Macro Events & News

FX News Today

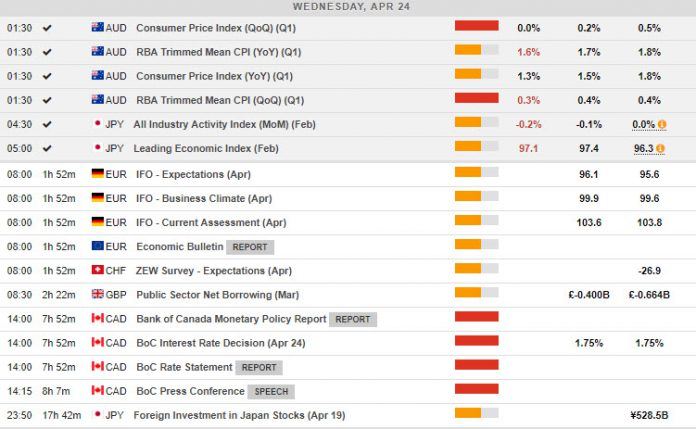

Australia’s bond as well as stock markets rallied after inflation came in lower than anticipated at 0.0% q/q, down from 0.5% in the previous period and versus median expectations of 0.1%.

Markets are convinced that the inflation miss will make a rate cut all but inevitable and 10-year yields plunged 10.5 bp, while the ASX jumped as much as 1.1% to a more than 11 year high, after already outperforming yesterday.

Elsewhere in Asia markets were under pressure, however, despite the strong close on Wall Street, where sentiment was boosted by upbeat earnings reports.

The USA500 and USA100 closed at record highs Tuesday

Twitter stock surges more than 15% on earnings beat, while Coca-Cola share price up 2% as Q1 earnings revenue was $8.02 billion, topping projections of $7.88 billionThe concerns that China may slow the pace of policy easing and stimulus measures continuing to weigh on sentiment.

The WTI oil softer today after surge to 6-mth high at $66.60 yesterday.

Charts of the Day

Technician’s Corner

USOIL softer at 66.00 hurdle after topping at a new nearly six-month high of $66.60. Overall outlook holds to the upsdie as asset is sloping within an uptrend, with small corrections to the downside.

USDJPY has continued to oscillate in a narrow range in the 111.75-112.00. The focus this week will be on fresh signs that corroborate the return-to-growth picture in major global economies. A continuation of this theme would be supportive of currencies that performer with higher beta characteristics, such as the dollar bloc units, while currencies of the low-yielding safe haven type, such as the yen, would be apt to underperform. USDJPY has support at 111.54-111.60, levels which encompasses the prevailing position of the 200-day moving average.

AUDUSD dove to 0.7026, just a breath above 3-year Support. It was driven by Aussie-spcecific losses following sub forecast CPI data out of Australian, which catalysed calls for the RBA to cut interest rates at its next policy review in May. A break of 0.7000 could open the way towards December slip.

Main Macro Events Today

IFO (EUR, GMT 08:00) – Business climate in the largest EU country is expected to have grown marginally to 99.9 compared to 99.6 last month.

Event of the week – BoC Interest Rate Decision (CAD, GMT 14:00) – At the BoC meeting, consensus expectations are that there should be no interest rate change. A sharper and more broadly based slowdown in the domestic economy, alongside a slowing in the global economy that has been more pronounced and widespread than anticipated saw the Bank state “the outlook continues to warrant a policy interest rate that is below its neutral range.”

Support and Resistance

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in