Markets are trading as though the cut is a dead cert

The market news yesterday was only partly about the summit at the White House. Also on the radar was the creep upward in the 10-year yield that started with last week’s inflation information. The bond gang is starting to get the message that the Sept rate cut is far from a done deal—and if Mr. Powell does not deliver what Bloomberg names a “dovish tilt,” there will be hell to pay. By whom? All those swap traders betting 80% on a 25 bp cut with some going for a 50 bp cut. As of 1 pm yesterday, the CME FedWatch probability was 83.2%.

In other words, markets are trading as though the cut is a dead cert. Well, it’s not, and to make matters worse, no matter how diligently the word-watchers work, Mr. Powell is not about to give a single clue. We might have more luck with the July 30 meeting minutes tomorrow, but even then, the both the jobs and inflation data was released after that meeting.

What happens then? More dither, probably, at least until we get more data.

Reuters reports “U.S. Treasuries have been on the backfoot since the alarming U.S. producer price report last week, with 30-year bond yields holding just shy of 4.95% on Tuesday and the two-to-30 year yield curve gap firming above 117 basis points for the first time since January 2022. With July housing starts on the diary later, along with a retail update from Home Depot, Fed futures currently price just over an 80% chance of a quarter point rate cut next month.”

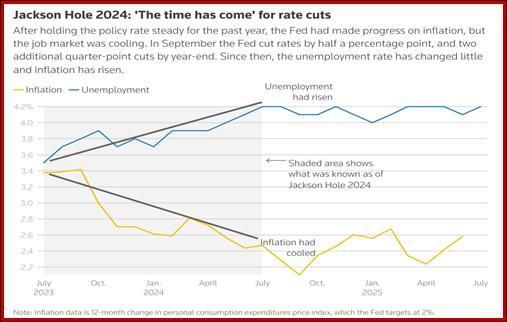

There is no planet on which this combination of outcomes makes sense—rising yields on inflation expectations plus a rate cut bet. Reuters goes some way in reconciling this puzzle with the chart showing what has happened to employment and inflation since the last Jackson Hole. Mind you, Jackson Hole is not the benchmark for anything for anyone, but it’s an interesting chart all the same. The divergence of the two measures can be interpreted to mean a rate cut is due.

The swaps and CME Fed funds betting point to a majority believing in that Sept rate cut. In equities, the old saw has it “don’t fight the tape” and we should probably give serious thought to whether that is not the right attitude in this case. Yes, rising inflation “should” keep the Fed on hold, but at the same time, interest rates have very little (or almost nothing) to do with the tariff-induced price increases about to hit. A small cut might be of some tiny help to smaller companies. The housing market would like it, too.

Note that TreasSec Bessent says rate cuts are desirable because AI is going to increase productivity. Maybe, sometime down the road, but not in the next 6 months. We say this is clutching at straws. What Bessent can do is change the rate of the Fed buying/selling Treasuries. Wait for it.

Bottom line, the bond vigilantes are adamant that a rate cut would be the wrong policy decision, while the rest of the trading world thinks it would be okay. The majority doesn’t rule, since the decision lies in the hands of the FOMC, but given these condition and the political pressure to cut, a cut is not out of the question.

This gives us a conundrum—does the dollar follow the Fed funds (down) or the 2-year and 10-year (yields higher)? Well, both. Initially, upon the release of the news, a drop in the dollar. Then, a renewed focus on inflation and a gain, possibly, on the rising yields. With the rest of the world mostly on a cutting regime, that puts the dollar return head and shoulders above the others.

Forecast

We are not convinced that the seemingly okay outcome of the summit yesterday was dollar-friendly. We are also not convinced that the Fed rate cut is as obvious as the bettors think. Powell can still dig in his heels. He has a legacy to consider, too. There is no upcoming data to dig us out of this swamp. The charts are of little help, either. Depending on what timeframe you are looking at, you can make the case to buy or sell. When in doubt, do nothing, or at least look to the cross-rates. Keep your powder dry. The primary trend is down for the dollar except against the yen and CAD, but the secondary indicates we could get a bump.

Tidbit: The White House summit yesterday demonstrated the wisdom of Zelensky bringing along seven top European leaders, five of them heads of state, to keep Trump in line. Even so, he was as giddy as a 4-year old at his birthday party, impulsively rushing off to phone Putin and telling French Pres Macron that Putin seems to want to make a deal for him.

This is an extreme of narcissistic delusion. It’s also yet another indication that Trump hasn’t read a book in decades or a briefing while in office, and knows nothing about foreign affairs or about how Putin is manipulating him.

Trump is pinballing between stances. We need a ceasefire, no, we don’t. The US will back up European troops on the ground, no it won’t. There will be consequences, no there won’t.

A “security guarantee” means something one day and something else ten minutes later. Putin, of course, bombed Ukraine again just hours after the summit. Trump fails to see the provocation. He is also ignorant of history, which reminds us that Czechoslovakia gave up some land (Sudetenland) to Russia to prevent war but got war anyway. This is not going to end well.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat