Macro Events & News

FX News Today

10-year Treasury yields are down -0.2 bp at 2.414$, JGB yields fell back 0.2 bp to -0.054% as BoJ Governor Kuroda warned against the fallout from escalating trade tensions between the U.S. and China and the minutes of the last RBA meeting confirmed that Australia’s central bank is laying the ground for a rate cut in coming months.

Stock markets moved mostly higher, with mainland China bourses outperforming and bouncing back from Monday’s lows, although the impact of the measures that cut Huawei off from vital supplies will likely to continue to impact the tech sector not just in China.

USD got a bid -AUD (&NZD sink) on RBA comments that rate cut likely if Employment situations does not improve. (0.6875 & 0.6510) respectively. Powells speech was non-market moving.

EUR back to 1.1150 (s) from 1.1175, JPY -110.15 – r at 110.25 (Questions over Abe’s Sales Tax) , GBP 1.2721 – (12 days down for Cable).

GOLD Pivots around 1275 support ; OIL – back up to 63.50 from yesterday 62.50 low. R at $64.

Charts of the Day

Technician’s Corner

AUDUSD fell back under 0.6900 – 20 period moving average sits at 0.6907, S2 is next support at 0.6866. R1 and the 200-period moving average is at 0.6930-33.

GBPUSD’s low is 1.2707 in what is now the eighth consecutive daily decline and the eleventh down day out of the last twelve trading days. Pivot point comes in at 1.2730, with support at 1.2700.

Main Macro Events Today

Inflation Report Hearings (GBP, GMT N/A) – The BOE Governor and several MPC members testify on inflation and the economic outlook before the Parliament Treasury Committee.

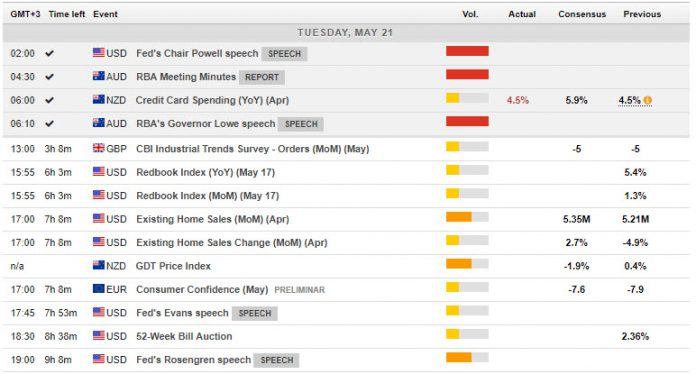

US Existing Home Sales – Expected – 5.38 million, last time 5.35 million.

Support and Resistance levels

Author

With over 25 years experience working for a host of globally recognized organisations in the City of London, Stuart Cowell is a passionate advocate of keeping things simple, doing what is probable and understanding how the news, c