Markets rebounded yesterday

Highlights:

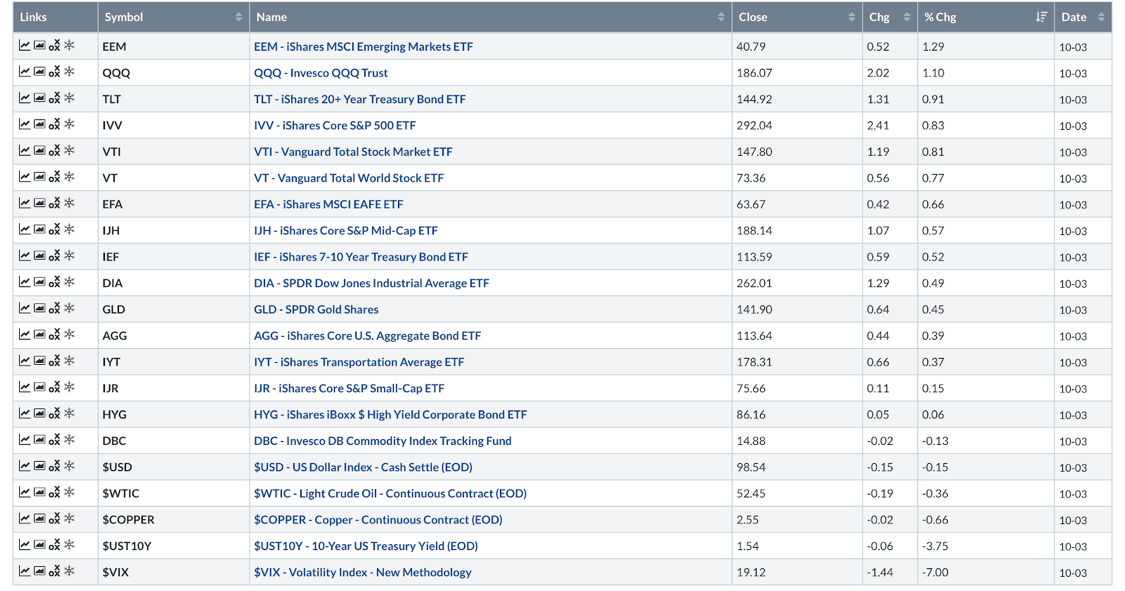

Market Recap: Markets rebounded yesterday, led by emerging markets (EEM up 1.29%). US 10 year yields continued to drop, falling -6 basis points on expectations of further rate cuts by the Fed. Global stocks (VT) were up 0.77%. The US dollar was weaker by -0.15%. Gold continued to rally, gaining 0.45%.

