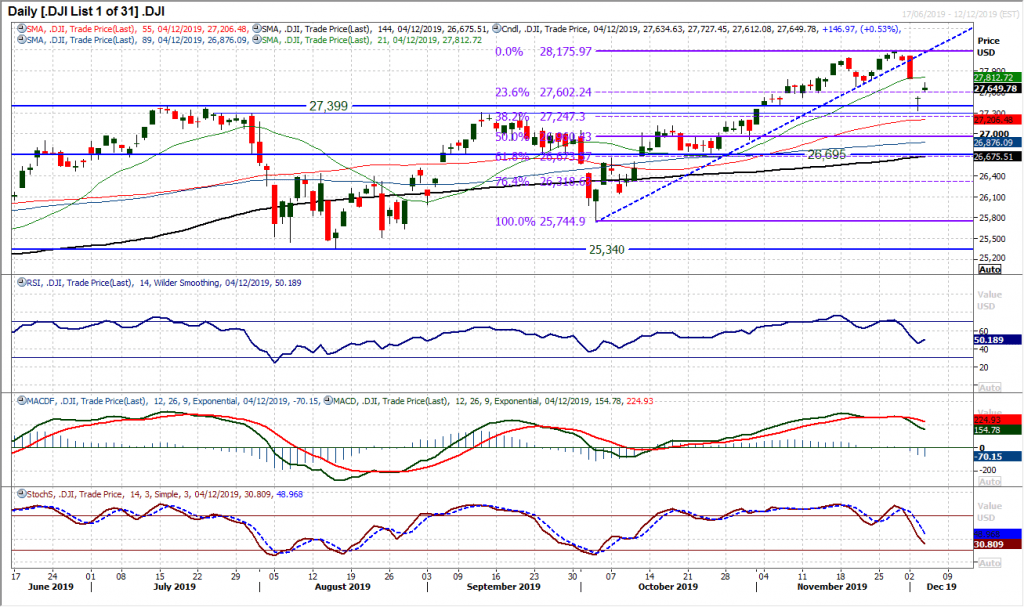

Dow Jones Industrial Average

The Dow is trading around with a significant degree of uncertainty as investors respond to conflicting reports on the trade dispute. It just looks as though they are chasing their tails at the moment. A huge gap lower on Tuesday (and a doji candlestick) was followed on Wednesday by a gap higher (with a very small candlestick body). Wednesday’s session traded entirely within Tuesday’s gap reflects the degree at which traders are struggling to make sense of it all. The old technical saying is that “gaps close” but we now have both a bull and bear gap still open. The direction of the closing of the gap could be key. So we look at the downside gap at 27,525 and the upside gap at 27,782. The fact that overhead supply at 27,675/27,725 was restrictive yesterday needs to also be considered as a problem for the bulls. US futures are flat this morning, so we are in limbo to an extent, but looking for closing one of the gaps could be the key for near term direction.

Author

Richard Perry

Independent Analyst