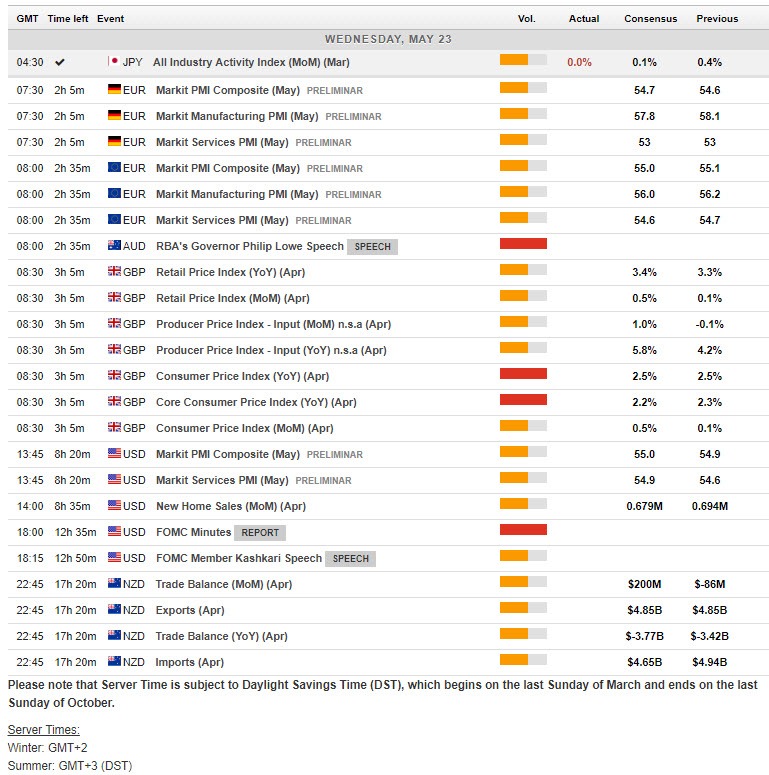

Macro Events & News

FX News Today

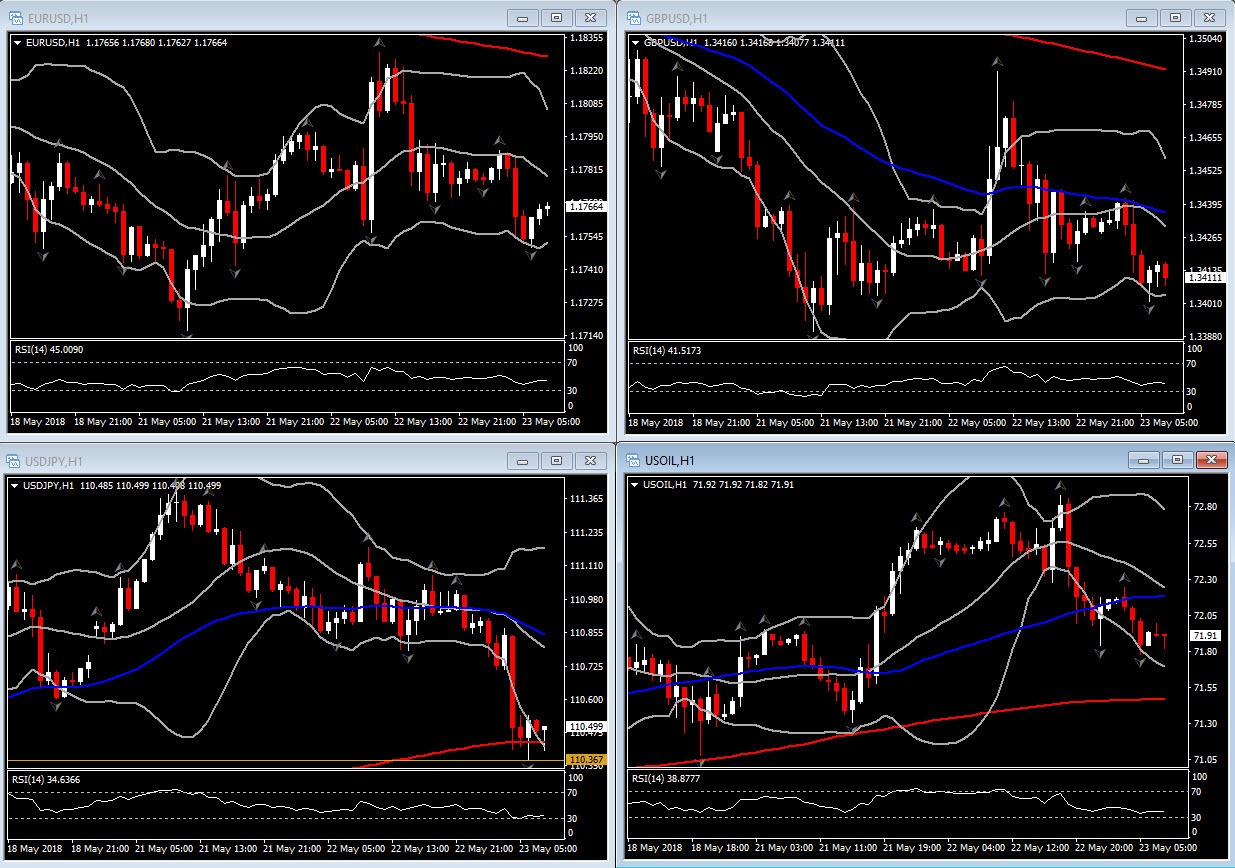

Asian Market Wrap: Long yields declined as risk aversion picked up and stock market retreated in Asia. The 10-year Treasury yield is down -0.9 bp at 3.050%, the 10-year JGB down 0.4 bp at 0.037%. Stock markets headed south, with Japanese markets underperforming as the yen advanced and the focus returned global risks including the U.S.-North Korea summit and Turkey financial market stability. Nikkei and Topix are down -0.64% and -1.14% respectively. The Hang Seng lost -1.02%, the CSI 300 is down -0.84%. U.S. futures are also heading south and oil prices pulled back from highs over USD 72 per barrel and it is trading at USD 71.92. European stock futures are declining in tandem with U.S. futures after a largely negative session for equities in Asia overnight. The good news for the Eurozone is that peripherals have so far not been hit and the Italian 10-year yield is down -2.4 bp, the Spanish down -1.5 bp in early trade. The calendar has Eurozone PMI readings, as well as U.K. inflation data, a German Schatz auction and the U.K. CBI retailing survey.

FX Action: The yen outperformed as risk aversion flared up in global markets, while the dollar, outside the case of USDJPY, traded mostly firmer, gaining ground on the euro, sterling and dollar bloc currencies, for instance. EURUSD settled back in the mid 1.1700s after yesterday’s recovery gains stalled above 1.1800. EURJPY dropped sharply, to an eight-day low at 129.70, while USDJPY posted a four-session low of 110.37 in Tokyo, extending the correction from Monday’s four-month high at 111.39. A risk-off sentient, supportive of the yen in