Macro Events & News

FX News Today

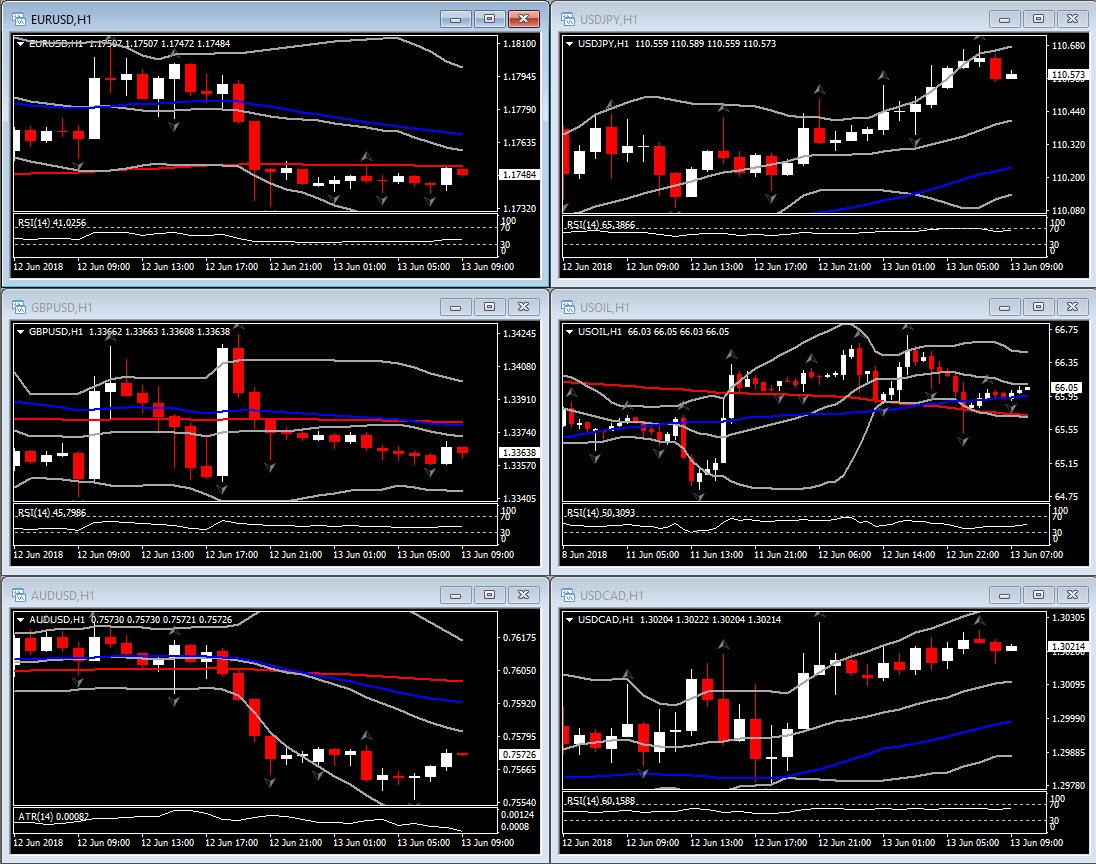

Asian Market Wrap: Stock markets are mostly in the red as a lacklustre session in Asia draws to a close. Investors left G7 and North Korea summits behind and focused on major central bank decisions this week. Haven assets including the yen weakened amid hopes of diminishing geopolitical risks and a weaker yen helped Nikkei and Topix to outperform and post gains of 0.44% and 0.53% respectively. U.S. Treasury yields moved up from early lows and are now up 0.7 bp at 2.970%, while 10-year 10year JGB yields corrected early gains and are down -0.2 bp at 0.041%. The Fed kicks off the round of CB decision with a 25 bp rate hike pretty much a done deal, leaving the focus on the rate outlook and similar to the ECB meeting tomorrow, there could actually be good news for markets if the guidance is less hawkish than feared. U.S. stock futures at least are moving higher for now.

