Macro Events & News

FX News

European Outlook: Asian stock markets are narrowly mixed and fluctuating at high levels, as trading volumes are low and investors await the Fed decision The MSCI Asia Pacific index has gained around 22% this year, despite escalating tensions with North Korea. FTSE 100 futures are slightly higher, while U.S. futures are in the red, ahead of the Fed, which is widely expected to announce the start of the balance sheet unwind, or QT (quantitative tightening), while leaving its rate posture unchanged. The BoJ will announce its decision tomorrow, and central banks and geopolitics remain driving factor for markets. Reports that there is still no broad majority at the ECB for a commitment to an end date for QE saw yields correcting again in the Eurozone yesterday, while the BoE’s flagging of the need for a rate hike in coming months has kept Gilt yields underpinned. Today’ calendar includes U.K. retail sales, but is unlikely to take the focus away from the Fed.

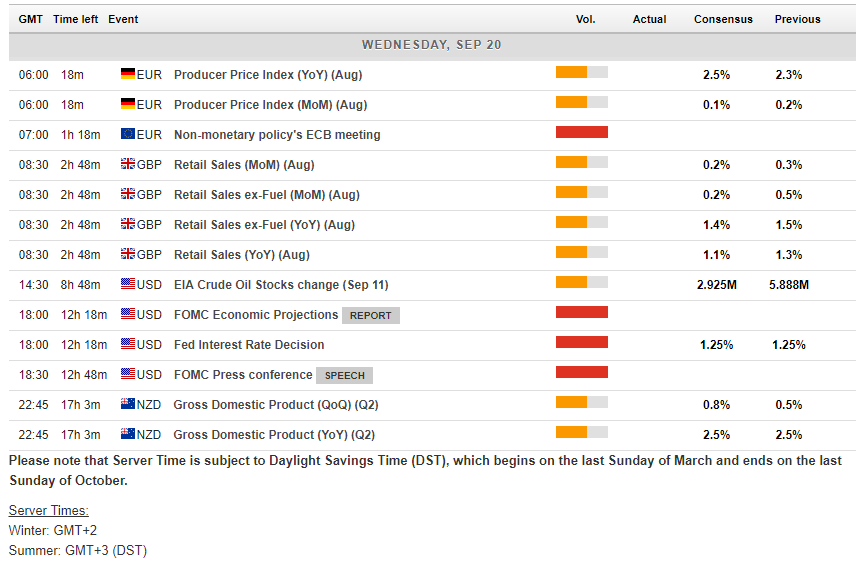

German producer price inflation higher than expected. The annual rate rose to 2.6% y/y in August, from 2.2% y/y in the previous month. A renewed uptick in energy prices was the main factor and energy prices rose 0.4% m/m, fuel prices 0.9% m/m and annual rates rose to 2.7 %y/y and 3.9% y/y respectively. Annual food price inflation fell back slightly, but at 5.3% y/y remains very higher and PPI excluding energy rose to 2.6% y/y from 2.5% y/y. Overall PPI remains below the highs seen earlier in the year, but seems to have bottomed out and the data will back the arguments of the hawks at the ECB, who are fighting for the end of additional asset purchases

U.S. reports: revealed upside surprises for both housing starts and trade prices in August, alongside a wider than expected Q2 current account deficit. For starts, we saw August declines of 0.8% for starts and a big 10.2% for completions, but we also saw a 5.7% pop for permits, a strong trajectory for starts under construction, and upward starts revisions that left a solid Q3 path. For trade prices, we saw big 0.6% August headline import and export price increases led by oil imports and nonagricultural exports with a likely Harvey-boost, before an assumed September lift from Irma. The U.S. current account gap widened to $123.1 bln from $113.5 (was $116.8) bln in Q1 thanks to a surge in the deficit on secondary income.

Canada’s manufacturing drop yesterday is suggestive of tame July GDP growth, at best. Factory shipment volumes fell 1.4% in June (values dropped 2.6%). We have penciled in a 0.1% rise for July GDP estimate, which would follow the 0.3% gain in June. A 0.5% decline in wholesale shipment volumes is projected, while retail sales volumes are seen improving 0.3%. Housing starts grew 4.5% to a 222.0k pace in July from 212.5k in June. Hence, the contribution from construction production should be positive. The outlook for mining, oil and gas production is to the downside. Energy export values fell 3.7% m/m in July after plummeting 11.3% m/m in June. However, the manufacturing report’s petro and coal shipments measure did edge up 0.6% in value after the hefty 7.0% drop in June. A 0.1% rise in July GDP would leave the measures on track for a 2.5% pace in Q3 (q/q, saar) which we expect for the separate quarterly measures. The BoC’s base-case estimates projected a slowing in GDP growth during the second half of this year.

Main Macro Events Today

UK Retail Sales – August retail sales data are due today, where expected a modest 0.2% m/m lift.

FOMC Rate Decision and Conference – FOMC began its 2-day meeting and is widely expected to announce the start of the balance sheet unwind, or QT (quantitative tightening), while leaving its rate posture unchanged. Remember this is a quarterly meeting that includes the release of economic/price forecasts (SEP – Summary of Economic Projections) and a Yellen press conference. Of importance to the rate outlook is the dot-plot and the nuances in the Fed chair’s remarks. The Committee was still expecting a total of three rate hikes this year at the June 13, 14 meeting, and that’s expected to be the case this time too, keeping the door open for a tightening at the December 12, 13 meeting. It is also expected that the FOMC will maintain the consensus view of three hikes in 2018. While the Fed believes there should be little market reaction to the gradual and well telegraphed unwinding of the balance sheet, it should be “like watching paint dry,” said Yellen in June, officials may be too complacent in their overall assessment on the market responses to policy actions.

US Existing Home Sales – Existing home sales for August should bounce 0.7% to a 5.47 mln unit pace, after falling 1.3% in July to 5.44 mln. Sales have fallen in 4 of the 7 months to date, thanks in large part to lack of inventory.

NZD GDP – The Q2 GDP, expected to grow 0.9% after the 0.5% gain in Q1 (q/q, sa).

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in