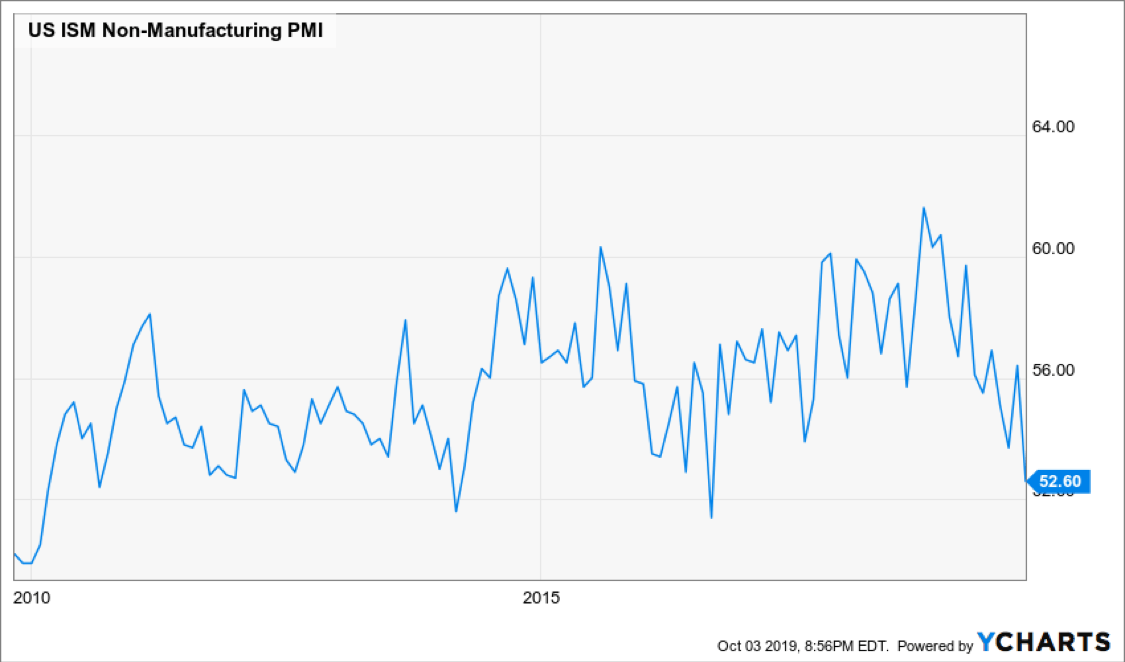

Economic Data: The ISM non-manufacturing PMI came in at 52.6, demonstrating a clear slowdown. The slowdown in the non-manufacturing sector created a significant rise in the probability of a rate cut in October for the US Fed. In our opinion, the Fed remains too tight.

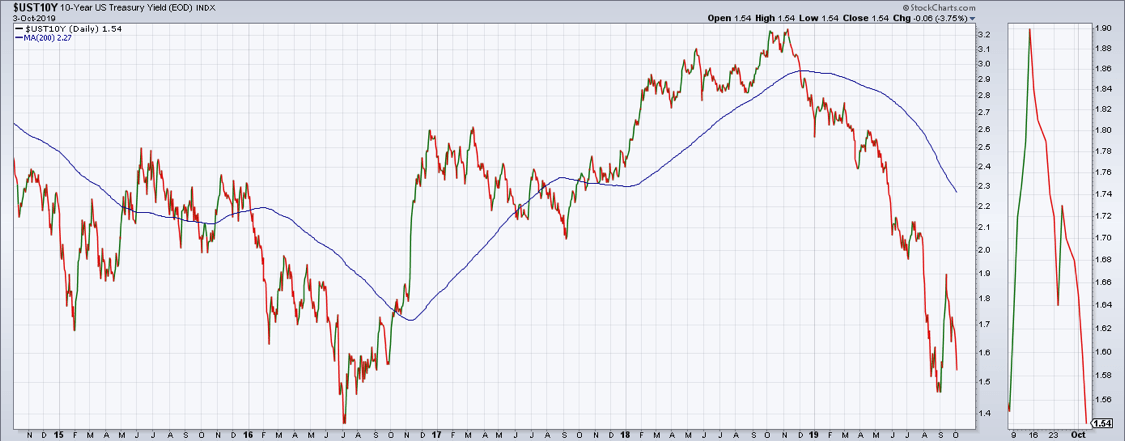

Interest Rates: Will the benchmark 10 year yield break to new 2019 lows? What about the 2016 lows? Rates remain in a negative trend and below their 200 day moving average. Compared to the rest of the developed nations in the world, the US 10 year yield is still pretty high.

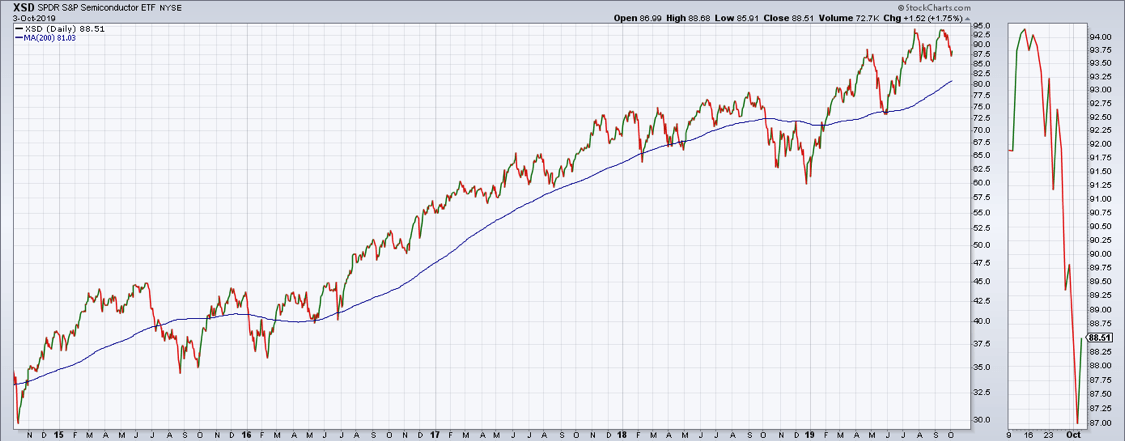

Semiconductors: Despite the recent bearishness in the market, the semiconductor sector has been strong. It was up 1.75% yesterday (XSD) and has been resilient in the face of weak fundamentals and deteriorating global economic conditions. XSD is still above its rising 200 day moving average and in a positive trend.

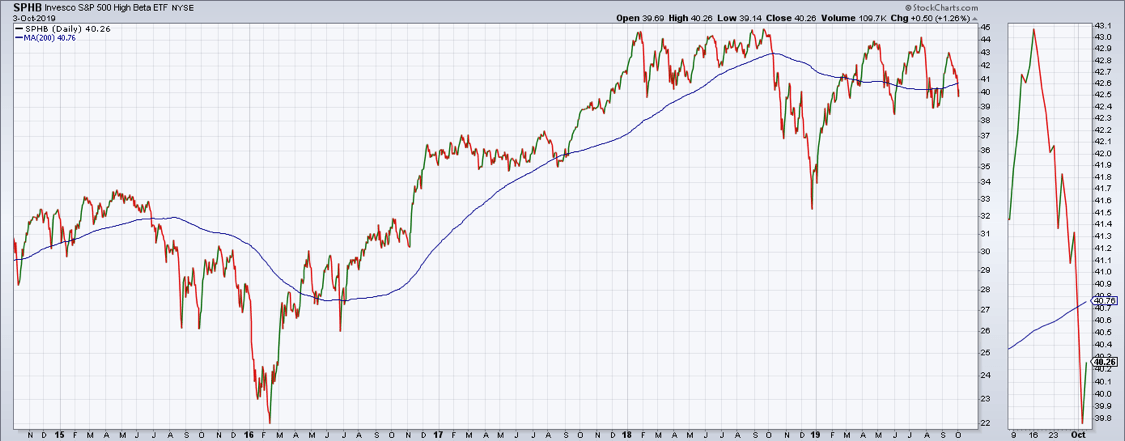

High Beta: High Beta was the top performing factor yesterday, gaining 1.26% (SPHB). However, it is below its 200 day moving average and has failed to make a new high recently. It remains in the same range it has been in since late 2017.

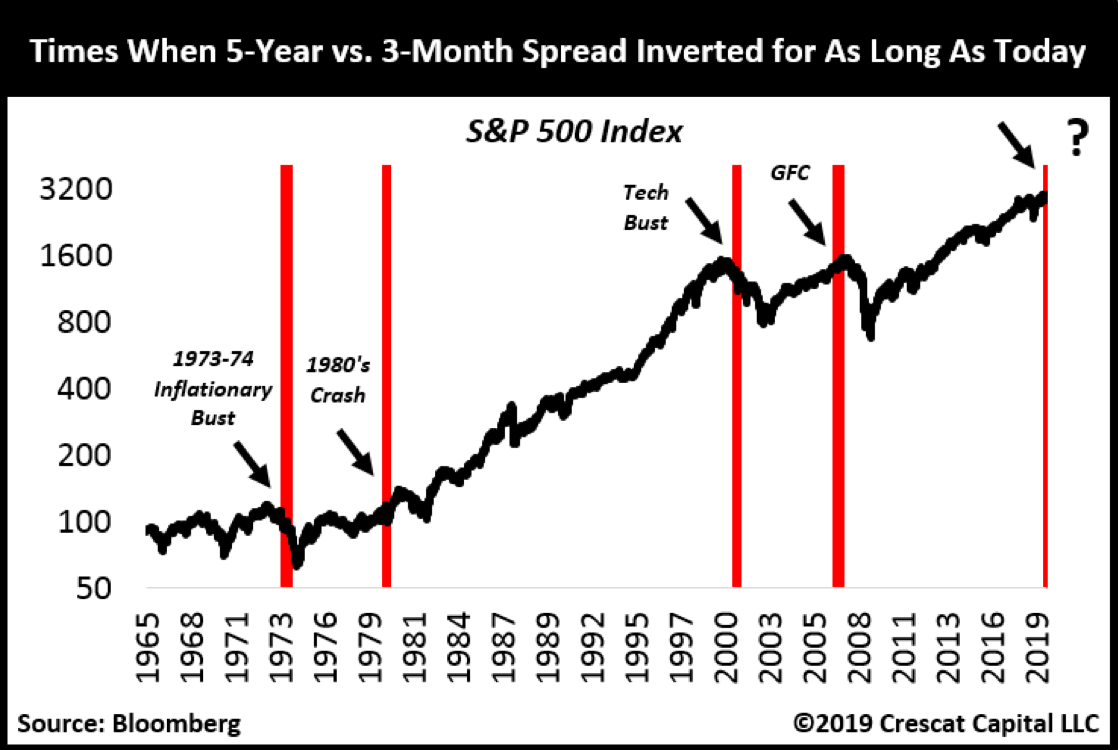

Chart of the Day: The curve has been inverted for a while now. What has happened in the past? It is a small sample size, but history is pretty scary in this instance.