FX Update: Most currencies have been directionally dormant so far today, though US-JPY managed to claw out a fresh three-week high at 110.68. Yen crosses also remained underpinned, though most, such as EURJPY and AUDJPY, for instance, remained below recent highs. Global stock markets have lost upside traction, with risk appetite turning somewhat neutral as market participants anticipate “live” Fed and ECB meetings this week, with the former set, later today, to hike the Fed funds rate by 25 bp and the latter to announce, tomorrow, an end of QE. Attention will be on the respective guidance the central banks give. The Japanese currency has been under-performing as it loses some of its safe haven premium following all the bonhomie, feel good glow of the Trump-Kim summit.

Charts of the Day

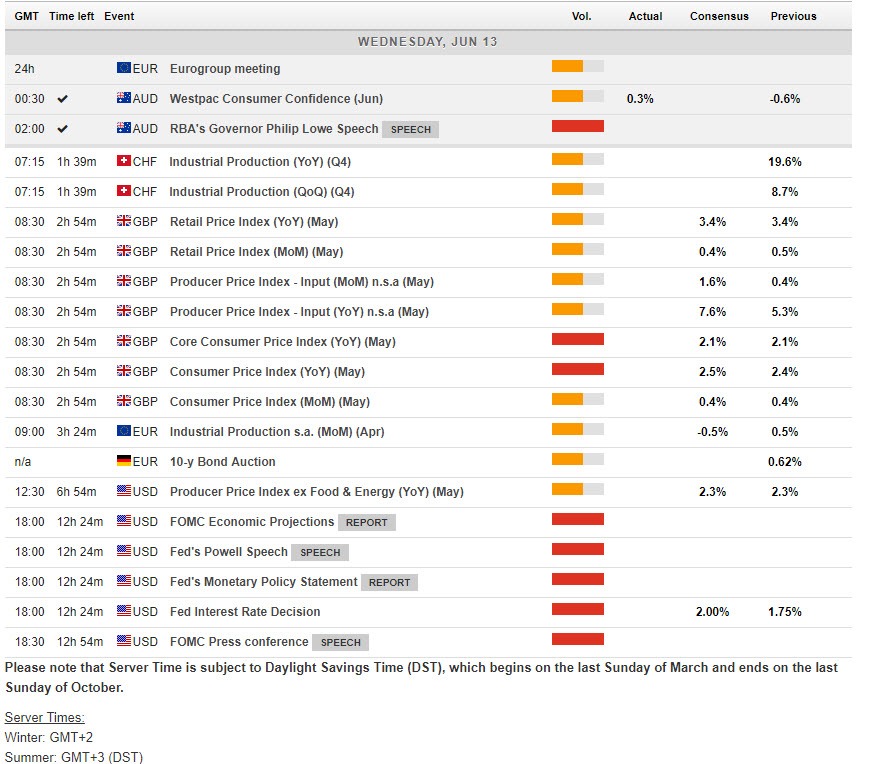

Main Macro Events Today

UK CPI and Core CPI – Expectations – to dip to a new cycle low of 2.4% y/y from 2.5% y/y in the month prior, and see core CPI to also remain unchanged, at 2.1% y/y.

US PPI – Expectations – a 0.2% increase in headline PPI. The gain should be reflect a 0.3% increase in services prices and a more benign 0.1% rise in goods prices (related to a 0.8% increase in PPI gasoline).

US Crude Oil Inventories – Expectations – crude supplies expected to decline by 1.4M barrels.

FOMC Statement & Press Conference – Expectations – A 25 bp rate hike, a second for this year, is a fait accompli. So, what will be market moving will be the quarterly forecasts (SEP), including the dot-plot, a potential tweak in IOER, and any surprises from Powell. The key risk for the markets is with the dot plot, and whether the median dot remains at three tightenings this year, or is bumped up to four. With the markets concerned over an aggressive FOMC, maintaining the dots at three would be bond friendly.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in