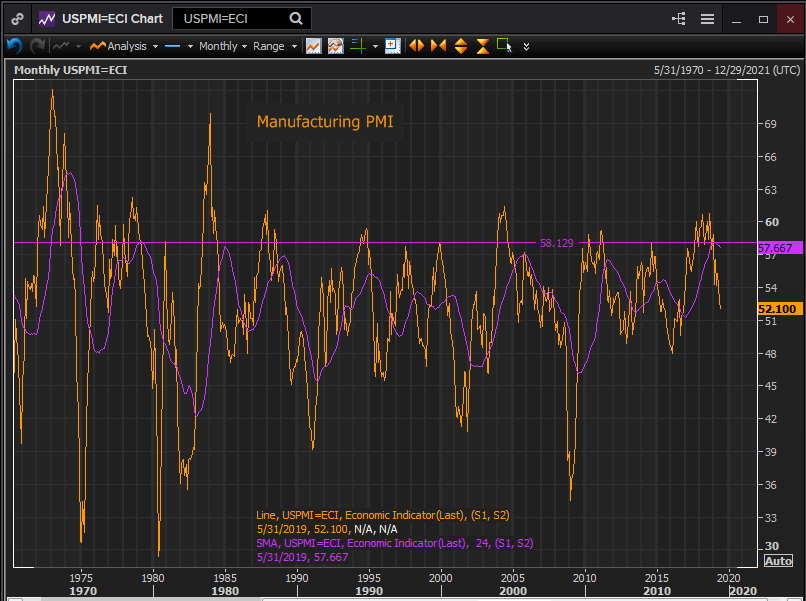

Manufacturing index slips to weakest level in 31 months

The outlook in the manufacturing sector fell to its lowest point since October 2016 as the lengthening US trade dispute with China forces a reconsideration of global and national economic growth.

The purchasing manager’s index from the Institute for Supply Management dropped to 52.1 in May from April’s 52.8, missing its median expectation of 53.0.

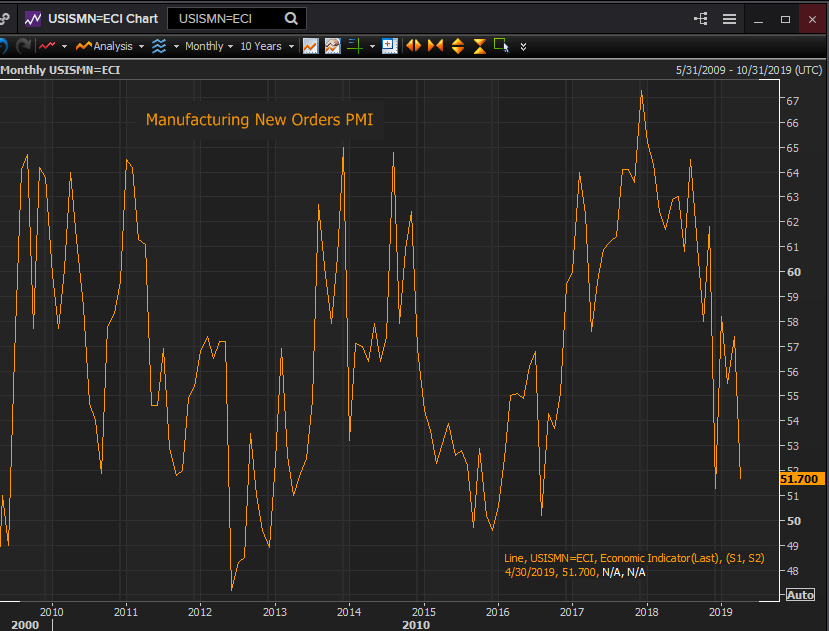

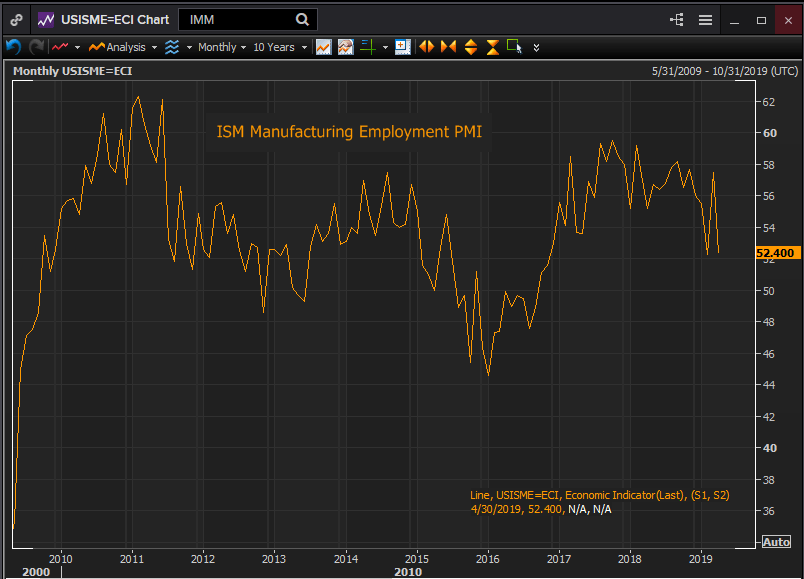

Its decline came despite a modest rebound in two of its key components. The new orders index climbed to 52.7 in May from 51.7 in April and the employment index rose to 53.7 from 52.4.

American manufacturing had it best two years in four decades to January of this year. The 24 month moving averge for the headline ISM index registered 58.129 in the first month of the year, its strongest sustained performance since April 1979.

Reuters

Business optimism had begun to decline from its record high of 61.3 in August 2018 before the partial government shutdown in January roiled sentiment indicators. Overall PMI fell to 54.3 in December, returned to 56.6 in January and has been ratcheting lower since.

New orders hit their post-recession and post-election high of 67.3 in December 2017. They stayed above 60 until October 2018, fell to 51.3 last December, which was the lowest since August 2016 and rebounded to 58.2 in January. April’s 51.7 was the second lowest score since the election in November 2016.

Reuters

The employment index’s best level came in October 2017 at 59.5, a six year high. Last year’s top was 58.2 in September, prefacing a plunge to 52.3 in February a recovery to 57.5 in March and then 52.4 in April and 53.7 in May.

Reuters

The production index rose 1 point to 51.3 and the price index jumped to 53.2 in May from 50.

Manufacturing optimism had maintained itself throughout last year despite the trade dispute with China and the imposition of competing tariffs. The argument was seen in the context of the vast exchange between the two countries and the importance to the relationship to both sides.

The American complaint in early May that China had reneged on several key points that had already been agreed led US President Trump to raise tariffs on a large portion of Chinese imports from 10% to 25%.

Although there are currently no talks scheduled both parties have recently expressed a willingness to resume negotiations. Senior officials from the US and China will attend preliminary meeting of the G-20 in Japan this month and a possible meeting between Presidents Trump and Xi Jinping at the G-20 summit is possible.

A press story had quoted a mainland government official who claimed that China had not reneged on its negotiating commitments because no final agreement had been formulated and that positions can be changed at at point in talks.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.