Source: Crescat Capital, LLC.

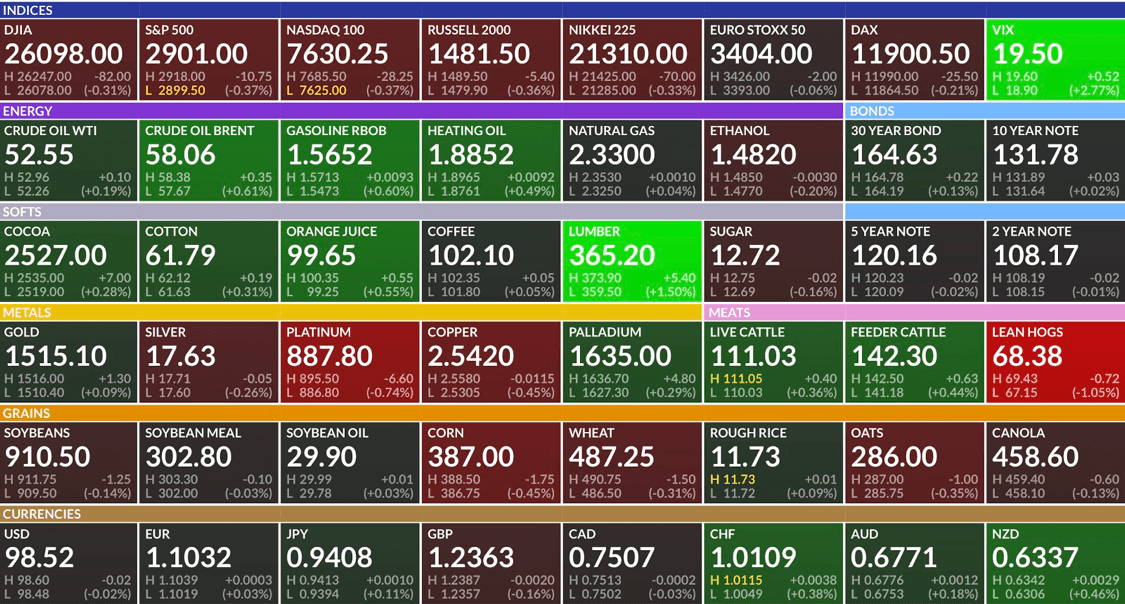

Futures Summary:

News from Bloomberg:

Storm clouds developed quickly over the labor market this week. A slew of weak data—including the lowest manufacturing jobs gauge since 2016 and slower private hiring—form the backdrop to today's jobs report. Analysts are bracing for downbeat figures, on par with times when hurricanes slammed the country in 2017 or when the government shut in 2013. Consensus for nonfarm payrolls is 145,000.

Two top U.S. diplomats sought to strike a deal on President Trump's behalf for Ukraine's leader to investigate allegations against Joe Biden and his son in return for better relations with the U.S., messages released by House Democrats show. Intelligence community watchdog Michael Atkinson gives a deposition to House panels today. Ukraine said all cases involving the Bidens are being reviewed.

Apple told suppliers to boost production of the iPhone 11 range by as much as 10% to meet stronger-than-expected demand, the Nikkei Asian Review reported. It would add 7 million to 8 million units to Apple's initial plans. The company expects to sell more iPhones in the closing months of this year than during the same period last year. Here's a review of the iPhone 11 Pro.

HP Inc. will cut up to 16% of its workforce as part of a broad restructuring. The company will eliminate 7,000 to 9,000 positions through firings and voluntary retirement to help save about $1 billion by the end of fiscal 2022. HP had 55,000 employees as of a year ago, the last time it disclosed the figure.

U.S. stock futures fell with European shares and Treasury yields ahead of the jobs report. Asian equities gained while those in Hong Kong fell after the city invoked emergency powers to ban face masks for protesters. China is still closed for a holiday. The dollar declined. Oil and gold moved higher.

Author

Clint Sorenson, CFA, CMT

WealthShield