Market update: Stock futures rise, oil bounces

-

USD (USDIndex 96.36) up, as Treasuries benefited again from the flight to safety, and as some of the oversold conditions from rate hike worries were pared. Stocks struggled after a lower close on Wall Street Friday, USA100 down over -2.0%, USA500 -0.84% to 4555 & USA30 up to 34784.

-

Investors try to sort out the big risks from monetary policy, along with renewed uncertainties over Covid and the Omicron variant, and now with renewed restrictions, all the while pandemic supply/demand dislocations continue with varying impacts on growth and inflation. All this was topped off by the mixed US jobs report. The earnings season has wound down, but there has been worrisome guidance from some big tech firms.

-

Traders keep a close eye on this month’s round of central bank meetings.

-

Chinese Premier Li Keqiang signaled an easing of reserve requirements and China’s securities watchdog tried to play down fears over the withdrawal of Chinese companies from American exchanges.

-

US Yields 10-year rate is up 4.4 bp at 1.39%. UK 10-year rate lifted 4.4 bp to 1.39%, while bond markets across the Asia Pacific region were supported and the 10-year JGB rate down -1. 2bp at 0.036%.

-

USOil – steadied below 200-DMA at $68.00 – recovered from $62.24 today – rose on positive sentiment after top exporter Saudi Arabia raised prices for its crude sold to Asia and the United States, and as indirect U.-Iran talks on reviving a nuclear deal appeared to hit an impasse.

-

Gold at $1780 area, as Treasury yields soften, unwinding some of the November selloff as it was seen as overdone, and as investors move back into haven trades as angst over an aggressive Fed policy posture abates and inflation concerns ease.

-

FX markets – EURUSD dropped back to 1.1279, USDJPY lifted to 113.11 & Cable steadied to 1.3328. Antipodeans bounced.

European Open – The March 10-year Bund future is fractionally higher, while US futures are in the red, although in cash markets, the US 10-year rate is up 4.4 bp at 1.39%. Asian stock markets also traded mixed and sentiment is likely to continue to fluctuate. GER30 and UK100 futures are up 0.9% and 0.8% respectively and US futures are also posting broad gains, amid some hope that Omicron may turn out to be more infectious but less deadly than previous strains.

Today – Today’s data calendar had German manufacturing orders which plunged -6.9% m/m in October, much more than anticipated. BoE’s Broadbent speech is also on tap.

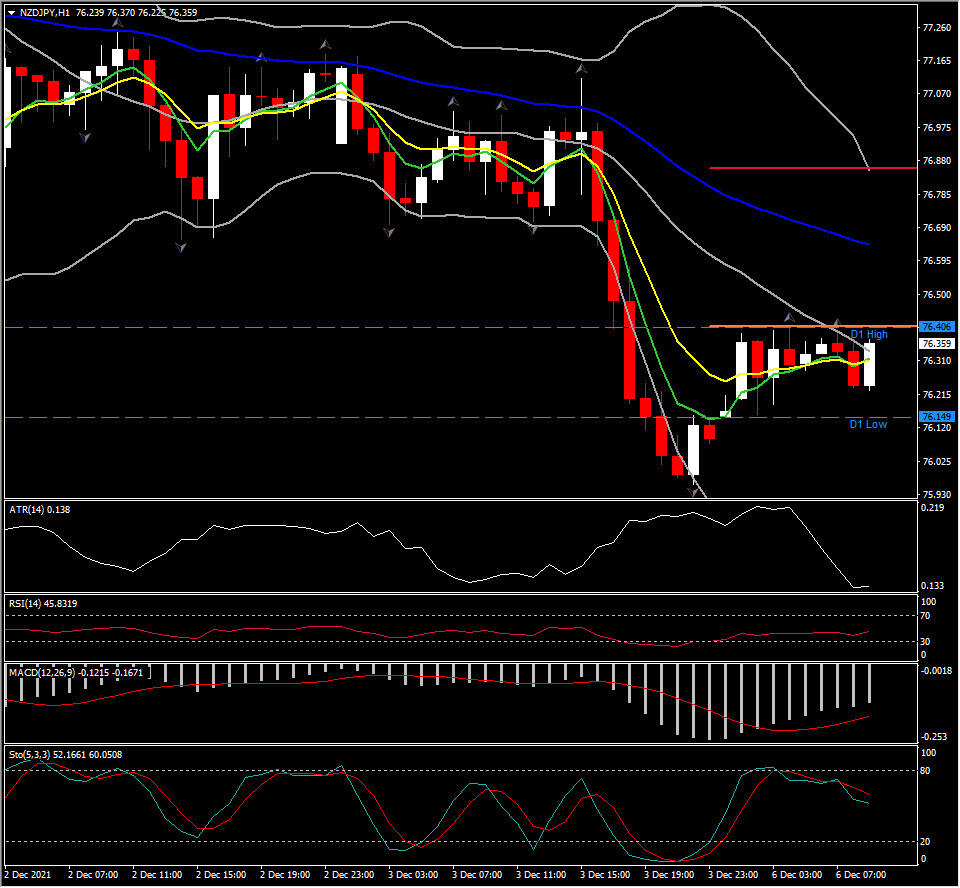

Biggest FX Mover @ (07:30 GMT) NZDJPY (+0.97%) Currently MAs flattened, MACD signal line & histogram below 0 and dipping, RSI steadied at 45, Stochastic declines. H1 ATR 0.138, Daily 0.91.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in