Macro Events & News

FX News Today

Asian indices broadly higher amid fresh hopes on the US-Sino trade front.

BoJ kept policy unchanged as expected, exports seen weighing on outlook.

Trump-Xi summit pushed back to end of April, USTR cited “major issues”.

Xinhua news agency reported that Chinese Vice Premier Liu He had a telephone conversation with US Secretary Mnuchin and US Trade Representative Ligthizer and that further substantive progress on trade talks has been made.

UK lawmakers backed a delay to the Brexit process.

PM May set to ask for a short term extension if her deal gets through by March 20, i.e. before the next EU summit, or a long term delay if not.

European stock futures are moving higher in tandem with US future.

WTI future is trading at USD 58.76 per barrel.

EURUSD softer after posting 9-day high at 1.1341 following soft U.S. PPI

USDJPY lifted to 1-week highs above 111.70; Yen wary of BoJ dovish tone.

Charts of the Day

Technician’s Corner

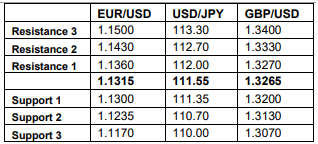

EURUSD found a floor at 1.1310 after rebounding from 1.1290. Remains overall in an uptrend. The same positive bias held intraday as well, with MAs pointing upwards, with RSI sloping above 50.

GBPUSD is traded in a descending triangle. Support is held at 50-period SMA at 1.3225 and Resistance 1.3265. A break of these barrier could suggest the near term direction for Pound.

XAUUSD rebounded from 1297 and broke earlier the 1300 barrier. Upper Bollinger bands are extending higher while the asset regain more than 60% of the losses seen yesterday, turning the negative near term outlook to positive one.

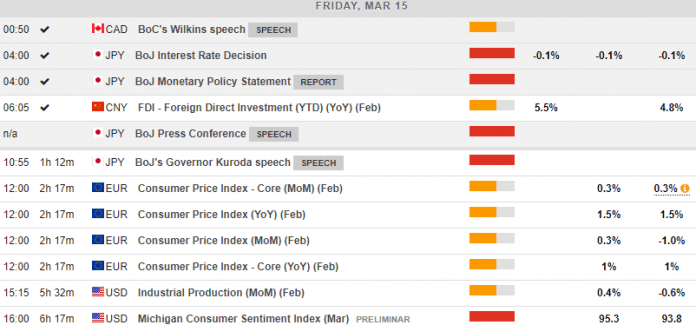

Main Macro Events Today

BoJ Koruda Speech -Due to speak at the B20 Tokyo Summit.

EU Final CPI – The overall Eurozone HICP is anticipated at 1.5% y/y.

Canadian Manufacturing Sales – the Manufacturing shipment values are expected to edge 0.5% higher in January after the 1.3% drop in December.

Michigan sentiment and Industrial data – Industrial production is projected to rise 0.4% in February, after a 0.6% drop in January, while capacity utilization should rise to 78.4% from 78.2% in January. An early March Michigan sentiment reading is expected of 96.0 , up from 93.8 in February, but well below the 14-year high of 101.4 last March.

Support and Resistance

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in