Macro Events & News

FX News Today

10-year Treasury yields are up 0.2 bp at 2.704% and JGB yields fell back -0.8 bp to -0.025% as the rally on stock markets faded.

Wall Street still closed with slight gains, but there wasn’t enough momentum to sustain a further broad move higher in Asia.

Topix and Nikkei closed little changed, the Hang Seng is down -0.26% while CSI 300 and Shanghai Comp are up 0.33% and 0.13%, after Chinese data showed a rebound in exports at the start of the year.

The tech hub of Shenzhen outperformed with a gain of 0.93%, but the ASX also closed with a marginal loss.

US futures as well as European futures are moving higher though, so there is still some life in markets after reports that the U.S. is considering delaying China tariffs for 60 days. President Trump had already told reporters that trade talks are making good progress.

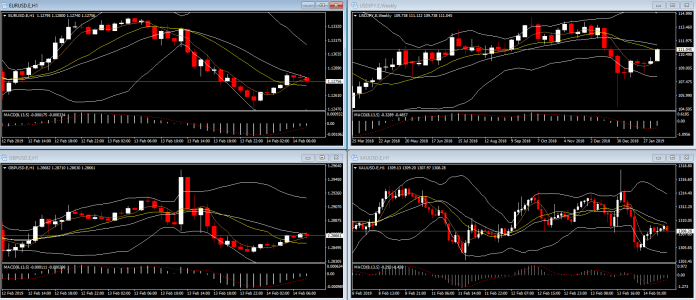

Charts of the Day

Main Macro Events Today

EU GDP – The common currency’s GDP is expected to have grown by 1.2% y/y on the final quarter of the year, the same growth rate recorded in Q3.

US Retail Sales – One of the most important indicators of consumption, Retail sales ex Autos are expected to have grown by 0.1% m/m in December, compared to 0.2% m/m in November.

US PPI Inflation – In accordance to the slowdown picture in the US, PPI inflation is expected to have slowed to 2.5% y/y in January, compared to 2.7% y/y in December.

US Jobless Claims – Continuing Jobless Claims are expected to have increased to 1.74M on the week ending at January 8, compared to 1.736M last week. Initial Jobless Claims are expected to have decreased to 225K compared to 234K on the previous week.

Support and Resistance

Author

With more than 4 years of experience at the Central Bank of Cyprus where he obtained hands-on experience with real-life economics, Dr Nektarios Michail is a supporter of a balanced approach between science and art when it comes to