Macro Eevents & News

FX News Today

Asian Market Wrap: Rising Treasury yields and geopolitical risks are keeping pressure on stock markets. The 10-year yield fell slightly from yesterday’s highs, but is already backing up again and continued to hold above the 3% mark throughout. 10-year JGB yields are up 0.4 bp at 0.048%, despite bond friendly data showing that the economy contracted -0.6% q/q in Q1. Australia and New Zealand underperformed again, with 10-year yields rising move then 5 bp. After the weaker close in the U.S. yesterday that saw Asian stock markets struggling. Nikkei and Topix are down -0.20% and -0.35% respectively. The Hang Seng stabilised after yesterday’s sell off and is up 0.12%, the CSI currently down -0.09%. The WTI future is trading at USD 71.18 per barrel, slightly down on the day. In europe, German HICP may have been confirmed at just 1.4% y/y, the Eurozone number is likely to come in at just 1.2% y/y, but underlying inflation is slowly picking up and ECB officials speaking today are expected to confirm that the ECB remains on course to phase out QE by the end of the year. Intra-eurozone safe haven flows and a sell off in Italian bonds is underpinning Bunds, as populists edge closer to a coalition agreement and prepare to take power. The calendar also has a Bund sale.

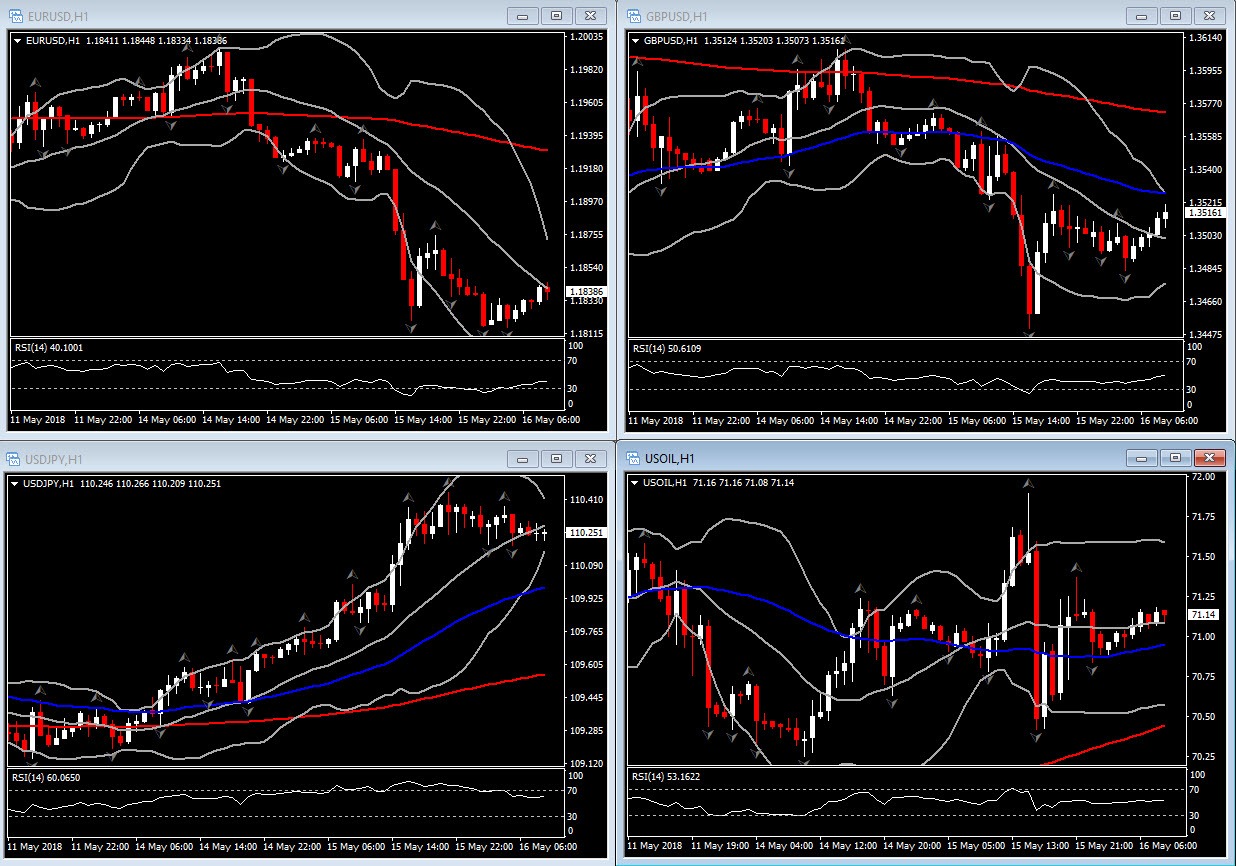

FX Action: USDJPY has settled in the lower 110.0s after posting a 13-week high at 110.45 during the New York PM session yesterday. The new high was largely a reflection of broad dollar buying, which has been concomitant with an ongoing spike in U.S. yields, with the 10-year T-note yield