Manufacturing growth slows, especially order backlogs, but prices surge

The ISM report looks strong but a dramatic reduction of growth in backlogs flashes a warning signal.

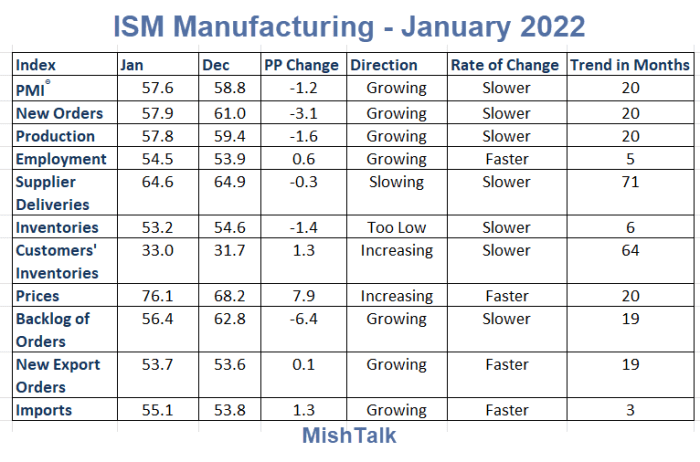

ISM Manufacturing for January 2022, Chart by Mish

The January 2022 Manufacturing ISM® Report by the Institute for Supply Management shows another big jump in prices but mostly weakening numbers.

Diffusion Index

The ISM report is a diffusion index which means direction is more important than quantity. Numbers above 50 indicate growth, number below 50 show contraction.

The numbers come from a survey of manufacturers, and indicate direction, not amount.

For example, two manufacturers increasing employment by a person weighs more than a third manufacturer who lays off 100 people.

Today's numbers show 54.5% of businesses are increasing employment but we do not know by how much, or even if overall employment is rising at all.

Backlog of Orders

The most important takeaway from today's report is the sharp reduction in the growth of backlogs.

Again, this is a diffusion index which makes things difficult to properly assess, but it's a possible indication that manufacturers are catching up with orders or their customers are catching up with whatever inventory build they intend to do.

Reflections on 4th-Quarter GDP

Recall my observation GDP Up 6.9% Is Mostly An Artificially Boosted Illusion

Inventory Adjustments

Change in Private Inventories (CIPI) added a whopping 4.9 percentage points to real GDP in the fourth quarter. Since inventories net to zero over time, the true bottom-line estimate of real GDP was 2.0%.

For the third quarter, CIPI added 2.20 percentage points to real GDP.

Thus, of the reported 2.3% GDP gain for the third quarter, nearly the entire rise was an inventory adjustment.

Retail Sales Unexpectedly Flop in December, Down 1.9 Percent

Holiday shopping was a big flop in 2021, even nonstore retailers were down a whopping 8.7%.

Unexpected Flop

The Bloomberg Econoday consensus was for December retail sales to be flat from November, in a range of -0.6% to +0.7%.

Economists missed the mark by a mile as the Census Data shows sales fell 1.9%.

Adding insult to injury, the Census Department revised November to the downside.

Businesses are stocking up but consumers are failed to show up and inflation is raging. Gee, what can possibly go wrong with this scenario?

With Nearly Everyone Looking the Other Way, It's Time to Discuss Recession

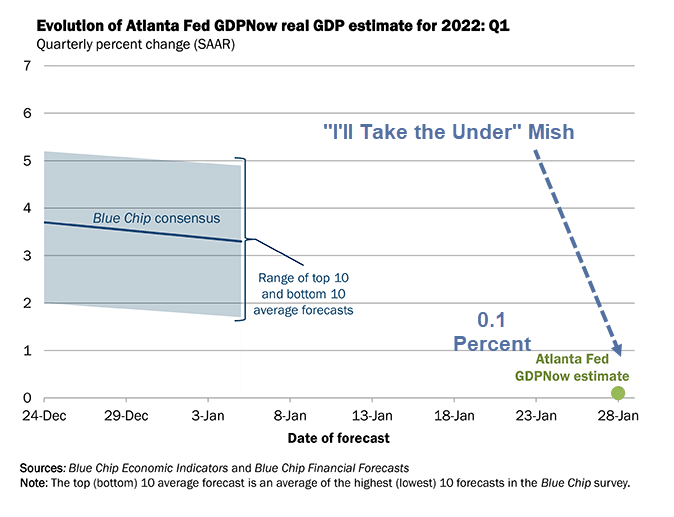

GDPNow Initial Forecast for 2022 Q1, Chart by Atlanta Fed, Chart Comments by Mish

Please reconsider my January 28 post With Nearly Everyone Looking the Other Way, It's Time to Discuss Recession

Finally please note Mortgage Rates Are at the Highest Level Since Before Covid-19 Hit

Housing is about to stumble and it won't stop there. Liquidity is drying up on multiple fronts simultaneously.

The ISM reduction in backlogs and relatively low new export orders put an additional spotlight on pending manufacturing weaknesses.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc