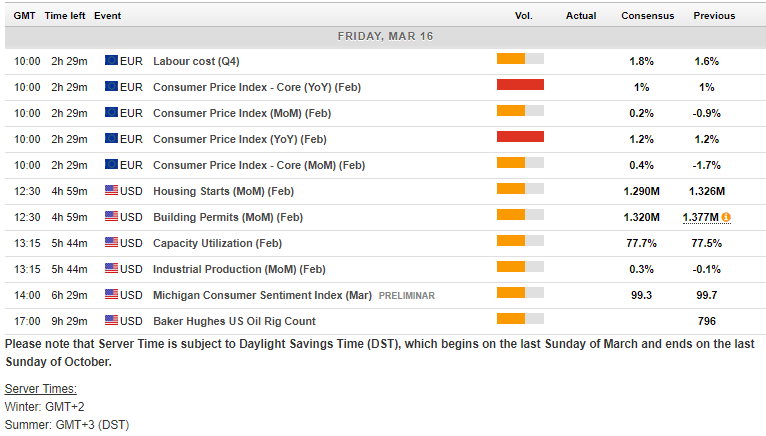

Macro Events & News

FX News Today

European Fixed Income Outlook: The Eurex trading system is experiencing serious issues according to their website and quotes are missing, but French 10-year yields are down -0.4 bp at 0.814%, French and Spanish stock futures are down, in tandem with UK100 futures after a weak session in Asia. Risk appetite has taken another hit as investors eye wearily the succession of personnel changes in Washington and Trump’s tariff plans, with fears of a global trade war intensifying. Geopolitics will likely to continue to trump data today with only final Eurozone inflation data of note in the European calendar.

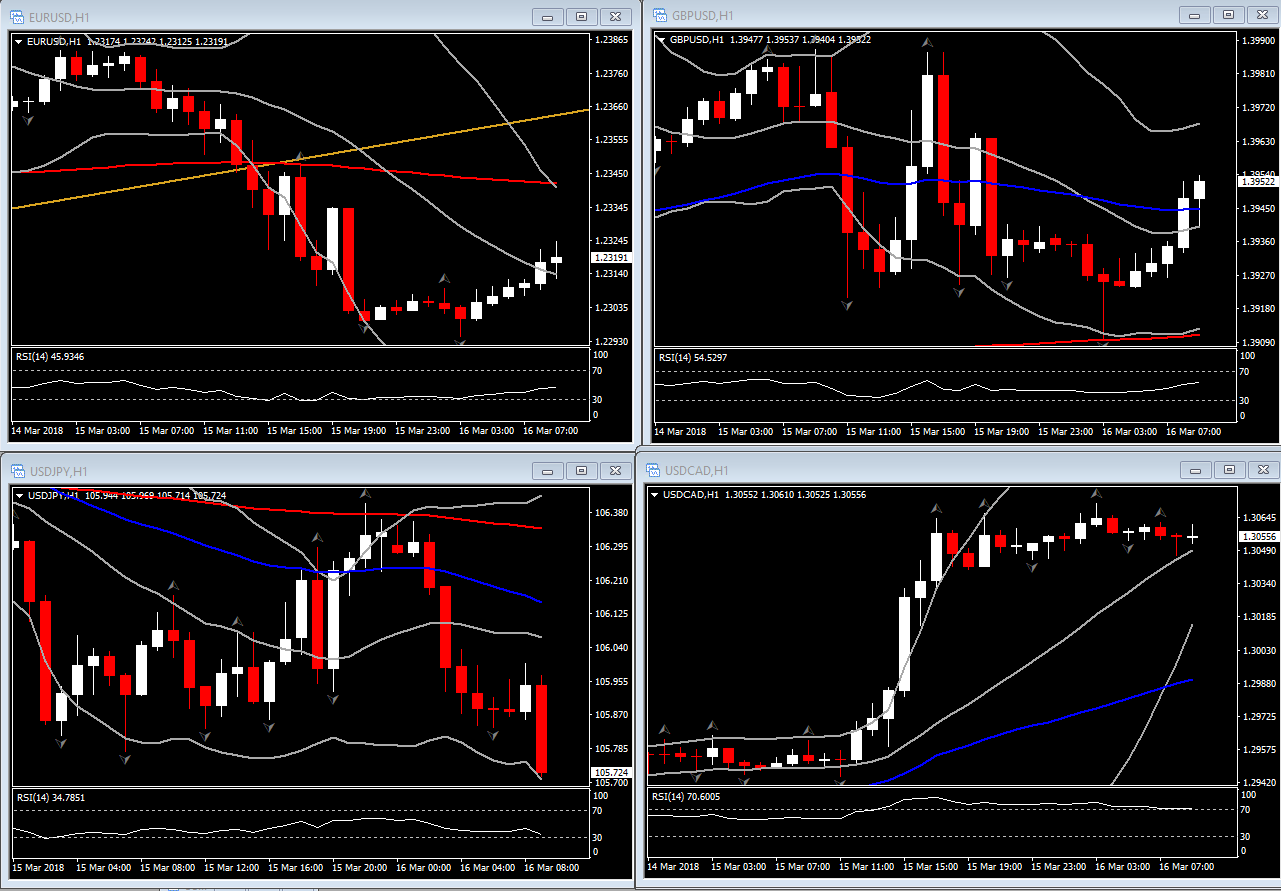

FX Update: The yen has maintained a firming bias amid a mixture of geopolitical news and fresh drama at the White House in the U.S.. USDJPY dipped back under 106.00, while EURJPY and other yen cross have also been trading with a heavy tone. News that Trump has removed his national security advisor, H.R. McMaster has been a worry for some on the view that it might mean Trump will become more hawkish on foreign policy. Some market narratives also pin some of the yen’s gains on news that U.S. special council Mueller has subpoenaed the Trump Organisation for business, some of which are related to Russia. This backdrop has fed a mixed path in global equity markets. Investors are additionally trying to fathom the risk of a Trumpian trade war, how extensive it might and what consequences it might have on global growth. The joint response to Russia by key NATO allies following the attempted hit on an ex Russian double agent is also in the mix. The greater risks is seen for USDJPY declining to 100.00 than climbing to 110.00. Elsewhere, EURUSD recouped above 1.2300 after dipping yesterday to a four-day low at 1.2295. AUDUSD hit a 10-day low at 0.7770 before recouping to 0.7800

Charts of the Day

Main Macro Events Today

EU Labour cost

EU CPI – February HICP inflation is expected to be confirmed at just 1.2% y/y down from 1.3% y/y in January. The breakdown is likely to confirm that the dip in the headline rate was mainly due to base effects from energy and in particular food prices and that core inflation actually held steady. Even the doves at the council are now more confident that underlying inflation is picking up. Indeed, across Europe central banks are turning the focus away from headline inflation to closing output gaps, and if uncertainty about global developments prevents companies from investing into expanding production capacity the ECB will remain on course to take out stimulus even if growth slows down.

US Industian Production, Housing Starts & Consumer Sentiment – The back end of the week winds down with February housing starts forecast to shrink 5% to a 1.29 mln pace from 1.326 mln in January. Industrial production should rise 0.3% in February from -0.1%, while capacity use increases to 77.6% from 77.5%. Preliminary Michigan sentiment may top 99.5 for March from 99.7 previously.

Support and Resistance levels

There's more! Access all our latest analyses and other great content by subscribing to the HotForex Youtube channel. You can also talk to our experts live by registering for one of our free webinars!

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in