ascending to seven-year high over 3.03%. Strong data out of the U.S. has also been the mix, including yesterday’s retail sales and Empire State manufacturing releases, while today’s preliminary Q1 GDP report out of Japan disappointed, at -0.6% q/q, with Q4 data revised to 0.6% q/q growth from 1.6% q/q growth. The Japanese data follows a Reuters survey finding that almost half of respondents expecting the BoJ to maintain ultra-accommodative monetary policy until 2020, which starkly contrasts Fed policy direction. Support is at 110.01-03, which encompasses former range highs.

Charts of the Day

Main Macro Events Today

-

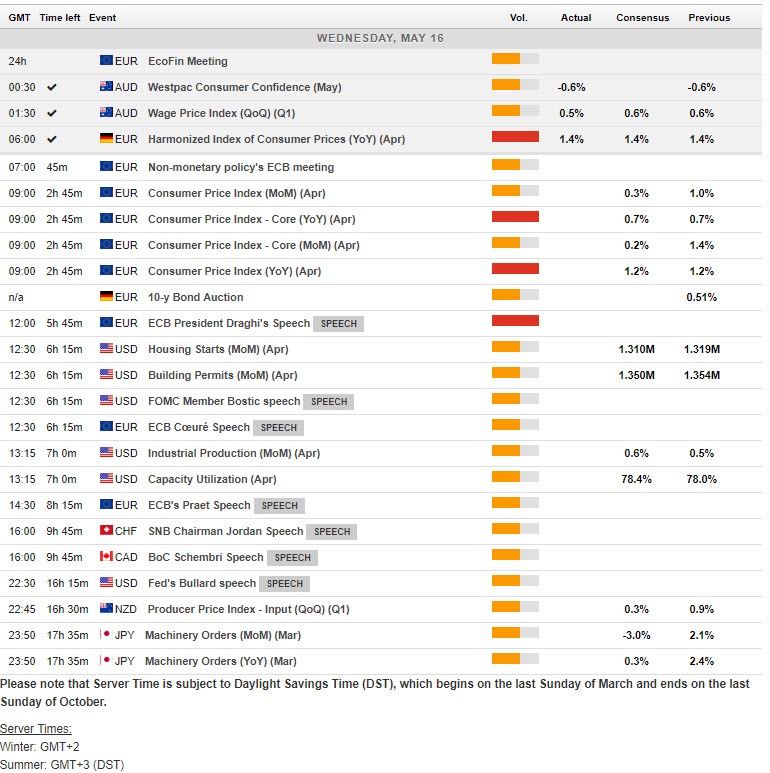

Eurozone Final CPI and Core – Expectations – Inflation expected to be confirmed at 1.2% y/y. Core inflation fell back to just 0.7% y/y in April, but that was impacted by base effects with services price inflation falling back earlier than last year from the Easter spike.

-

ECB President Draghi Speaks

-

US Building Permits, Housing Starts and Industrial Production – Expectations – April housing starts expected to fall 2.2% to a still-strong 1.290 mln in April, following a 1.319 mln pace in March. Building permits are expected to be 1.330 mln, slowing from 1.379 mln in the prior month. Also on tap is industrial production estimated to rise 0.5% in April, following the same gain in March, while capacity use tightens to 78.4% from 78.0%.

-

Canadian Manufacturing Sales – Expectations – projected to gain 2.0% in March after the 1.9% gain in February.

-

Crude Oil Inventories

Support & Resistance Levels

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in