Macro Events & News

FX News Today

European Fixed Income Outlook: The December 10-year Bund future opened at 161.00, up from a close of 160.90 on Wednesday. 10-year cash yields are down -1.2 bp at 0.336% in opening trade, versus a -4.0 bp decline in Treasury yields, which are now trading at 3.019%. Dovish leaning comments from Fed Chairman Powell boosted bond as well as stock markets, although the rally in equities already started to fizzle out during the Asian session amid growth warnings from the IMF and as Trump revisited the threat of 25% tariffs on imported cars. US stock futures are heading south as are DAX futures, although FTSE 100 futures are moving higher, despite warnings from the government as well as the BoE on the impact of a no-deal Brexit on the economy. Already released Swiss GDP growth unexpectedly contracted -0.2% q/q, highlighting the impact trade tensions are having on export oriented economies. Still to come the busy calendar holds preliminary inflation data from Germany and France as well as German labour market data and Eurozone ESI economic confidence data.

Asian Market Wrap: 10-year Treasury yields dropped -4.6 bp to 3.01%, 10-year JGB yields fell back -1.1 bp to 0.075%, after dovish leaning comments from Fed Chairman Powell boosted speculation that the central bank may halt the rate hike cycle after the widely anticipated hike in December. The remarks underpinned a very strong close on Wall Street, where the Dow Jones jumped 2.5%, but also put pressure on the Dollar, which capped gains on Asian markets. Topix and Nikkei are still up 0.35% and 0.39% respectively, but down from early highs as the Yen strengthened. Hang Seng and Shanghai Comp erased early gains and are down -0.85% and -0.70% respectively as the focus shifts to the upcoming G-20 meeting and the prospects for US-Sino relations as Trump raised the prospect of putting a 25% tariff on imported cars and ordered a review of China’s retaliatory auto tariffs against the U.S. Emerging market equities and developing nation currencies benefited from the softer stance at the Fed, but U.S. stock futures are already heading south again. Oil prices are trading at USD 50.38 per barrel, after topping out at USD 51.04 overnight.

Charts of the Day

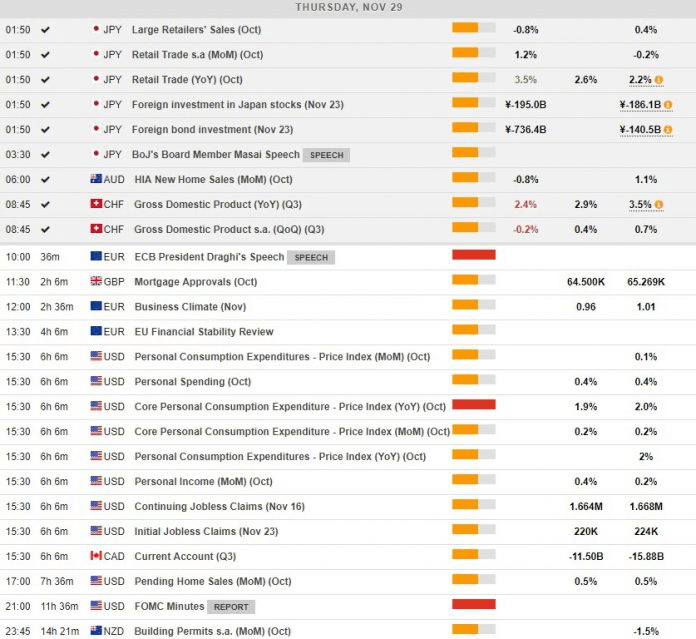

Main Macro Events Today

ECB Draghi Speech – ECB President Mario Draghi is set to speak at the Global Research Forum on International Macroeconomics and Finance in Frankfurt, with much awaited comments after Powell’s dovish remarks yesterday.

EU Business Climate and Financial Stability Review – The Business Climate indicator, published by the European Commission on the basis on monthly surveys, is expected to have deteriorated to 0.96 compared to 1.01 last month.

PCE Inflation, Personal Income and Jobless Claims – October’s PCE inflation is expected to come out at 1.9%, slightly lower than the 2% September figure, again close to the Fed’s 2% inflation target. Personal Income is expected to have increased by 0.4%, compared to 0.2% last month, while jobless claims, both continuing and initial, are expected to decline compared to last month.

Canadian Current Account – Q3 data on the Current Account are expected to have been better than last quarter, registering an almost CAD4.5bln improvement.

FOMC Minutes – Offering an insight into the policymakers’ mind, the FOMC minutes should present more information regarding its members’ positions regarding future rate hikes, especially after Powell’s dovish speech yesterday.

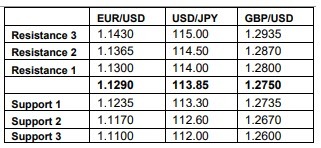

Support and Resistance

Author

With more than 4 years of experience at the Central Bank of Cyprus where he obtained hands-on experience with real-life economics, Dr Nektarios Michail is a supporter of a balanced approach between science and art when it comes to