Macro Events & News

FX News Today

Asian Market Wrap: 10-year Treasury and JGB yields gained 0.2 bp each and are trading at 3.165% and 0142% respectively, but despite broad gains on Asian stock markets, Treasuries are down from earlier highs and most government bonds in Asia managed to move higher. Japanese bourses continued to bounce in the wake of the tech stock recovery in the US yesterday and with earnings from the likes of Goldman Sachs, and Netflix adding support. Topix and Nikkei are up 1.35% and 1.05%. The ASX also managed a strong 1.12% gain, but Chinese bourses are underperforming. Hong Kong was closed today. US stock futures are actually posting slight losses, highlighting not only that stocks still have a way to go before they have recouped last week’s losses, but also that sentiment is still fragile as investors struggle with the sharp rise in yields. Markets are now looking ahead to today’s release of the minutes from the last Fed meeting. The local calendar was quiet and Oil prices are trading around the USD 72 per barrel mark after the unexpected drop in American crude stockpiles and as investors keep a nervous eye on simmering tensions between the US and Saudi Arabia over the missing journalist. For now Trump seems to be giving Saudia Arabia the benefit of the doubt.

FX Action: USDJPY posted a 3-session high at 112.42 before settling around 112.14 . AUDJPY posted a 1-week high before ebbing back, while the likes of EURJPY and GBPJPY have remained below their respective highs from yesterday, although also running higher during the Tokyo AM session. The weakness in the Yen has been concomitant with an improvement in risk appetite, with Wall Street closing solidly higher following a tech-led rally founded on encouraging earnings reports and stock markets in Asian, outside of China, following suit. The Nikkei 225 is showing a 1.3% gain, while China’s SSE index is down by 0.7% on nagging concerns about the impact of the US-China trade war. USDJPY has been in a choppy range rooted on the 112.00 level for nearly a week now, consolidating after dropping back from levels near 114.50 over the week before. Fundamentals (yield differentials and the associated contrast between Fed and BoJ policy paths) remain supportive, but the spectre of risk aversion has been an offsetting bearish force.

Charts of the Day

Main Macro Events Today

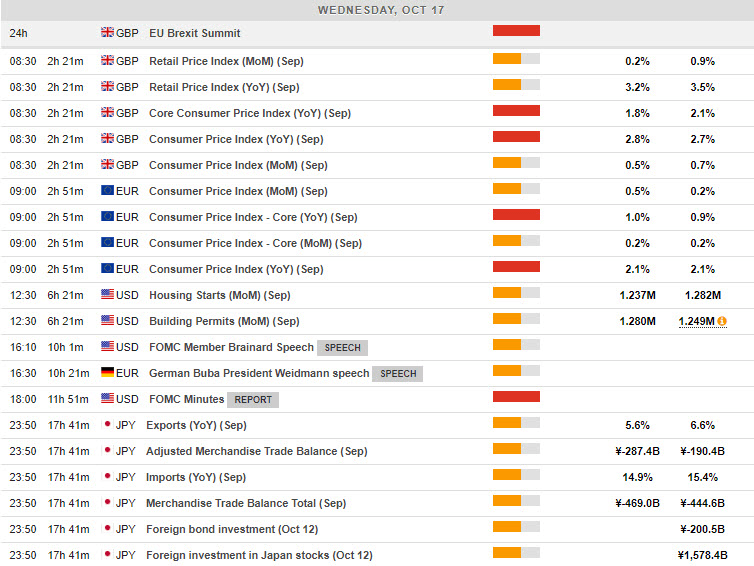

UK Sep CPI – Expectations – The UK inflation is anticipated headline CPI to dip to 2.6% y/y in September from 2.7% in the month prior, with the core CPI figure seen ebbing to a 2.0% y/y rate from 2.1% in August.

EU 27-Summit on Brexit

Eurozone Sept. HICP – Expectations –The final reading of September Eurozone HICP is unlikely to hold any surprise and confirm the headline rate at 2.1% y/y, above the ECB’s 2% limit for price stability, but mainly due to higher energy and food price inflation.

US Sept. Housing start, Permits & EIA inventories – Expectations – They are forecast to drop 2.5% to 1.250 mln, while permits should rise 2.5% to 1.280 mln. Also slated are MBA mortgage stats. All of the September housing data are at risk for a hit from hurricane Florence. EIA energy inventory data is on tap too.

FOMC Meeting Minutes

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in