Macro Events & News

FX News

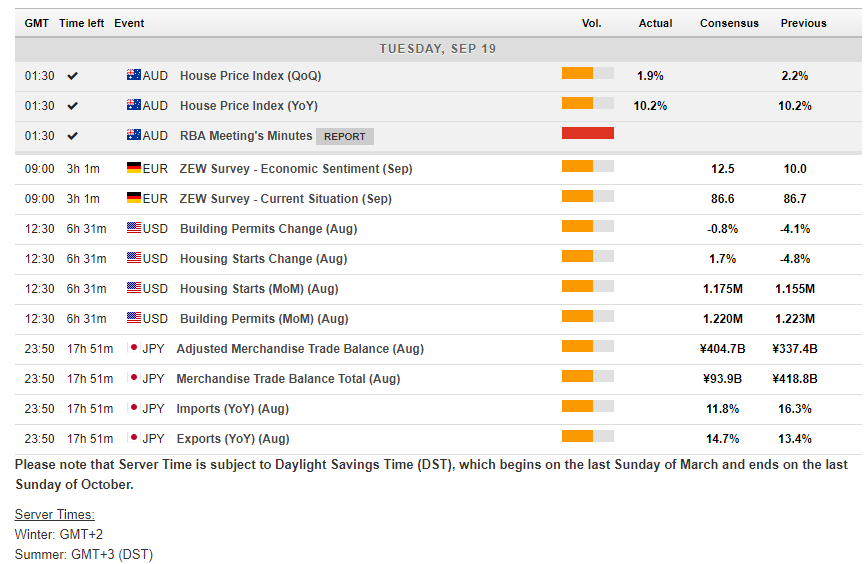

European Outlook: Asian stock markets traded mixed overnight. Japanese markets got a boost by speculation of a snap election, after Abe confirmed reports that he is considering a vote ahead of schedule. Catch up trade after yesterday’s holiday also underpinned a nearly 2% rise in the Nikkei. Elsewhere markets are marginally in the red as markets turn cautious ahead of tomorrow’s Fed announcement. U.K. and U.S. stock futures are also little changed. returned from yesterday’s holiday. The calendar gets more interesting today with the release of German ZEW investor confidence, which we expect to show a slight improvement in the expectations reading to 12.0 from 10.0 in the previous month.

BoE Governor Carney walked back hawkish guidance, saying that “any prospective increases in Bank Rate would be expected to be at a gradual pace and to a limited extent, and be consistent with monetary policy continuing to provide substantial support to the economy.” He also stressed that there “remain considerable risks to the UK outlook, which include the response of households, businesses, and financial markets to developments related to the process of EU withdrawal.” More specifically on Brexit, Carney argued that the “de-integration effects” of Brexit can be expected to be “inflationary.” Carney is evidently displeased with the markets reaction to the BoE’s statement last week, where markets seemed to run with the hawkish soundbites while ignoring the dovish soundbites. The pound, on the ebb after the outsized gains of last Thursday and Friday, declined further as markets responded to Carney’s remarks. Prospects for a “dovish tightening” should keep a lid on the pound’s upside potential.

BOC Gov Council Member Lane held out a gradualist fig leaf to the market, or at least that is how his speech and comments were interpreted by GoCs and the loonie, as yields dropped and USD-CAD jumped to two-week high. The Deputy Governor, in a Q&A with the audience following his speech, said the BoC will take the Canadian Dollar into account “strongly,” according to Bloomberg news. The Bank does not know how the economy will react to higher rates. The policy rate is still low relative to neutral levels, and rates below neutral are still appropriate given risks. The current level of interest rates are “exceptional.” Unlike the Fed, BoC speakers have spoken with one voice, so Lane’s outing is interesting following last week’s defense of the Bank’s communication strategy between July and September and Wilkins’ reminder that all meetings are “live.” Lane himself reiterated that all meetings are live. There is plenty here to suggest they will take a breather next month and perhaps shift to a more gradualist strategy. That being said, more firm data would tip the balance in favour of a rate hike, given that each announcement is “live.” Note that Poloz speaks on September 27th, and he will take questions from the press. Today’s speech does significantly trim the odds for a move next month however.

Main Macro Events Today

German ZEW – A slight improvement in the expectations reading to 12.5 from 10.0 in the previous monthis anticipated, indicating that optimists still outnumber pessimists and that confidence stabilised slightly in line with stocks, after being hit by geopolitical risks in the previous survey round. Even if the ZEW comes in much weaker than anticipated, it would only support the arguments of the doves at the ECB, who are reluctant to commit to an end date for QE just yet, while a stronger than expected number is unlikely to prompt a majority for Weidmann’s push to end QE.

US Housing Stats – August housing starts are projected to dip modestly to 1.150 mln after tumbling 4.8% to 1.155 mln in July. Risk is to the downside due to disruptions from Harvey.

Canada Manufacturing – Manufacturing shipments values, are expected to reveal a 1.5% m/m drop in July after the 1.8% decline in June. This projection is supported by a tremendous 4.9% plunge in export values during July. Prices played a role however, with the IPPI down 1.5% (m/m, nsa). Hence the decline in the manufacturing shipment volume measure may be less pronounced.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in