Macro Events & News

FX News Today

FX Action: USDJPY has lifted to the 112.30-40 area after posting a 25-day low at 111.83 during the late New York PM session yesterday. The low was followed by broad Dollar declines in the wake of the softer than expected US CPI data yesterday, which has taken the edge out of Fed tightening expectations. Gains in USDJPY in Tokyo, however, have reflected broader Yen weakness, which has seen safe-haven premium unwind as stocks in Asia stabilize, and with S&P 500 futures managing gains of more than 1.2%, after the cash index closed on Wall Street with a 2.1% decline. EURJPY and most other Yen crosses have also lifted. In news today, a 5.3 earthquake hit Japan’s Kanto region, which is reportedly manageable for Japan. No tsunami warning has been issued. A senior official from the IMF, which today started its annual meeting in Bali, said that it was “too early” for Japan to talk about normalizing monetary policy while encouraging Tokyo to make structural reforms to accompany the stimulus.

Asian Market Wrap: 10-year Treasury yields moved up from yesterday’s lows and gained 2.9 bp to reach 3.178%. 10-year JGB yields are unchanged at 0.136%, as stock markets bounced back in Asia and the MSCI Asia Pacific Index moved up from the lowest level since May 2017, led by bourses in Hong Kong and South Korea. As of 5:24GMT Topix and Nikkei were still down -0.35% and -0.34% respectively, but the Hang Seng bounced 1.67%, the CSI 300 was up 1.30%. Shanghai Comp and Shenzen Comp still declined at the start of the session, but are now at 0.53% and -0.06% respectively after a better than expected trade surplus. Kospi and Kosdaq are up 1.98% and 3.06% and the ASX gained 0.20%. Sentiment remains fragile, but US stock futures are posting gains of more than 1% so it seems markets are closing a very volatile week on a less pessimistic note. With central banks on course to end stimulus and Fed Chairman Powell stressing last week that the central bank is a “long way” from neutral rates concerns remain that the Fed may tighten too much and the IMF warning about the impact of a tightening of financing conditions markets will be struggling to find a new equilibrium, with overreactions likely also a result of heightened uncertainties. This leaves a wide range of possible outcomes for the world economy.

Charts of the Day

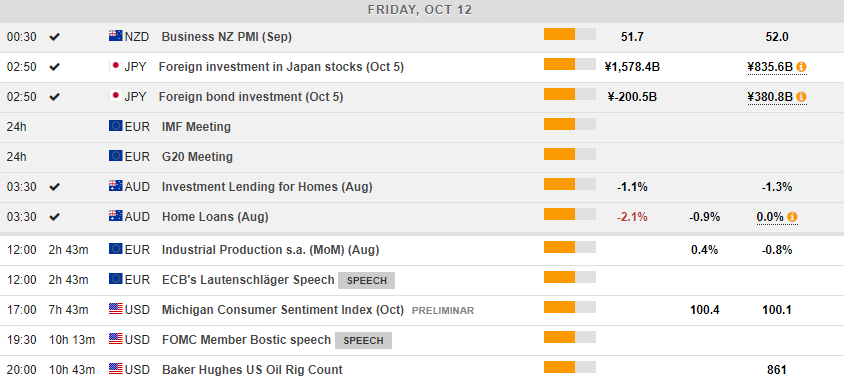

Main Macro Events Today

Euro Area Industrial Production – Expectations – Industrial Production is expected to have increased by 0.4% m/m in August, compared to a reduction of 0.8% in July.

US Michigan Consumer Sentiment Index – Expectations – The Michigan Consumer Sentiment Index is expected to pose slight gains in October, moving to 100.4, compared to 100.1 in September.

Support and Resistance Levels

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in