accordance with the typical correlative pattern, came amid a cocktail of geopolitical concerns. In the mix was U.S. President Trump saying that that there was a “very substantial chance” of the North Korean summit being delayed. The recent dive in the Turkish lira also mutated into a full nosedive in thin market conditions just ahead of the Tokyo session, posting fresh record lows. Concerns about excessive dictatorial control of Turkey’s economic policies have been negatively impacting the lira. In data, Japan’s March all industry activity index undershoot expectations at 0.0% m/m. The median had been for 0.1% m/m growth. Australian construction data also missed expectations.

Charts of the Day

Main Macro Events Today

Eurozone PMIs – Expectations – Central bankers will watch this month’s round of confidence data with special interest and hopes that data will show signs that growth is recovering in the second quarter, after the slowdown in Q1 that was impacted by special factors. An effective stabilization is expected to be seen in Eurozone PMI readings for May and an improvement in the manufacturing reading to 56.4 from 56.2. The services reading meanwhile seen falling back to 54.5 from 54.7

RBA Gov Lowe Speech

UK CPI, PPI & Retail Index – Expectations – CPI at 2.5% y/y and core at 2.2% y/y, which would match the prior month’s figure, which itself had undershot both the market and BoE expectation. The PPI is expected at 1% in April from -0.1% seen last month, while Retail Price Index expected at 0.5% in April from 0.1% in March.

US Prel. PMIs – Expectations – Composite PMI for May expected at 55.0 from 54.9, while Services expected at 54.9 from 54.6

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in