Macro Events & News

FX News Today

European Fixed Income Outlook: The December 10-year Bund future opened at 158.89, down from a close of 158.16 yesterday. Hawkish leaning Fed minutes put pressure on bond as well as stock markets and the 10-year cash yield is trading above 0.46% after closing at 0.459% yesterday. UK100 futures are moving higher, while US futures are heading south following a weak session in Asia. Confirmation that EU-27 leaders didn’t see sufficient progress in Brexit talks to schedule a November summit to sign off a deal put fresh pressure on Sterling. Elsewhere in Europe though risk aversion is likely to hit stock markets, especially as the US singled out Germany’s trade surplus with the US as a course for “significant concern”. Brexit jitters aside Italy’s fiscal problems also remain in focus. The data calendar holds Eurozone Balance of Payments data, as well as UK public finance data.

Asian Market Wrap: 10-year Treasury yields gained a further 0.2 bp overnight, and trading at 0.321%, after jumping in the wake of hawkish leading Fed minutes yesterday. 10-year JGB yields rose 0.6 bp to 0.143%. Asian bourses meanwhile are a sea of red with Chinese markets under fresh pressure amid fresh focus on troubled companies that used share holdings as collateral for loans. Topix and Nikkei are down 0.35% and -0.68% respectively. The Hang limited losses to -0.18% after returning from yesterday’s holiday, but mainland China indices slumped 1-2%. Risk off sentiment is back as rising yields and reduced central bank support not just in the U.S. is back in focus. U.S. futures are also heading south. Oil prices are edging higher, after dropping on a big stock build Wednesday.

Charts of the Day

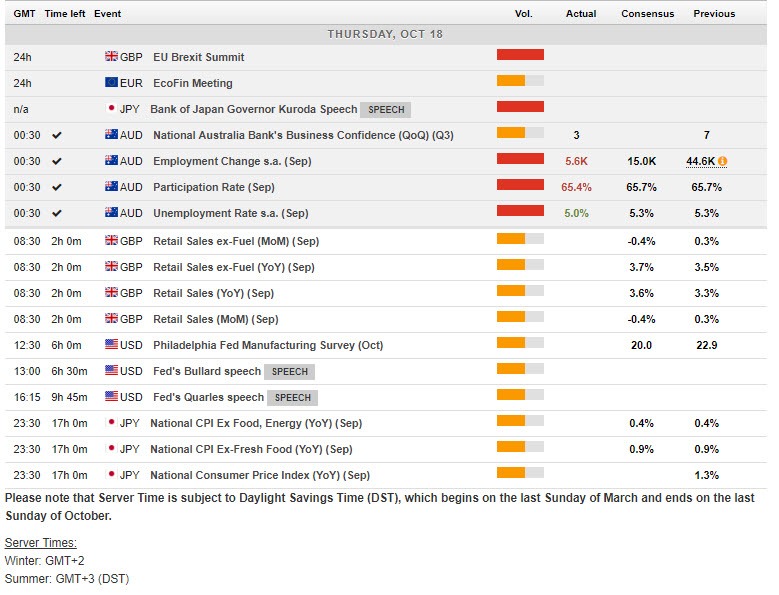

Main Macro Events Today

UK Retail Sales – Expectations – The September retail sales expected to reach 0.3% m/m contraction (median -0.4%) after 0.3% growth in the month prior, with the y/y rate seen lifting to 3.7% y/y from 3.3%.

Philly Fed Manufacturing Index – Expectations – It is expected to ease to 21.0 from 22.9. This compares to the already released Empire State measure which posted a climb to 21.1 from 19.0 in September. More broadly, we expect to see a slight easing in producer sentiment in October with the ISM-adjusted average of all measures easing to 58 from 59 in both September and August.

US Unemployment Claims- Expectations – Claims data should post a 6k increase to 220k from 214k last week and 207k in the week prior to that.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in